Battery Electric Vehicles and Emissions in India

Recent studies reveal vital information about the emissions of passenger vehicles in India. A collaboration between the Indian Institute of Technology (IIT) Roorkee and the International Council on Clean Transportation (ICCT) has shown that Battery Electric Vehicles (BEVs) emit up to 38 per cent less carbon dioxide equivalent (CO₂e) per kilometre compared to Internal Combustion Engine (ICE) vehicles. This research synthesises findings from six life-cycle greenhouse gas emission assessments.

Key Findings of the Study

The study marks three main factors that contribute to the variability in emissions – grid carbon intensity, laboratory test assumptions, and real-world driving conditions. Together, these factors account for nearly 75 per cent of the differences in emissions. The analysis indicates that emissions can vary based on grid mix and efficiency, with differences reaching up to 368 grams of CO₂e per kilometre.

Advantages of Battery Electric Vehicles

BEVs consistently outperform ICE and Hybrid Electric Vehicles (HEVs) in terms of life-cycle GHG emissions. Their efficiency is maximised when analyses reflect real-world performance rather than unrealistic energy consumption assumptions. The study warns against delaying BEV adoption in anticipation of a cleaner grid. Vehicles that are ICE will remain operational for 10 to 15 years, continually contributing to emissions.

Real-World Performance and Testing

The discrepancy between laboratory test cycles and real-world fuel use in HEVs is . Accurate emissions accounting requires the application of real-world correction factors. BEVs demonstrate the highest energy efficiency in practice, underscoring the need for stringent fuel efficiency standards. Real-world adjustments are essential, particularly for BEVs, where charging losses are often overlooked.

Importance of Land-Use Change in Assessments

Many assessments fail to consider land-use change, leading to an underestimation of emissions from biofuels. For example, diesel production emissions vary widely depending on land-use change considerations. This oversight can misrepresent the environmental impact of biofuels and needs to be addressed in future evaluations.

Policy Recommendations

https://www.gktoday.in/battery-electric-vehicles-and-emissions-in-india/

We came across a bullish thesis on Northern Dynasty Minerals Ltd. (NAK) on TripleS Special Situations’s Substack by Tiny Stock Ninja. In this article, we will summarize the bulls’ thesis on NAK. Northern Dynasty Minerals Ltd. (NAK)'s share was trading at $1.2 as of 4th June.

Is Southern Copper Corporation (SCCO) the Best Stock To Buy According to Marjorie Taylor Greene?

A large open-pit mining site, its machinery providing a long-term supply of copper.

Northern Dynasty Minerals (NAK) offers a uniquely asymmetric investment opportunity at the intersection of geopolitics, resource sovereignty, and severe market mispricing. The Pebble Project—one of the world’s largest undeveloped copper deposits—has long been stalled by regulatory hurdles, but the return of the Trump administration has radically altered its strategic outlook.

Recent executive orders prioritize domestic mineral independence and list copper and gold as critical to national security, with directives to expedite permitting. These policy shifts directly benefit dormant projects like Pebble, especially as the U.S. now imports over 45% of its copper.

Simultaneously, the global copper supply is entering a structural deficit, exacerbated by decades of underinvestment and geopolitical tensions, including tariffs cutting off U.S. access to Chinese rare earths. Legally, Northern Dynasty has advanced its position through persistent appeals and a well-documented challenge to both the EPA veto and Army Corps denial, citing contradictions with the Final Environmental Impact Statement, which found no measurable impact on local fisheries.

These appeals align with the administration’s deregulatory momentum, especially in Alaska, where a broad pro-development agenda is unfolding. The Pebble resource base is staggering, with measured and inferred deposits totaling tens of billions of pounds of copper and millions of ounces of gold, carrying a gross market value exceeding $400 billion.

At a current market cap of just $660 million, the upside is massive, with after-tax profits projected in the tens of billions. While regulatory and execution risks remain high, the strategic alignment of policy, resource needs, and valuation distortion sets the stage for potentially generational returns.

Previously, we have covered a bullish thesis on Harmony Gold Mining Company Limited (HMY) by Intelligent_Okra5374 on the Value Investing Subreddit in April 2025, which operates in the same industry as Northern Dynasty Minerals Ltd. (NAK). Harmony Gold is a profitable, cash-generative gold producer with diversified assets and a strong balance sheet, benefiting from macro tailwinds in precious metals and expanding into copper for long-term growth.

https://finance.yahoo.com/news/northern-dynasty-minerals-ltd-nak-154317032.html

COPPER smelters are paying unprecedented sums to process raw materials as China’s aggressive expansion of processing facilities creates a global market imbalance that threatens the viability of facilities worldwide, the Financial Times reported today.

Processing fees charged by smelters have turned negative for most of this year, hitting a record low of minus $45 per ton in May, said the newspaper, citing Fastmarkets data. This means smelters are effectively paying to process copper concentrate rather than earning their traditional margins, forcing many to operate at a loss simply to keep running.

“There is likely to be reduced copper smelter activity and potentially also some shutdowns in the Asian market,” Toralf Haag, CEO of copper producer Aurubis, told the FT.

The crisis stems from China’s strategic push to dominate base metals markets through massive capacity expansion, even as Western nations seek to reduce their dependence on Chinese processing. China has continued building new smelting facilities despite a shortage of the concentrate needed to feed them, the newspaper said.

Several facilities have already succumbed to market pressures. Glencore halted operations at its Pasar smelter in the Philippines in March, citing “increasingly challenging market conditions.” Analysis group CRU reported that continued commissioning of Chinese smelters is exacerbating downward pressure on processing fees.

The negative fees persist despite copper prices reaching near-record levels, with London copper trading at roughly £7,650 per ton on Monday. Global demand is expected to outstrip supply by 30% by 2035, according to the International Energy Agency.

Analysts warn that benchmark processing fees on long-term contracts between smelters and miners could turn negative for the first time, potentially forcing “meaningful smelting capacity reductions,” said Andrew Cole of Fastmarkets.

https://www.miningmx.com/trending/61417-copper-smelters-face-record-losses-amid-oversupply/

By Anushree Mukherjee and Kavya Balaraman

(Reuters) -Platinum and palladium prices have both rallied this month, notching a more than four-year and seven-month high respectively, but analysts say they remain more cautious about the outlook for palladium due to its narrower demand base.

Spot platinum was trading at $1,272.45 per ounce as of 1545 GMT on Wednesday, its highest level since February 2021, and has risen 41% this year on supply concerns, renewed investor interest following London Platinum Week in May, and increased jewellery demand as high gold prices drive consumers to cheaper alternatives, analysts say.

Spot palladium, meanwhile, was trading at $1,078.62/oz, its highest level since November 2024, and has gained 18% this year, but has struggled to reach the high of $1,244.75 hit in October 2024.

"The biggest factor is likely the wider appeal which platinum enjoys. Platinum’s uses are more diverse, spanning industrial applications, jewelry, and investor demand," said Zain Vawda, market analyst at MarketPulse by OANDA.

"This diversification shields platinum from the headwinds palladium faces, such as declining long-term demand from the traditional automotive market due to the EV transition."

Palladium is mainly used in catalytic converters for gasoline vehicles, while platinum has broader uses in diesel catalytic converters, jewellery, industrial applications, and emerging hydrogen technologies.

PALLADIUM PRICES LAGGING

Palladium could be considered a "one trick pony", with 90% of its demand coming from car manufacturers, Bank of America said in a note last week.

"China's rising EV penetration rates are particularly damaging because it means that palladium-intensive cars with a gasoline engine are now being quickly displaced," the note added.

The transition to EVs will also affect platinum in the medium term, but to a lesser extent, analysts told Reuters.

"Large commercial vehicles will likely use larger amounts of platinum (relative to palladium) and these vehicles will be slower to electrify. Over time, the hydrogen economy will also absorb some platinum, limiting the downside risk on platinum versus palladium," said Nitesh Shah, commodities strategist at WisdomTree.

Global sales of battery-electric vehicles and plug-in hybrids rose to 1.5 million in April. Sales in China were up 32% from the same month of 2024 to 0.9 million vehicles.

PLATINUM RALLIES

Platinum, meanwhile, is expected to be moderately supported over the next six to 12 months, although the upside may be capped without a clear rebound in auto demand or meaningful acceleration in hydrogen-related applications, said Alexander Zumpfe, a precious metals trader at Heraeus Metals Germany.

https://finance.yahoo.com/news/platinum-surges-palladium-lags-narrow-163815752.html

Wall Street's attention next week will be on further trade developments and key inflation data.

U.S. and Chinese officials, including U.S. Treasury Secretary Scott Bessent, Secretary of Commerce Howard Lutnick, Trade Representative Ambassador Jamieson Greer, and Chinese Vice Premier He Lifeng, are set to meet in London on Monday. Investors will be keeping a close eye on the talks. The last round of discussions had resulted in a surprise temporary trade truce, boosting market sentiment.

Turning to the economic calendar, traders will receive May readings for the consumer price index and the producer price index.

The earnings season next week is highlighted by video game retailer GameStop (GME), cloud software firm Oracle (ORCL) and Photoshop creator Adobe (ADBE).

Also grabbing the spotlight will be Apple's (AAPL) WWDC 2025, kicking off on Monday. The event is expected to feature major announcements and a first look at new updates for iOS, iPadOS, macOS, watchOS, tvOS, and visionOS.

Earnings spotlight: Monday, June 9: Casey's General Stores (CASY), Calavo Growers (CVGW), Lakeland Industries (LAKE). See the full earnings calendar.

Earnings spotlight: Tuesday, June 10: GameStop, J. M. Smucker (SJM), United Natural Foods (UNFI), GitLab (GTLB). See the full earnings calendar.

Earnings spotlight: Wednesday, June 11: Oracle, Chewy (CHWY), SailPoint (SAIL). See the full earnings calendar.

Earnings spotlight: Thursday, June 12: Adobe, Lovesac (LOVE). See the full earnings calendar.

https://seekingalpha.com/article/4793264-wall-street-week-ahead?source=feed

2 Picks For Monthly Distributions And Participating With Activists

Summary

Aleksandra Zhilenkova/iStock via Getty Images

Written by Nick Ackerman, co-produced by Stanford Chemist

Closed-end funds can offer opportunities to invest in assets at below their current valuation, which is through the discount/premium mechanic. That is the result of these funds not having a creation and redemption mechanism, such as is the case with their traditional open-ended mutual funds and exchange-traded funds counterparts. With that, they can present these potential opportunities, and there are activist groups that specifically target these types of opportunities.

Investing in them through activist funds can be an interesting way to participate in their expertise in this area, while also delivering substantial diversification. We're looking at two funds today that have a long history of delivering solid results through the generation of their high distributions paid monthly.

#1 Special Opportunities Fund (SPE)

SPE "employs an opportunistic investment philosophy with a particular emphasis on investing in discounted closed-end funds, undervalued operating companies, and other attractive special situations, including risk arbitrage and distressed securities."

This is a fund that is the result of Bulldog Investors taking over in 2009 as an activist target.

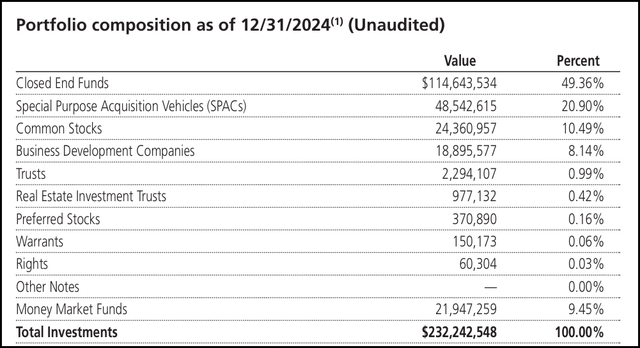

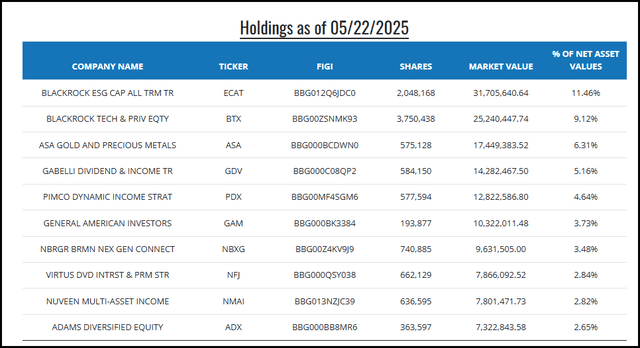

As another closed-end fund, there is a unique opportunity here to pick up a position that is at a discount itself, while it invests in a significant allocation of other discounted CEFs. Besides around half of its portfolio being invested in traditional CEFs, they also hold an allocation to business development companies. These are also a pool of assets, usually mostly senior loan investments. Otherwise, the fund also has a rather high allocation to special purpose acquisition vehicles and common stocks.

SPE Portfolio Composition (Bulldog Investors)

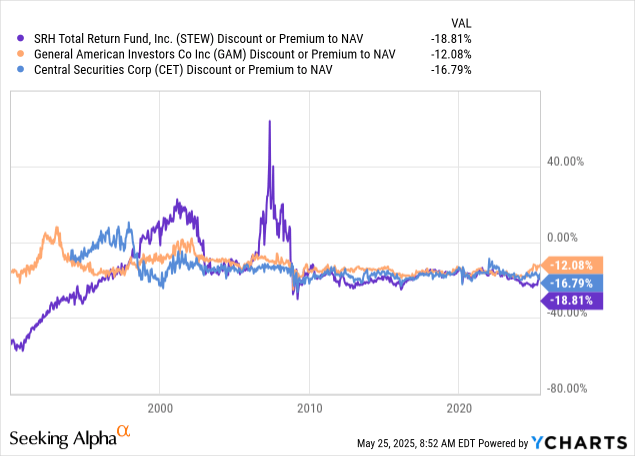

The top positions of the fund tend to be heavily discounted CEFs, with SRH Total Return (STEW) and General American Investors (GAM) being the top two. This is then followed by BDC CION Investment (CION) and then back to a traditional CEF Central Securities Corp. (CET). STEW, GAM and CET all trade at wide discounts, and have tended to do so for quite a significant period of time.

They've also been regular positions in SPE's portfolio, so these three appear to be more core types of positions for the fund.

Similar to CEFs, BDCs can also trade at discounts, and as of the last reported NAV, CION is pushing near a 33% discount.

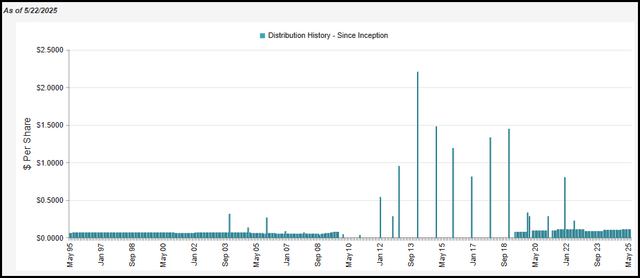

SPE provides a monthly distribution that is based on a managed 8% NAV distribution rate calculated at the end of the year. They pay monthly, which is another potentially attractive feature of SPE. CET and GAM pay semi-annual distributions, with CION and STEW paying quarterly. In a way, that makes SPE convert these into more regular monthly payers.

The distribution policy went into place several years ago, as SPE was a rather irregular payer too. Then, prior to 2009, it was a muni fund.

SPE Distribution History (CEFConnect)

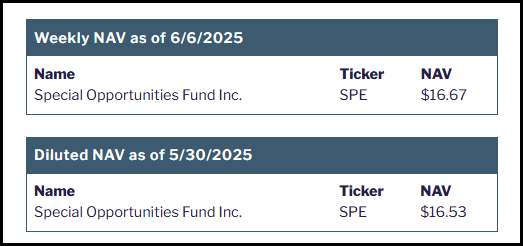

They report NAV weekly, and they also include a diluted NAV due to their leverage coming via a convertible preferred offering, the Special Opportunities Fund 2.75% Convertible Preferred Series C (SPE.PR.C). This is an enviable leverage rate when you consider that most other funds are borrowing through a credit facility, paying closer to 5% these days.

SPE Weekly NAV (Bulldog Investors)

Worth noting is that SPE is being leveraged and holding other CEFs that are also leveraged; you can get leverage on leverage, which could make SPE even more volatile. In that same line of thinking, that also comes with fees on fees, so being able to pick up SPE at a meaningful discount can be important.

At this time, I believe that SPE is presenting a fairly attractive time to consider investing in this fund. Our buy target is at around a 10% discount, and we are quite close to that, but technically just under, based on the latest weekly NAV. If calculating it based on the diluted NAV reported a week earlier, then we are at an 11% discount.

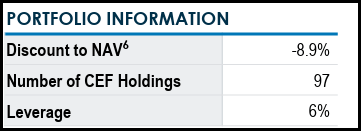

#2 Saba Closed-End Funds ETF (CEFS)

CEFS' investment objective and investment strategy are to "generate high income by investing in closed-end funds trading discounted to net asset value, and hedging the portfolio's exposure to rising interest rates."

CEFS is an exchange-traded fund, which doesn't provide a "discount on discount" opportunity due to the ETF creation and redemption mechanism that keeps the NAV per share reasonably close to the share price. That said, as a Saba Capital managed fund, they are much more active when it comes to targeting CEFs.

CEFS Top Ten Holdings (Saba Capital)

The average discount to NAV of the underlying holdings was listed at nearly 9% across 97 holdings. The fund also utilizes leverage, but they've been reducing the leverage they're using. Keeping in mind, some of CEFS' portfolio holdings are also leveraged.

CEFS Portfolio Info (Saba Capital)

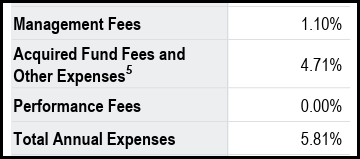

Unlike CEFs, ETFs have to report the acquired fund fees and other expenses, which are expenses of the underlying portfolio. Therefore, we get a good idea of what the fees on fees add up to with CEFS, which we don't get for SPE, as it isn't provided.

CEFS Expense Ratio (Saba Capital)

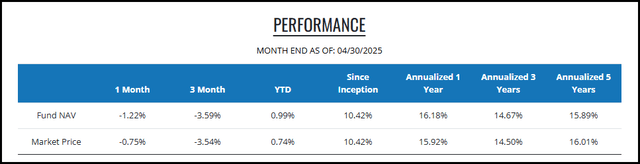

These are hefty expenses, but the fund's performance has been able to put up a solid track record of stronger long-term results, nonetheless, which is usually what counts.

CEFS Annualized Performance (Saba Capital)

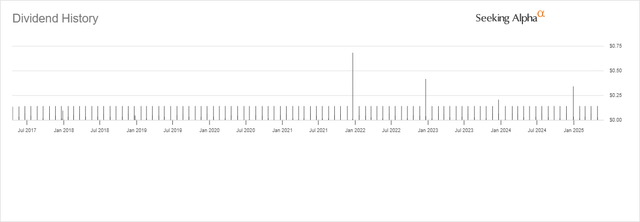

What else counts for investors in this fund is likely the distribution that is paid out monthly. Unlike most ETFs, they pay a level distribution, providing a predictable monthly payout for extended periods of time. Most other ETFs pay out whatever income/gains they'd have generated during the period. At this time, they pay $0.14 a month as the regular distribution and then pay out a year-end special as required.

CEFS Distribution History (Seeking Alpha)

Conclusion

SPE and CEFS provide significant diversification wrapped up into one package through investing in underlying CEFs. Both of these funds are run by activists, though Saba Capital tends to be much more aggressive relative to Bulldog. For SPE, one has the opportunity of investing in a discounted fund that is also trading at a discount to its NAV. For CEFS, it may not have a meaningful discount, but being more active can tend to drive discount narrowing within the underlying portfolio of holdings.

At the CEF/ETF Income Laboratory, we manage closed-end fund (CEF) and exchange-traded fund (ETF) portfolios targeting safe and reliable ~8% yields to make income investing easy for you. Check out what our members have to say about our service.

Russia said on Sunday that its forces had launched cluster sticks against multiple military targets of Ukraine, while Ukraine, on the same day, reported downing a Russian Su-35 fighter jet.

The Russian military conducted cluster strikes using long-range precision weapons and drones against targets in Ukraine in the past 24 hours. The strikes targeted enterprises of Ukraine's military-industrial complex, including workshops assembling attack drones, facilities for the maintenance and repair of weapons and military equipment, and ammunition depots, the Russian Ministry of Defense said.

The objective of the strikes has been achieved, with all designated targets being hit, the ministry said.

It also said that the Russian air defense systems shot down a total of 311 Ukrainian fixed-wing drones, among which 140 were located outside the special military operation area, and the Russian army also destroyed four Ukrainian unmanned boats in the Black Sea.

On the same day, the General Staff of the Ukrainian Armed Forces reported over 100 combat clashes with Russian forces on the front lines over the past day, with the most intense fighting occurring in the directions of Pokrovsk and Krasnyi Lyman (Red Lyman).

The Ukrainian Air Force said that it shot down a Russian Su-35 fighter jet in the direction of Kursk on Saturday.

The Ukrainian side also said that on Friday, the Ukrainian military, in coordination with the Defense Intelligence of Ukraine, carried out strikes on multiple Russian military targets, including facilities within the territory of Russia.

Meanwhile, Ihor Terekhov, mayor of Ukraine's second-largest city of Kharkiv, said the city came under the "most intense" Russian attack early on Saturday since the outbreak of the conflict between the two countries.

On Saturday, Andriy Kovalenko, head of the Center for Countering Disinformation at Ukraine's National Security and Defense Council, said that a refinery owned by Russian company Lukoil had caught fire that day.

Kovalenko said that Lukoil is a key asset in Russia's energy sector, primarily providing aviation, armored vehicle, and logistical fuel for the Russian military.

There has been no response from the Russian side regarding this incident.

Russia strikes Ukrainian military targets, while Ukraine downs Russian fighter jet

President Trump and Chinese leader Xi Jinping spoke on Thursday, with tariff and trade talks set to resume next week.

Trump said Treasury Secretary Scott Bessent, Commerce Secretary Howard Lutnick, and US Trade Representative Jamieson Greer would meet with Chinese counterparts in London on Monday.

"The meeting should go very well," he said.

Trump's call with Xi, which both leaders framed as positive, came after weeks of Trump publicly pushing for the talk. US-China tensions have risen in the aftermath of the countries' trade truce reached in mid-May in Geneva, with both countries have accused the other of breaching that truce while ratcheting up pressure on other issues.

The US and China are also now using their control over certain key materials to gain control in the trade war. Bloomberg reported on Friday that the US dominates in ethane, a gas used to make plastics, and China buys nearly all of it. Washington is now tightening control by requiring export licenses. China's curbs on exports of rare earth minerals, crucial for autos and more, have drawn Washington's ire.

Read more: What Trump's tariffs mean for the economy and your wallet

The US-China talks come as Trump pushes countries to speed up negotiations. The US sent a letter to partners as a "friendly reminder" that Trump's self-imposed 90-day pause on sweeping "reciprocal" tariffs is set to expire in early July.

White House advisers have for weeks promised trade deals in the "not-too-distant future," with the only announced agreement so far coming with the United Kingdom. US and Indian officials held trade talks this week and agreed to extend those discussions on Monday and Tuesday ahead of the July 9 deadline.

Also effective Wednesday, June 4, Trump doubled tariffs on steel and aluminum from 25% to 50%

Meanwhile, Trump's most sweeping tariffs face legal uncertainty after a federal appeals court allowed the tariffs to temporarily stay in effect, a day after the US Court of International Trade blocked their implementation, deeming the method used to enact them "unlawful."

Here are the latest updates as the policy reverberates around the world.

LIVE

1110 updates

The U.K. Treasury has run out of road for delaying nuclear decisions, according to Whitehall and industry insiders.

LONDON — Philip Hunt, the unassuming Labour peer put in charge of rejuvenating U.K. nuclear energy, has a favorite joke about how slowly the industry moves.

Hunt — who was first an energy minister from 2008-2010 and retired from his second stint in government just last month — liked to roll out the gag at Westminster receptions, according to one industry figure who saw him in action.

“I came back after 14 years,” the minister would say, “and everything was exactly as I left it.”

It was a way to bash the Conservatives’ decade-and-a-half in power, but also an admission of the glacial pace of the nuclear world.

That is about to change. Ministers are prepping a series of high-profile nuclear announcements in the lead-up to the government-wide spending review on June 11.

The government is expected to unveil, after months of delay, the winner of a multi-billion pound contract to build next-generation small modular reactors (SMRs), known as “mini nukes.” A long-awaited financial decision on the mega nuclear plant Sizewell C in Suffolk is on its way. Meanwhile, U.K. officials are discussing buying up nuclear sites from private ownership to bring the industry under greater state control.

It would trigger more activity on nuclear over a handful of weeks than there has been in a generation.

This flurry of action is coming, insiders say, not because of astute maneuvering by Hunt or his political bosses but because the Treasury — long skeptical about nuclear — has run out of road for ignoring the problem.

The looming spending review, the last chance in this parliament to commit cash to the U.K.’s neglected nuclear energy system, “has forced the government’s hand,” said a second energy figure, granted anonymity, like others in this piece, to speak candidly about government planning.

Worried about the splurge

Bringing more low-carbon nuclear power online is crucial to two of Prime Minister Keir Starmer’s “missions” in government — galvanizing sluggish economic growth and ending the U.K.’s reliance on high-polluting fossil fuels.

Backing more nuclear power in a speech in February, Starmer said he was taking on “the blockers who have strangled our chances of cheaper energy, growth and jobs for far too long.”

The industry has its vocal supporters on Labour’s benches, too. “We urgently need new nuclear in this country, not just for the energy security but for the jobs and the growth opportunities, too,” said Charlotte Nichols, MP for the red wall seat Warrington North. Tom Greatrex, an ex-Labour MP who now heads the Nuclear Industry Association lobby group, said: “The time for talking is over. We need to see decisions being made.”

https://www.politico.eu/article/nuclear-power-will-spending-reviews-big-winner-philip-hunt/

By Metal Miner - Jun 07, 2025, 4:00 PM CDT

The Rare Earths MMI (Monthly Metals Index) found more price stability month-over-month. As a result, it moved sideways, with only a 0.81% increase. Despite this, the short-term outlook for rare earths remains uncertain. Chinese export restrictions jolted prices in H1 of 2025 and fractured long-running supply lines. Shortly after, global automakers warned that Beijing’s April curbs on alloys and magnet exports “could cause production delays” without fast relief.

China’s Rare Earths Shockwaves Continue to Jolt Global Markets

Chinese market data show how wild things got in May. According to China Tungsten Industry charts, Chinese rare earth prices jumped sharply in early May before easing later in the month. For example, after a brief rally, neodymium-praseodymium metal was about $4,176.53/ton higher. Overall, May’s closing prices were slightly above April levels.

China’s policy shock continues to be felt worldwide. The export bans target medium-heavy rare earths used in EV motors, wind turbines and high-tech weapons. One industry report said the restrictions “triggered a ripple effect” through global EV and clean-energy supply chains.

According to Reuters, the country still mines roughly 60% of the world’s rare earths and refines ~90% of them, making it the undisputed supply giant. MP Materials, the U.S.’s only large rare-earth miner, warned the situation is “broken,” and that China’s moves will force a laser focus on American supply security.

Trade Truce or Temporary Fix?

Throughout 2025, U.S. buyers have scrambled for solutions. After a G7 trade “truce” in mid-May, Washington pressed Beijing to ease restrictions, and Reuters sources say China may now fast-track export licenses for U.S. customers. Still, complete relief isn’t assured. Meanwhile, suppliers are sounding the alarm, warning that electric vehicles, defense and renewable energy are all in the crosshairs.

Permanent magnets are vital in EV motors. In fact, a single electric car can require several kilograms of neodymium and dysprosium. In aerospace and military manufacturing, the stakes are even higher. For instance, the F-35 fighter consumes roughly 900 pounds of rare-earth magnets, while a Virginia-class submarine requires over 9,200 pounds. Wind turbines and satellite systems also rely heavily on these materials.

Prices on Edge: U.S. Buyers Brace for a Volatile Summer

Rare earth element prices will likely experience continued instability over the next few months due to persistent supply challenges and rising geopolitical friction. China’s tightening of export controls on crucial materials like neodymium and praseodymium has caused significant ripples throughout global supply chains. These disruptions are hitting U.S. sectors especially hard, particularly those tied to electric vehicles, wind energy and national defense.

For U.S procurement teams, this landscape highlights the need to both diversify supply channels and support the development of domestic production. Rare earth companies are expanding output, but that effort won’t solve short-term shortages. In the meantime, decision-makers should stay alert to evolving market conditions and consider building up inventory as a buffer against future shocks. Regularly consulting trustworthy market data and industry insights will be essential to making informed sourcing decisions during this volatile period.

Many procurement teams have shifted strategies overnight. Manufacturers are diversifying suppliers, boosting recycling of old magnets and even redesigning products to use fewer heavy rare earths. For example, EU firms are planning magnet recovery from scrap batteries and turbines, while the EU government recently identified 13 new mining projects outside China to shore up supply.

Summary

We have three strategic asset-allocation models, based on risk-tolerance levels: Conservative, Growth, and Aggressive. We make tactical adjustments to the models on a regular basis, based on our outlooks for the various segments of the capital markets. In terms of performance through May, stocks and bonds are neck-and-neck, both with sub-par returns of 1% year to date. Looking ahead from an asset-allocation standpoint, our Stock-Bond Barometer model still slightly favors bonds over stocks for long-term portfolio positioning. In other words, these asset classes should be near their target weights in diversified portfolios, with a slight tilt toward bonds. We are over-weight on large-caps at this stage of the market cycle. We favor large-caps for growth exposure and financial strength, amidst volatility. Our recommended exposure to small- and mid-caps is 10% of equity allocation, below the benchmark weighting. Global stocks have taken an early performance lead in 2025, although U.S. stocks have outperformed their global peers over the trailing one- and five-year periods. We expect the long-term trend favoring U.S. stocks to re-emerge, given volatile global economic, political, geopolitical, and currency conditions.

The Bundesbank lowered expectations in its new six-month forecast

The German Bundesbank expects the economy to stagnate in 2025 after two years of recession in the country. This is stated in the new six-month forecast of the central bank, released at the end of last week.

Thus, the regulator has downgraded its December expectations, according to which Germany’s GDP growth was expected to reach 0.2% this year.

As noted, the recovery of the German economy is delayed due to uncertainty over international trade policy, and fiscal measures are only gradually beginning to support it.

According to Bundesbank President Joachim Nagel, new US tariffs and uncertainty about future US policy will initially slow economic growth. This hits German industry at a time when it is beginning to stabilize after a long period of weakness. However, a sharp increase in government spending on defense and infrastructure should provide a noticeable boost to demand and GDP growth from 2026 onwards. According to the new forecast, inflationary pressures in Germany also continue to decline.

The central bank predicts that the country’s GDP will grow by 0.7% in 2026 (December expectations – 0.8%), and by 1.2% in 2027 (0.9% in December).

Bundesbank experts point out that the short-term prospects are primarily overshadowed by the protectionist trade policy of the United States. In general, German exports will decline significantly in 2025 and grow only slightly in 2026. The decline in industrial production due to tariffs is cooling the labor market and slowing wage growth.

“Starting in 2026, expansionary fiscal policy and the reduction of the inhibitory effect of US economic policy on growth will lead to a marked recovery in the German economy,” the regulator said in a statement.

Inflation growth will slow to an average annual rate of 2.2% in 2025. In 2026, it is expected to temporarily decline to 1.5% due to energy prices, and then rise again to 1.9% in 2027.

The European Central Bank has maintained its estimate of eurozone GDP growth this year at 0.9%. Expectations for the next year have been revised to 1.1% (previously 1.2%). In 2027, the eurozone economy is expected to grow by 1.3%.

https://gmk.center/en/news/german-central-bank-does-not-expect-economic-growth-in-2025/

By Eurasianet - Jun 09, 2025, 1:00 PM CDT

China has shifted from the world’s largest creditor nation to the globe’s biggest debt collector. Central Asian states owe billions to Chinese entities, but their geographic importance to Beijing is helping protect them from strong-arm repayment tactics.

A report issued by the Australia-based Lowy Institute, Peak repayment: China’s global lending, charts China’s transition from “lead bilateral banker to chief debt collector of the developing world.” It shows that China’s lavish loaning under the auspices of its Belt & Road Initiative (BRI) from 2013-2018 is now set to inflict lots of fiscal pain on recipients. Debtor nations, many of them described in the report as “the world’s poorest and most vulnerable countries,” owe $22 billion to China in 2025.

“Beijing has transitioned from capital provider to net financial drain on developing country budgets as debt servicing costs on [BRI] projects from the 2010s now far outstrip new loan disbursements,” the report states. “In 2012, China was a net drain on the finances of 18 developing countries; by 2023, the count had risen to 60. In full, China’s net flows to developing countries dropped to negative $34 billion in 2024.”

At the start of 2024, Central Asian states collectively owed Chinese state entities roughly $20 billion, with Kazakhstan’s having the largest share at $9.2 billion. Kyrgyzstan’s and Uzbekistan’s debts totaled almost $4 billion each, while Tajikistan owed China about $3 billion.

The debt amounts for Kazakhstan and Uzbekistan appear manageable within the context of those nations’ overall GDP numbers, according to economic experts. Meanwhile, Kyrgyzstan and Tajikistan can be considered prime candidates for falling into a Chinese debt trap. Turkmenistan’s debtor status, given the country’s opaque governing system, is murky, but Ashgabat at the same time is the only Central Asian state running a trade surplus with Beijing, due to its abundant natural gas exports.

A combination of factors is behind China’s transition from lender to debt collector, including the slowdown of China’s domestic economy. But the current surge in debt collection is also a natural outgrowth of the terms of many BRI loans, which included grace periods of up to five years followed by relatively compressed timelines for loan repayment. “Because China’s Belt and Road Initiative lending spree peaked in the mid-2010s, those grace periods began expiring in the early 2020s,” the report notes. “The early 2020s was always likely to be a crunch period for developing country repayments to China.”

Lowy Institute analysts seem to believe China is unlikely to turn the screws on Central Asian states. The report notes that Beijing is continuing to extend loans to “strategic and resource critical partners” including Kazakhstan, Kyrgyzstan and Tajikistan.

The change in Chinese lending behavior could well hamper the ability of developing nations, including Central Asian states, to hit growth targets, reduce poverty rates and address global-warming related issues.

“The burden from Chinese debts coming due is also part of a broader set of severe headwinds, particularly for the poorest and most vulnerable economies,” the report states. “An increasingly isolationist United States and a distracted Europe are withdrawing or sharply cutting their global aid support. Reliant on an open, rules-based global trading system, developing economies must also grapple with the impact of new trade-war shocks and the specter of punitive US tariffs being levelled against them.”

Beijing too faces tough geopolitical choices; Chinese officials will need to strike a delicate balance between pressing debtor nations to meet their obligations while not engendering hard feelings that could undermine the country’s geopolitical interests. “Pushing too hard for repayment could damage bilateral ties and undermine its diplomatic goals,” the report states. “At the same time, China’s lending arms, particularly its quasi-commercial institutions, face mounting pressure to recover outstanding debts.”

It’s not just Beijing’s debt-recovery actions that may pose an image problem for the country. An investigative report by the Uzbek outlet Anhor.uz published on June 4 indicated that Chinese entities are engaging in what appear to be predatory business practices in Uzbekistan. The report documents the influx of Chinese companies into the country’s construction sector resulting in a decrease in the price of cement to a point where local Uzbek cement-makers can’t compete and are being driven out of business.

“Over the past two years, almost half of Uzbekistan’s cement plants have ceased operations — only 24 remain, nine of which belong to Chinese companies,” the Anhor report states.

https://oilprice.com/Geopolitics/International/Central-Asias-Debt-Burden-to-China-Examined.html

June 10, 2025 — 09:11 pm EDT

Written by RTTNews.com for RTTNews->

(RTTNews) - Australian shares are trading notably higher on Wednesday, extending the gains in the previous session, with the benchmark S&P/ASX 200 moving well above the 8,600 level, following the broadly positive cues from Wall Street overnight, with gains across most sectors led by energy and technology stocks.

The benchmark S&P/ASX 200 Index is gaining 37.10 points or 0.43 percent to 8,624.30, after touching a high of 8,639.10 earlier. The broader All Ordinaries Index is up 36.50 points or 0.41 percent to 8,849.20. Australian stocks ended significantly higher on Tuesday.

Among major miners, BHP Group and Fortescue metals are gaining more than 2 percent each, while Rio Tinto is adding more than 1 percent and Mineral Resources is advancing almost 4 percent.

Oil stocks are mostly higher. Woodside Energy is gaining more than 3 percent, Santos is adding 1.5 percent and Origin Energy is edging up 0.4 percent, while Beach energy is losing more than 1 percent.

In the tech space, Afterpay owner Block is losing more than 1 percent and Xero is edging down 0.1 percent, while WiseTech Global is gaining more than 1 percent and Appen is adding almost 1 percent.

Zip is jumping more than 15 percent after the buy now pay later company upgraded its full-year earnings guidance amid continued strong performance, particularly in the US business.

Among the big four banks, Commonwealth Bank, National Australia bank, Westpac and ANZ Banking are all edging up 0.3 to 0.5 percent each.

Among gold miners, Evolution Mining is edging down 0.5 percent and Resolute Mining is declining more than 1 percent, while Northern Star Resources and Newmont are down almost 1 percent each. Gold Road Resources is gaining almost 1 percent.

In other news, shares in Johns Lyng Group are jumping more than 14 percent after the integrated building services group confirmed media reports of a non-binding indicative offer from Pacific Equity Partners.

Shares in Perseus Mining are slipping almost 6 percent after the gold miner released weak five-year operating outlook.

Shares in Pilbara Minerals are surging more than 8 percent after the lithium miner revealed a significant upgrade to the mineral resource at its 100%-owned Pilgangoora Operation in Western Australia.

In the currency market, the Aussie dollar is trading at $0.652 on Wednesday.

On the Wall Street, stocks moved modestly to the upside on Tuesday as traders await the outcome of the ongoing trade talks between China and the U.S. in London. Trade negotiations between the world's two largest economies commenced on Monday - and while U.S. Commerce Secretary Howard Lutnick told reporters the talks are "going well," there has been no breakthrough as of yet.

The Dow climbed 105.11 points or 0.25 percent to finish at 42,866.87, while the NASDAQ gained 123.75 points or 0.63 percent to close at 19,714.99 and the S&P 500 added 32.93 points or 0.55 percent to end at 6,038.81.

Meanwhile, the major European markets turned in a mixed performance on the day. The U.K.'s FTSE 100 gained 0.44 percent, while Germany's DAX and France's CAC 40 closed down 0.1 percent and 0.2 percent, respectively.

Crude oil prices were down on Tuesday amidst uncertainty over trade talks between China and the United States continued, although the outcome remains uncertain. West Texas Intermediate crude oil for July delivery closed down by $0.31 to settle at $64.98 per barrel.

https://www.nasdaq.com/articles/australian-market-notably-higher-91

Rolls-Royce SMR selected as preferred bidder to build country’s first small modular reactors.

From:Department for Energy Security and Net Zero, Great British Energy – Nuclear, The Rt Hon Ed Miliband MP and The Rt Hon Rachel Reeves MP

Published 10 June 2025

Rolls-Royce SMR has been selected as the preferred bidder to partner with Great British Energy – Nuclear to develop small modular reactors, subject to final government approvals and contract signature – marking a new golden age of nuclear in the UK.

Today (Tuesday 10 June) Great British Energy – Nuclear has taken on a new name from Great British Nuclear, reflecting its joint mission with Great British Energy to rollout clean homegrown power as 2 publicly-owned energy companies.

As part of the government’s modern Industrial Strategy to revive Britain’s industrial heartlands, the government is pledging over £2.5 billion for the overall small modular reactor programme in this Spending Review period – with this project potentially supporting up to 3,000 new skilled jobs and powering the equivalent of around 3 million homes with clean, secure homegrown energy.

The biggest nuclear rollout for a generation will support the clean power mission – boosting energy security and protecting families’ finances. Great British Energy - Nuclear is aiming to sign contracts with Rolls-Royce SMR later this year and will form a development company.

Great British Energy - Nuclear will also aim to allocate a site later this year and connect projects to the grid in the mid-2030s. Once small modular reactors and Sizewell C come online in the 2030s, combined with the new station at Hinkley Point C, this will deliver more nuclear to the grid than over the previous half century.

‘SMRs’ are smaller and quicker to build than traditional nuclear plants, with costs likely to come down as units are rolled out. The outcome of this competition is the first step towards reducing costs and unlocking private finance, enabling the UK to realise its long-term ambition of delivering one of Europe’s first small modular reactor fleets. It comes after the government announced plans to shake up the planning rules to make it easier to build nuclear, including small modular reactors across the country.

Energy Secretary Ed Miliband said:

We are ending the no-nuclear status quo as part of our Plan for Change and are entering a golden age of nuclear with the biggest building programme in a generation.

Great British Energy - Nuclear has run a rigorous competition and will now work with the preferred bidder Rolls-Royce SMR to build the country’s first ever small modular reactors – creating thousands of jobs and growing our regional economies while strengthening our energy security.

Chancellor of the Exchequer, Rachel Reeves, said:

The UK is back where it belongs, taking the lead in the technologies of tomorrow with Rolls-Royce SMR as the preferred partner for this journey.

We’re backing Britain with Great British Energy - Nuclear’s ambition to ensure 70% of supply chain products are British built, delivering our Plan for Change through more jobs and putting more money in people’s pockets.

Simon Bowen, Chairman of Great British Energy – Nuclear said:

This announcement is a defining moment for the UK’s energy and industrial future.

By selecting a preferred bidder, we are taking a decisive step toward delivering clean, secure, and sovereign power. This is about more than energy—it’s about revitalising British industry, creating thousands of skilled jobs, and building a platform for long-term economic growth.

Gwen Parry-Jones, CEO of Great British Energy - Nuclear, said:

We are proud to lead this national mission. Nuclear is the cornerstone of the UK’s energy strategy, and today’s announcement will accelerate deployment.

Together with Rolls-Royce SMR, our selected preferred bidder, and subject to government approvals and contract signature, we will deliver a programme that is technically world-class and delivers real value to the British people—through energy security, economic opportunity, and environmental leadership.

The global SMR market is, according to the International Energy Agency, projected to reach up to nearly £500 billion by 2050, and today’s announcement puts Britain at a competitive advantage as a frontrunner in the global race to build new nuclear technology.

The selection follows a rigorous and transparent procurement process over 2 years, with the competition having launched in July 2023. Subject to final approvals and contract signature, Rolls-Royce SMR Ltd will enter a strategic technology development partnership with Great British Energy - Nuclear – a fully publicly-owned company.

Rolls-Royce SMR is progressing through the final stage of the assessment by the UK nuclear industry’s independent regulators.

Notes to editors

As it moves to its delivery phase, Great British Nuclear has been renamed to Great British Energy – Nuclear, an allied company to Great British Energy. Two separate publicly-owned energy companies with a shared mission - providing a clear signal at home and on the world stage that from SMRs to floating offshore wind, Britain is determined to win the race for the industries of the future.

In its founding statement, the government confirmed it would explore how Great British Energy and Great British Nuclear can best work together: Great British Energy founding statement. The first call for evidence on SMRs was launched a decade ago in 2015 under a previous government.

https://www.gov.uk/government/news/rolls-royce-smr-selected-to-build-small-modular-nuclear-reactors

New Delhi: A disruption in rare earth magnet supplies lasting beyond a month can impact production of passenger vehicles, including electric models, weighing on the domestic automobile industry’s growth momentum, a report on Tuesday said.

Rare earth magnets, low in cost but critical in function, could emerge as a key supply-side risk for India’s automotive sector if China’s export restrictions and delays in shipment clearances persist, Crisil Ratings said in a statement. “The supply squeeze comes just as the auto sector is preparing for aggressive EV rollouts. Over a dozen new electric models are planned for launch, most built on PMSM platforms,” Crisil Ratings Senior Director Anuj Sethi said.

While most automakers currently have 4-6 weeks of inventory, prolonged delays could start affecting vehicle production, with EV models facing deferrals or rescheduling from July 2025, he added. A broader impact on two-wheelers and ICE PVs may follow if the supply bottlenecks persist for an extended period, Sethi said. “The shortage of rare earth magnets is forcing automakers to reassess supply-chain strategies. Despite contributing less than 5 per cent of a vehicle’s cost, these magnets are indispensable for EV motors and electric steering systems,” said Crisil Ratings Director Poonam Upadhyay. Automakers are actively engaging with alternative suppliers in countries such as Vietnam, Indonesia, Japan, Australia, and the US, while also optimising existing inventories, she noted.

Rare earth magnets are integral to Permanent Magnet Synchronous Motors (PMSMs) used in EVs for their high torque, energy efficiency and compact size. Hybrids also depend on them for efficient propulsion. In internal combustion engine (ICE) vehicles, the use of rare earth magnets is largely limited to electric power steering and other motorised systems. In April this year, China, the world’s dominant exporter of rare earth magnets, imposed export restrictions on seven rare earth elements and finished magnets, mandating export licences.

The revised framework demands detailed end-use disclosures and client declarations, including confirmation that the products will not be used in defence or re-exported to the US. With the clearance process taking at least 45 days, this added scrutiny has significantly delayed approvals.

https://www.thehansindia.com/business/rare-earth-magnets-supply-risk-to-india-978830

Low water levels at the Haweswater reservoir in the valley of Mardale, Cumbria. The north west of England is now in drought following one of the driest springs on record.

It has been an exceptionally dry spring in north-western Europe and the second warmest May ever globally, according to the Copernicus Climate Change Service (C3S).

Countries across Europehave been hit by drought conditions in recent months, with water shortages feared unless significant rain comes this summer, and crop failures beginning to be reported by farmers.

The new Copernicus data shows that May 2025 was the second-warmest May globally, with an average surface air temperature of 15.79 degrees, 0.53 degrees above the 1991-2020 average for May. The month was 1.4 degrees above the estimated 1850-1900 average used to define the pre-industrial level. This interrupts a period of 21 months out of 22 where the global average temperature was more than 1.5C above the pre-industrial level.

Carlo Buontempo, director of C3S at the European Centre for Medium-Range Weather Forecasts (ECMWF), said: “May 2025 breaks an unprecedentedly long sequence of months over 1.5 degrees above pre-industrial. Whilst this may offer a brief respite for the planet, we do expect the 1.5 degrees threshold to be exceeded again in the near future due to the continued warming of the climate system.”

The 1.5 degrees is the climate target agreed by the 2015 Paris agreement. The target of 1.5 degrees is measured over a decade or two, so a single year above that level does not mean the target has been missed, but does show the climate emergency continues to intensify.

Every year in the past decade has been one of the 10 hottest, in records that go back to 1850.

Dry weather has persisted in many parts of the world.

In May 2025, much of northern and central Europe as well as southern regions of Russia, Ukraine, and Turkey were drier than average.

Parts of north-western Europe experienced the lowest precipitation and soil moisture levels since at least 1979.

In May 2025, it was drier than average in much of north America, in the Horn of Africa and across central Asia, as well as in southern Australia, and much of both southern Africa and South America.

May also saw abnormally high sea surface temperatures in the north-eastern Atlantic, reaching the highest ever recorded, according to Copernicus. - Guardian

Beijing has a virtual monopoly on supply of the critical minerals used to make everything from cars to wind turbines.

China’s export of rare earth elements is central to the trade deal struck this week with the United States.

Beijing has a virtual monopoly on the supply of the critical minerals, which are used to make everything from cars to drones and wind turbines.

Earlier this year, Beijing leveraged its dominance of the sector to hit back at US President Donald Trump’s sweeping tariffs, placing export controls on seven rare earths and related products.

The restrictions created a headache for global manufacturers, particularly automakers, who rely on the materials.

After talks in Geneva in May, the US and China announced a 90-day pause on their escalating tit-for-tat tariffs, during which time US levies would be reduced from 145 percent to 30 percent and Chinese duties from 125 percent to 10 percent.

The truce had appeared to be in jeopardy in recent weeks after Washington accused Beijing of not moving fast enough to ease its restrictions on rare earths exports.

After two days of marathon talks in London, the two sides on Wednesday announced a “framework” to get trade back on track.

Trump said the deal would see rare earth minerals “supplied, up front,” though many details of the agreement are still unclear.

What are rare earths, and why are they important?

Rare earths are a group of 17 elements that are essential to numerous manufacturing industries.

The auto industry has become particularly reliant on rare-earth magnets for steering systems, engines, brakes and many other parts.

China has long dominated the mining and processing of rare earth minerals, as well as the production of related components like rare earth magnets.

It mines about 70 percent of the world’s rare earths and processes approximately 90 percent of the supply. China also maintains near-total control over the supply of heavy rare earths, including dysprosium and terbium.

China’s hold over the industry had been a concern for the US and other countries for some time, but their alarm grew after Beijing imposed export controls in April.

The restrictions affected supplies of samarium, gadolinium, terbium, dysprosium, lutetium, scandium, and yttrium, and required companies shipping materials and finished products overseas to obtain export licences.

The restrictions followed a similar move by China in February, when it placed export controls on tungsten, bismuth and three other “niche metals”.

While news of a deal on rare earths signals a potential reprieve for manufacturers, the details of its implementation remain largely unclear.

What has been the impact of the export restrictions?

Chinese customs data shows the sale of rare earths to the US dropped 37 percent in April, while the sale of rare earth magnets fell 58 percent for the US and 51 percent worldwide, according to Bloomberg.

Global rare earth exports recovered 23 percent in May, following talks between US and Chinese officials in Geneva, but they are still down overall from a year earlier.

The greatest alarm has been felt by carmakers and auto parts manufacturers in the US and Europe, who reported bottlenecks after working their way through inventories of rare earth magnets.

“The automobile industry is now using words like panic. This isn’t something that the auto industry is just talking about and trying to make a big stir. This is serious right now, and they’re talking about shutting down production lines,” Mark Smith, a mining and mineral processing expert and the CEO of the US-based NioCorp Developments, told Al Jazeera.

Even with news of a breakthrough, Western companies are still worried about their future access to rare earths and magnets and how their dependence on China’s supply chain could be leveraged against them.

The Financial Times reported on Thursday that China’s Ministry of Commerce has been demanding “sensitive business information to secure rare earths and magnets” from Western companies in China, including production details and customer lists.

What have the US and China said about rare earth exports?

Trump shared some details of the agreement on his social media platform, Truth Social, where he also addressed concerns about rare earths and rare earth magnets.

“We are getting a total of 55% tariffs, China is getting 10%. The relationship is excellent,” Trump said, using a figure for US duties that includes levies introduced during his first term.

“Full magnets, and any necessary rare earths, will be supplied, up front, by China. Likewise, we will provide to China what was agreed to, including Chinese students using our colleges and universities (which has always been good with me),” Trump said.

Ahead of the negotiations in London, China’s Ministry of Commerce had said it approved an unspecified number of export licences for rare earths, and it was willing to “further strengthen communication and dialogue on export controls with relevant countries”.

However, an op-ed published by state news outlet Xinhua this week said rare earth export controls were not “short-term bargaining tools” or “tactical countermeasures” but a necessary measure because rare earths can be used for both civilian and military purposes.

NioCorp Developments’ Smith said Beijing is unlikely to quickly give up such powerful leverage over the US entirely.

“There’s going to be a whole bunch of words, but I really think China is going to hold the US hostage on this issue, because why not?” he said.

“They’ve worked really hard to get into the position that they’re in. They have 100 percent control over the heavy rare earth production in the world. Why not use that?”

Deborah Elms, the head of trade policy at the Hinrich Foundation in Singapore, said it was hard to predict how rare earths would be treated in negotiations, which would need to balance other US concerns like China’s role in exporting the deadly opioid fentanyl to the US.

Beijing, for its part, will want guarantees that it can access advanced critical US technology to make advanced semiconductors, she said.

Gold Price Forecast: XAU/USD rallies hard as Israel-Iran conflict sparks flight to safety

Gold price is gaining roughly 1.50% in Asian trading on Friday, underpinned by intense flight to safety amid escalating geopolitical tensions between Israel and Iran.

Gold price looks to record highs at $3,500

Israel said earlier on that it attacked Iranian nuclear targets to block Tehran from developing atomic weapons.

Several Iranian media outlets now claim that Iran will declare a war on Israel and retaliate "soon."

Iran's Armed Forces General staff responded on Friday, warning that Israel and the US will "pay a very heavy price".

Against this backdrop, US President Donald Trump has convened a meeting of the National Security Council in the White House situation room later in the day at 15 GMT.

Investors run for cover in the traditional safe-haven assets such as Gold price, the US Treasury bonds and the Japanese Yen (JPY) in times of market panic and uncertainty.

Therefore, the ultimate store of value, Gold price, is seeing unabated demand as it extends its winning streak into a third consecutive day on Friday, sitting at the highest level in seven weeks.

Gold buyers now aim for the record high of $3,500 if the Mid East conflict intensifies, with Iran initiating a harsh response to the Israeli pre-emptive strikes on Iran’s main enrichment facility in Natanz.

However, the strengthening haven demand for the US Dollar (USD) could impede Gold price rally.

Markets shrug off the latest trade headlines as geopolitics dominate alongside risk-off flows.

Reuters reported that tariffs on a range of imported household appliances, which are currently at 50% for most countries, would take effect on an additional range of “steel derivative products” on June 23.

Looking ahead, all eyes will remain on Iran’s probable retaliation to the Israeli strikes and the US’ response to the Middle East conflict.

The University of Michigan (UoM) Consumer Sentiment and Inflation Expectations could play second fiddle to the geopolitical headlines.

Markets ramp up odds for a US Federal Reserve (Fed) interest rate cut in September following softer-than-expected US Consumer Price Index (CPI) and Producer Price Index (PPI) data released earlier in the week.

Gold price technical analysis: Daily chart

Having closed Thursday above the critical resistance at $3,377, the 23.6% Fibonacci Retracement (Fibo) level of the April record rally, Gold price solidified its bullish momentum on Friday.

The 14-day Relative Strength Index (RSI) holds firm above the midline, currently near 62, suggesting that there is more room for the upside.

The next stiff resistance is spotted at the $3,450 psychological level, above which the lifetime high of $3,500 will be threatened.

On the downside, the immediate support is aligned at the $3,400 threshold, below which the resistance-turned-support of the 23.6% Fibo level at $3,377 will come into play.

Deeper declines will likely challenge the 21-day Simple Moving Average (SMA) of $3,325.

By Tsvetana Paraskova - Jun 13, 2025, 6:00 AM CDT

The plans of many EU countries to boost nuclear power capacities will need an investment of as much as $278 billion (241 billion euros), according to estimates by the European Commission.

Many EU countries have drafted plans to increase nuclear power capacity or even return to nuclear energy after decades of no nuclear generation, as they look to reduce imports of fossil fuels and meet emissions reductions and net-zero goals with more nuclear power.

Some EU countries have started considering a return to nuclear power after four decades—the latest examples include Denmark and Italy, which are looking at small modular reactors (SMRs) to complement their renewable energy generation.

Now, the European Commission is preparing an update to its Nuclear Illustrative Programme (PINC) to estimate the investment needs of the nuclear power sector in the EU.

In a draft of the analysis reported by Reuters on Friday, the Commission says that the EU member states have so far laid out plans to expand their nuclear power capacity to 109 gigawatts (GW) by 2050, up from 98 GW at present.

The expansion will need $237 billion (205 billion euros) in investments in new nuclear power generation capacity, as well as $42 billion (36 billion euros) in investments to extend the lifespan of operating reactors. The investment includes both public and private funds, according to the European Commission’s estimates.

Germany, which has been opposing for years EU attempts to treat nuclear power as a green electricity source on par with renewable energy, has dropped this opposition under new chancellor Friedrich Merz, which could make EU energy policy much easier to adopt.

Since the 2022 energy crisis, Germany and France have clashed on how nuclear energy should be treated in the green transition in the EU.

Now, Merz’s Germany appears to be shifting its anti-nuclear stance on EU energy policies, French and German officials told the Financial Times last month.

By Tsvetana Paraskova for Oilprice.com

German Chancellor Friedrich Merz, together with the leaders of France and the United Kingdom, promised to impose tough sanctions on Russia if it did not agree to a ceasefire with Ukraine. But he did not keep the promise, thereby undermining trust in Europe, believes Lithuanian President Gitanas Nausėda, according to Bild .

"This is a problem. And it affects not only trust in our sanctions but also trust in all our measures toward Russia and our support for Ukraine. We have repeatedly announced that we will support Ukraine and supply fighter jets, long-range missiles, and ammunition. But we are unable to fulfill these promises," Nausėda said in an interview with Bild.

According to him, the sanctions that have already been imposed on Russia since February 2022 have not had the effect the West expected. First, the sanctions were not decisive enough, and second, third countries are helping Russia to circumvent them.

"That is why the Russian economy, although not in the best condition, still functions relatively well under these circumstances," the Lithuanian leader said.

Currently, the European Union is preparing its 18th package of sanctions against Russia, and Lithuania is demanding that it "resemble a Molotov cocktail." As Nausėda said, it means the package must include all energy companies that supply money to the Russian state budget: Nord Stream, Rosatom, Gazprom, Lukoil.

"The remaining Russian banks must also be excluded from the SWIFT system, as well as the rest of the shadow fleet vessels. Otherwise, we will be seen as weak and perceived as if Europe is unwilling to make bold decisions," he stressed.

Sanctions against Russia

During a visit to Kyiv in May, the leaders of Germany, France, and the United Kingdom gave Russia a deadline to agree to an unconditional 30-day ceasefire with Ukraine. In the event of non-compliance, the countries threatened to impose tough sanctions.

The final day for agreeing to a ceasefire was Monday, May 12. Moscow did not comply with this demand, but Germany has yet to impose punitive measures.

At the beginning of June, German Defense Minister Boris Pistorius once again announced the upcoming tough sanctions against Russia.

https://newsukraine.rbc.ua/news/lithuanian-president-slams-broken-promise-1749373411.html

Marler Clark retained by California woman likely sickened by Salmonella-tainted eggs

Seattle, WA – As of June 5, 2025, a total of 79 people infected with Salmonella Enteritidis have been reported from 7 states (Arizona 3, California 63, Kentucky 1, Nebraska 2, New Jersey 2, Nevada 4, Washington 4). The attorneys at Marler Clark have been hired by one of the likely California victims in this outbreak. Health officials in California and other states are continuing to investigate this outbreak and have determined that there is a link to August Egg Company, based in Hilmar, California. 1.7 million eggs have been recalled from multiple states.

Outbreak Facts

Illnesses started on dates ranging from February 24, 2025, to May 17, 2025. Of the 61 people with information available, 21 have been hospitalized. No deaths have been reported.

Epidemiologic, laboratory, and traceback data show that eggs distributed by August Egg Company may be contaminated with Salmonella Enteritidis and may be making people sick. On June 6, 2025, August Egg Company recalled eggs. Egg Recall list.

The recalled eggs were sold at grocery stores in California and Nevada, including FoodMaxx, Lucky, Raleys, Ralphs, Safeway, Food 4 less, Save Mart and Smart & Final. They were also sold at Walmart stores in Arizona, California, Illinois, Indiana, Nebraska, Nevada, New Mexico, Washington and Wyoming.

90% of those interviewed recalled eating eggs. State health officials have identified illness sub-clusters at two unnamed restaurants. Eggs were served at both sub-cluster locations.

Six ill people from Kentucky, New Jersey, and Washington reported traveling to California and Nevada before they got sick.

Salmonella

“Given the lag time in reporting and broad sales of the eggs, this outbreak will increase in number over the coming weeks,” said Bill Marler, managing partner at Marler Clark. “In addition, the CDC estimates that for every one person counted, there are nearly 40 other sick but will remain uncounted,” added Marler.

William (Bill) Marler will be representing a California victim in this Salmonella egg outbreak. An accomplished attorney and national expert in food safety, Bill has become the most prominent foodborne illness lawyer in America and a major force in food policy in the U.S. and around the world. As an food safety expert, Bill is featured in the current Netflix documentary called Poisoned, the Dirty Truth About Your Food. Over the last 30 years, Marler Clark, The Food Safety Law Firm, has represented thousands of individuals in claims against food companies whose contaminated products have caused life altering injury and even death.

If you would like to speak with Bill Marler about this outbreak, please contact Julie Dueck at 206-930-4220 or jdueck@marlerclark.com.

By Adedapo Adesanya

Nigeria and Saudi Arabia are struggling to reach an agreement on a record $5 billion crude oil-backed loan, Reuters is reporting.

According to four sources which spoke with the publication, there were concerns among banks which would finance the deal due to recent decline in crude prices, which is trading around $67 per barrel.

At $5 billion, the Aramco loan would be backed by at least 100,000 barrels per day of oil, the sources said.

The facility would be Nigeria’s largest oil-backed loan to date and Saudi Arabia’s first participation of this scale in the country.

The decline in oil price could shrink the size of the deal, the sources said.

According to two of the sources, President Bola Tinubu broached the loan when he met with Saudi Crown Prince Mohammed bin Salman in Riyadh at the Saudi-African Summit in November 2023.

However, this is the first time that such conversation have been made public as the federal government didn’t announce any plans to the public.

According to Reuters, the slow progress in discussions reflects the strain of the recent oil price drop, caused largely by a shift in policy by the Organisation of the Petroleum Exporting Countries and allies, OPEC+ to regain market share rather than curtail supply.

The banks involved in the talks that are expected to co-fund part of the loan with Aramco, the state oil company of Saudi Arabia, have expressed concerns about oil delivery, which has slowed discussions.

It is believed that Gulf banks and at least one African lender are involved.

“It’s hard to find anyone to underwrite it,” one source said, citing concerns over the availability of the cargoes.

The report claimed that Nigeria is using at least 300,000 barrels per day to repay NNPC’s other oil-backed loans, adding that if the Saudi deal is reached, it would almost double the roughly $7 billion of loans taken in the last five years.

The amount of oil going towards repaying the loans is fixed, but when the crude price falls, it takes longer to repay them.

So when prices are lower, the Nigerian National Petroleum Company (NNPC) Limited has to funnel more crude oil to joint-venture partners like to Shell, Oando, and Seplat for its portion of operation costs.

Nigeria is having difficulties increasing its crude production to its set target of 2.5 million barrels per day and with prices lower than $70 per barrel at the international market, the country is finding it difficult to make enough revenue.

https://businesspost.ng/economy/nigeria-saudi-struggle-to-agree-on-5bn-crude-oil-loan/

European Commission President Ursula Von der Leyen proposed an 18th round of sanctions on Russia over the war in Ukraine

The move comes ahead of a G7 summit in Canada next week where allies will push US President Donald Trump to be more aggressive in punishing the Kremlin.

"We are ramping up pressure on Russia, because strength is the only language that Russia will understand," European Commission president Ursula von der Leyen said.

"Our message is very clear, this war must end. We need a real ceasefire, and Russia has to come to the negotiating table with a serious proposal."

The European Commission, the EU's executive, suggested cutting the current oil price cap from $60 to $45 as Moscow drags its feet on a ceasefire in Ukraine.

The cap is a G7 initiative aimed at limiting the amount of money Russia makes by exporting oil to countries across the world.

Set at $60 by the G7 in 2022, it is designed to limit the price Moscow can sell oil around the world by banning shipping firms and insurance companies dealing with Russia to export above that amount.

To have most impact the EU and other G7 partners need to get the United States to follow suit and agree to the cut in level.

But Trump so far has frustrated Western allies by refusing to impose sanctions on Russia despite President Vladimir Putin's failure to agree a Ukraine ceasefire.

"My assumption is that we do that together as G7," von der Leyen said. "We have started that as G7, it was successful as a measure from the G7, and I want to continue this measure as G7."

'Massive' sanctions threatened

Trump last week said he had a deadline to sanction Russia "in my brain", but warned that he may also target Kyiv if no advances are made in his peace push.

European leaders in May threatened Moscow with "massive" sanctions if it did not agree a truce.

"Russia lies about its desire for peace. Putin is taking the world for a ride. Together with the United States, we can really force Putin to negotiate seriously," EU foreign policy chief Kaja Kallas said.

As part of its 18th round of sanctions since Russia's 2022 invasion, the EU also proposed measures to stop the defunct Baltic Sea gas pipelines Nord Stream 1 and 2 from being brought back online.

Officials said they would also look to target some 70 more vessels in the "shadow fleet" of ageing tankers used by Russia to circumvent oil export curbs.

The EU in addition is looking to sever ties with a further 22 Russian banks and add more companies, including in China, to a blacklist of those helping Moscow's military.

One EU diplomat described the latest proposals as "one of the most substantive and significant packages we've discussed recently".

"It will hurt Russia's ability to finance its war machine. Now let's see how the discussions evolve."

The sanctions will need to be agreed by all 27 EU countries, and could face opposition from Moscow-friendly countries Hungary and Slovakia.

© 2025 AFP

Saudi Arabia's crude oil exports to China are expected to dip slightly in July, though volumes will remain robust for the third consecutive month, highlighting Riyadh’s determination to defend its market share in the world’s largest crude importer.

Trade sources reported Tuesday that Saudi Aramco will supply around 47 million barrels of crude to China in July, down marginally from 48 million barrels in June. Despite the one-million-barrel drop, the allocation remains high, signaling Saudi Arabia’s continued emphasis on maintaining a competitive edge in the Asian market.

Sources noted that Chinese state-owned refiners such as Sinopec, PetroChina, and Aramco’s Fujian joint venture will receive increased volumes next month. In contrast, supply to three independent refiners will be reduced, reflecting a strategic pivot toward long-term partners.

The slight adjustment follows Aramco’s recent decision to lower the official selling price of its flagship Arab Light crude by 20 cents per barrel for Asian buyers starting in July. The grade will now be priced at $1 above the regional benchmark, a move analysts say is aimed at protecting Saudi Arabia’s foothold in a crowded and competitive market.

Saudi Arabia faces mounting pressure from rival suppliers such as Russia and Iran, both of which are seeking to expand their presence in the Chinese energy market by offering discounted barrels and flexible terms.

China, which imported more than two-thirds of its crude in 2024, remains a critical market for Aramco. The company continues to prioritize securing long-term contracts and stable supply flows despite ongoing geopolitical uncertainty and shifts in global demand.

https://oilprice.com/Company-News/Saudi-Aramco-To-Send-Less-Crude-to-China-in-July.html

Most countries in the Group of Seven nations are prepared to go it alone and lower the G-7 price cap on Russian oil even if U.S. President Donald Trump decides to opt out, four sources familiar with the matter said.

G-7 country leaders are due to meet on June 15-17 in Canada where they will discuss the price cap first agreed in late 2022. The cap was designed to allow Russian oil URL-E to be sold to third countries using Western insurance services provided the price was no more than $60 a barrel.

The European Union and Britain have been pushing to lower the price for weeks after a fall in global oil prices made the current $60 cap nearly irrelevant.

The sources, who declined to be named, said the EU and Britain are ready to lead the charge and go it alone, backed by the other European G-7 countries and Canada.

They said it is still unclear what the U.S. will decide, though the Europeans are pushing for a united decision at the meeting. Japan’s position also remains uncertain, they said.

“There is a push among European countries to reduce the oil price cap to $45 from $60. There are positive signals from Canada, Britain and possibly the Japanese. We will use the G-7 to try to get the U.S. on board,” one of the sources said.

The White House had no immediate comment. During the G-7 finance ministers meeting in the Canadian Rockies last month, U.S. Treasury Secretary Scott Bessent remained unconvinced there was a need to lower the cap, according to sources.

However some U.S. Senators may endorse the idea, including Lindsay Graham, who in recent weeks told reporters he supports lowering the cap. Graham is pushing a hard-hitting new set of Russia sanctions that could impose steep tariffs on buyers of Russian oil.

The EU has proposed lowering the price to $45 a barrel in its latest 18th package of sanctions. The package must have unanimity from member states in order for it to be adopted, which could take several weeks.

Russia’s largest export grade, Urals, trades at around a $10 a barrel discount to the Dated Brent benchmark BFO-URL-NWE out of Baltic ports. Brent futures have been trading below $70 a barrel since early April.

Sources said Washington’s buy-in was not essential to lower the cap owing to Britain’s dominance in global shipping insurance, and the EU’s influence on the Western rules-abiding tanker fleet.

The U.S., however, does matter when it comes to dollar-denominated payments for oil and its banking system.