Daniel Andrews has said: “every job is worth fighting for” and that “every government needs to ensure that every job stays here in Australia.”

Ms Britnell says “The smelter is an integral part of the south-west’s economy and I will do everything in my power to support Alcoa to ensure it has a future in Portland."

“There is a strong worldwide demand for aluminium and Portland’s smelter has a history of strong performance and has a massive part to play in Victoria’s economy – there’s no question it needs to remain."

“The policies of the Andrews Labor Government have forced electricity prices sky high, and placed enormous pressure on the business.”

“Daniel Andrews can’t sit on his hands, he must act and support Alcoa to make the Portland smelter is sustainable.”

“The potential closure of the Portland smelter would be devastating for the community, the Premier must step up and work with Alcoa to ensure ongoing sustainability and drive down energy costs.”

“Daniel Andrews and his Melbourne-centric government have ignored regional Victoria for too long, he can’t simply wash his hands of this, he must step up to the plate and support the Portland community.”

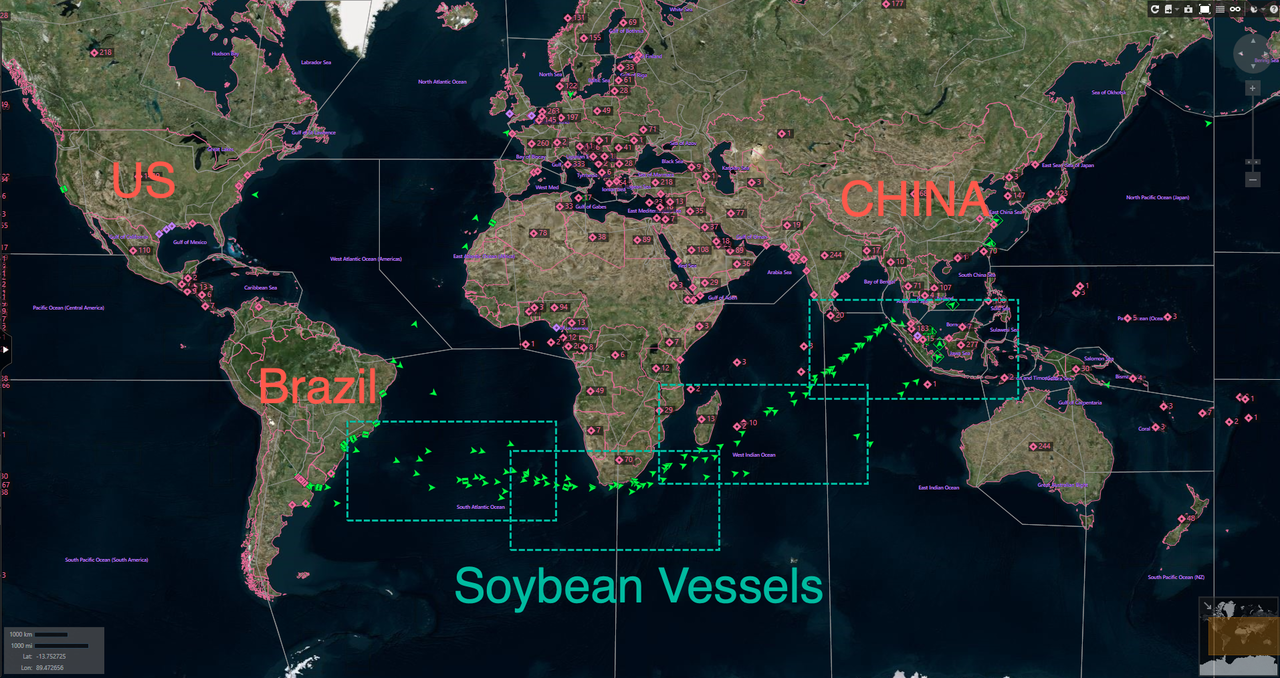

After trade talks in U.S., China ramps up Brazilian soy purchases

Chinese importers have been busy booking fresh purchases of soybeans from Brazil this week, despite the White House announcement that China had agreed to buy up to $50 billion of U.S. farm products annually during trade talks last week.

Two traders said China has booked at least eight boatloads, or 480,000 tonnes worth $173 million, of Brazilian soybeans since Monday.

While Brazil is China’s largest soybean supplier, large purchases from Brazil are unusual at this time of year.

The lack of purchases from the United States so far this week shows China is in no hurry to buy U.S. products in the wake of last week’s phase one trade agreement, that U.S. President Donald Trump hopes will be signed next month.

Trump said on Twitter on Sunday that China has already begun making U.S. agricultural purchases. But three U.S. soybean exporters said there have been no U.S. sales to China since last week’s talks in Washington, and none have been confirmed by the U.S. Department of Agriculture.

“I’ve not had any inquiries at all for U.S. (shipments),” said one of the U.S. soybean exporters. “There were a few November boats bought from Brazil and several new-crop South American boats for March forward but nothing here.”

Another U.S. exporter said a drop in Brazilian soybean prices sparked fresh demand from commercial soy importers that have been unable to profitably import American soybeans for more than a year unless given tariff waivers.

State-owned firms COFCO and Sinograin, which are exempt from the 25% retaliatory duties on U.S. imports, have “little appetite” to buy unless U.S. prices drop further, the second U.S. exporter said.

Before the trade war, China imported most of its U.S. soy between October and January, turning to South America around February.

Prices for U.S. soybeans loaded at Gulf Coast terminals in November and December and shipped to China are now near par with Brazilian soy prices. But when prices for soybeans from the two top suppliers are similar, Chinese importers tend to favor Brazilian beans due to their higher average protein content.

Chinese importer Hopefull Grain & Oil bought 10 cargoes of Brazilian soy last week ahead of U.S.-China talks and at least 3 cargoes this week, two of the trade sources said.

Wilmar was also a buyer, with about 5 to 6 cargoes purchased from Brazil this week, according to a U.S. exporter and two traders, one of whom was based in Beijing while the other worked for a Chinese trading house.

Both Hopefull and Wilmar declined to comment.

The companies are believed to have used up their waivers for tariff-free U.S. purchases in recent waves of buying, a U.S. exporter and a Chinese importer said.

White House economic adviser Larry Kudlow acknowledged on Thursday that China’s “serious commitment” to buy up to $50 billion of agricultural products would depend in part on private companies and market conditions.

Soybeans are one of the leading agriculture products that the U.S. exports to China -- so when Trump touts "China Is Purchasing U.S. Agricultural Products Now," one would expect to see a whole bunch of soybeans -- but as the one trader said, China abandoned the U.S. market for Brazil.

Also, check out a vessel map from Saturday, each green dot is a bulk carrier hauling soybeans. Notice how there is just one bulk carrier transporting soybeans off the East Coast, while dozens and dozens of vessels are traversing back and forth from Brazil and China.

https://www.zerohedge.com/markets/trump-touts-china-buying-agriculture-products-traders-firmly-disagree

Another year, another portfolio review by Alcoa.

The U.S. aluminium producer has just announced a five-year review of around 4.0 million tonnes of alumina capacity and 1.5 million tonnes of smelter capacity.

Assets will be improved, curtailed, closed or sold.

It’s not quite an annual event but Alcoa shareholders have been here many times before as the company keeps trying to move down the cost curve in the face of chronically depressed prices.

On the London Metal Exchange (LME) three-month aluminium has ground steadily lower over the course of 2019 and at a current $1,720 per tonne is close to the near three-year low of $1,705 recorded earlier this month.

This time around, however, Alcoa is throwing an extra ingredient into the cost-cutting mix - sustainability.

The company “expects to be the lowest emitter of carbon dioxide among all global aluminium companies”.

Going green is the new differentiator in the cut-throat business of making aluminium.

GREEN POWER

Aluminium is one of the metals expected to benefit from the “green revolution” given its recyclability and light-weighting potential in the automotive sector.

However, its green credentials have recently come in for some serious scrutiny.

The part suspension of the Alunorte alumina refinery in Brazil last year and closures in China this year have served as a reminder that aluminium has its own tailings dam issues, a sensitive topic after the devastating dam failure at Vale’s Brumadinho iron ore mine.

Moreover, aluminium is only as “green” as the power source used to make the stuff, particularly since power is such an important input in the aluminium smelting process.

Alcoa is hoping to leverage its existing strengths on both fronts.

Its entire production chain is certified by the Aluminium Stewardship Initiative, it boasts “the lowest carbon footprint of any (alumina) refining system in the world” and is one of the lowest emitters among major aluminium producers.

Around 70% of the electricity powering its smelters comes from renewable sources, a ratio that Alcoa hopes will rise to around 85% after its portfolio review.

BLACK ALUMINIUM

Alcoa has the advantage of being based in North America, which thanks to Canada’s massive hydroelectric dam system has one the highest renewable energy profiles of any major producing region.

Hydro power accounted for 82% of North American aluminium production last year, according to the International Aluminium Institute (IAI).

Latin America was close behind with 77%, albeit with a much smaller smelter network.

In Europe hydro power fed 75% of aluminium production last year. Rusal’s giant Siberian smelters are an important part of that calculation.

If these are the “green” aluminium production hubs, the “black” ones are in China, the world’s largest producing nation, and in the rest of Asia. Hydro powered around 10% of aluminium output in each region last year with coal accounting for the rest, according to the IAI.

Coal is a particularly problematic source of power for any metal that wants to claim it is environmentally sustainable.

Chinese producers are increasingly reacting to this emerging power-source differentiation in the aluminium production sector.

Hongqiao Group, the country’s largest producer, last week announced it will take the lead in developing a “green aluminium” industrial park in Yunnan, a Chinese province rich in hydropower resources.

It will follow a trail blazed by other Chinese producers such as Chalco and Henan Shenhuo, which have also been building out “green” capacity in Yunnan.

Since most Chinese producers are prohibited from building more aluminium production capacity, new plants in Yunnan are replacing older, coal-powered smelters in heavily industrialized provinces such as Shandong.

But while part of the country’s aluminium production is migrating to hydro-rich provinces, another part is locked into stranded coal deposits in the northwestern provinces.

That means the evolving green-black aluminium differentiation is not going to go away any time soon.

HOW MUCH TO GO GREEN?

The question is whether sustainable “green” aluminium will end up commanding a financial premium over non-green metal.

Is differentiation a mere branding exercise or can it be a financial driver as well?

“We have a series of products right now that are either focused on being low-carbon or being made on a certain amount of recyclable material (...) that have been able to command a premium in the market-place,” according to Roy Harvey, Alcoa President and Chief Executive Officer.

However, Harvey conceded on the company’s quarterly earnings call that “this is just a nascent market” which will “take time to develop.”

Alcoa hopes that what is a niche market today becomes a global market tomorrow.

Alcoa’s sustainability message is, according to Harvey, “something that is a natural addition and is in fact the way that Alcoa’s succeeds into the future because we do the right thing and because at some point the market recognizes that is value in that responsibility.”

BATTLEGROUND

The aluminium industry is just at the start of its own green revolution.

It is being driven by producers such as Alcoa, Rusal and Norway’s Hydro, all of which already enjoy high renewable energy inputs into their smelters.

The next phase will be the evolution of the smelting process itself.

Alcoa and Rio Tinto have formed a joint venture, ELYSIS, to commercialize a smelting process that generates oxygen and eliminates all direct greenhouse gas emissions.

The aim is to have a technology package for sale in 2024, either for retrofitting existing smelters or building new greenfield plants.

Apple is also part of the joint venture, a clear sign of the interest from consumer groups in ensuring their metal ticks all the sustainability boxes.

It’s just part of a bigger technological rethink by aluminium products.

Rusal, for example, is working on ways of converting waste such as “red mud” into saleable products. Its Sayanogorsk smelter site already processes or sells over 90% of the waste produced and the goal is to move the rest of the company’s smelters up to a similar ratio.

Expect similar announcements from other producers to follow.

The concept of “green” aluminium is only a couple of years old but sustainability looks set to be a defining feature of this market for years to come.

https://www.oaktreecapital.com/insights/howard-marks-memos

suggested I write a memo about negative interest rates. My reaction was immediate and unequivocal: “I can’t. I don’t know anything about them.” And then I realized that’s the point. No one does.

MGL: Must reading.

MGL: Above average.

MGL: Permian prices collapse again, post the 2bcf add to pipe capacity?

Many privately held firms in Shandong, China’s third-biggest province by economic output, are struggling to repay short-term debt due to declining industry fundamentals, entangled cross guarantees and ill-managed investments, S&P Global Ratings said.

China’s slowing economy and enforcement of environmental protection rules have pressured the profitability and cash flow of Shandong companies in over-capacity sectors including oil refining, petrochemicals, steel, aluminium and textiles, S&P said.

“The Shandong economy is skewed toward gritty smoke-stack industries where companies are typically highly leveraged,” said Chang Li, China country specialist for S&P Global Ratings.

“We view the plight of Shandong POEs (privately owned enterprises) as indicative of China’s wider challenge: the difficulty of transitioning to a higher value-added economy, while managing high debt and slowing growth.”

Private firms in Shandong are also frequent users of the cross guarantee, which has the potential to send one company’s liquidity problems reverberating through the credit system, the ratings agency said.

Reuters reported in February, citing court rulings, that at least 28 private companies in Dongying, a hub for oil refining and heavy industry in Shandong, are seeking to restructure their debts and avoid bankruptcy, mainly due to souring loans that they guaranteed for other firms.

For a private firm to get bank loans in China, especially those in traditional, capital-intensive industries, it often needs substantial collateral or the guarantee of another company. The guarantor itself is very likely to have taken on loans guaranteed by other firms.

Complicating the situation is the weak transparency of these companies in disclosing their full exposures, potentially creating vicious cycles where complex cross guarantees spread solvency risks to the entire region, swamping the good credits along with the bad.

“We foresee no immediate relief to Shandong’s POE liquidity and refinancing challenges given China’s slowing economy. We expect Shandong POE credit risk will remain significant for the next 12 months,” S&P said.

The ratings agency added that Shandong’s support will be limited, as the provincial government has been favouring high-value-added sectors in recent years, and may not mind letting some private firms in over-capacity industries go under, if there is no systemic risk.

Miner Anglo American (AAL.L) said on Tuesday it was on track to meet annual output targets after production rose 4% in the third quarter, driven by a ramp up at its Minas-Rio mine in Brazil and rise in coking coal production.

Minas-Rio, one of Anglo’s biggest growth projects that was suspended last year, is expected to produce 20-22 million tonnes of iron ore in 2019, up from previous expectations of 19-21 million tonnes, the company said.

Production of iron ore at Minas-Rio was 6.1 million tonnes, and metallurgical coal jumped 22% to 6.6 million tonnes in the quarter ended Sept. 30, the company said.

Miner Anglo American said copper and thermal coal production would be at the lower end of their guidance ranges after output increased 4% in the third quarter of the year, as a fall in copper, coal and diamond production kept a lid on growth.

Still, the company said it remained broadly on track to deliver within its full-year production targets, with an increase in production guidance at Minas-Rio.

Copper production decreased by 8% to 158,900 tonnes due to unprecedented drought conditions impacting Los Bronces in Chile.

Copper production guidance was tightened to a range of 630,000 to 650,000 tonnes (previously 630,000 to 660,000 tonnes) due to the severe drought, which also remained a risk for 2020 production, the company said.

Production guidance for export thermal coal was tightened to about 26m tonnes from a range of 26m to 28m tonnes due to lower than expected production from Cerrejón, the company added.

De Beers' diamond production decreased by 14% to 7.4m carats due to planned mine closures and the underground transition at Venetia. Production guidance was unchanged at about 31m carats.

As per usual, a soft pound gave a fillip to blue-chips

5.15pm: FTSE 100 in positive finish

FTSE 100 closes up around 50 points Pound weakened as prospect of a 2019 General Election looms Just East surges to Footsie podium

FTSE 100 index closed higher on Tuesday, aided by the decline in sterling and as traders await the next vote on Brexit in parliament.

Expected is a key vote around 7.30pm on the Commons debate timetable on the latest Brexit plan. Word is that Prime Minister Boris Johnson will call for a general election if MPs don't back the proposed three day timetable.

The Footsie finished up 50.85 points at 7,214.59.

But the more UK -company focused FTSE 250 plunged 108 points to stand at 20,200.79.

The pound lost 0.11% to 1.2946 against the US dollar.

"Pound traders are broadly opting to stay on the side-lines rather than guess the outcome of today’s voting," said Fiona Cincotta, market analyst at City Index.

She added: "Should the House of Commons reject the idea of pushing the legislation through in just 3 days, Bojo’s Brexit bill could potentially under much more scrutiny. This opens up the probability of a more drawn out Brexit. This would also give the opposition ore time to get their act together and push for an election or second referendum."

Top riser on FTSE 100 was take-away app Just Eat (LON:JE.) which gained a stonking 24.19% to 732p as a bidding war looms as it rejected a hostile £4.9bn bid from investment firm Prosus in favour of a £8.4bn merger with Dutch rival Takeaway.com.

4pm: Footsie clings to gains

Having entered the final hour of trading, the Footsie has been engaged in holding its station, clinging on to earlier gains.

London's top-shares index was up 45 points (0.6%) at 7,208, some 12 points off its intra-day high and almost 70 points above its low.

Sterling has now lost almost half a cent today to US$1.2916 as traders remain on alert for a General Election to be called if Parliament does not pass the withdrawal agreement bill (WAB).

Pound gets Brexit butterflies as Johnson talks up election; investors hungry for Just Eat... https://t.co/ODdoMSLCvt$JE $GBP #Brexit #WAB #sterling #pound

— Connor Campbell (@Connor Spreadex

“As tension builds ahead of this evening’s votes on the Brexit withdrawal agreement bill, the pound lost a step on Tuesday afternoon,” reported Connor Campbell at Spreadex.

“The currency’s stoic open was gradually chipped away at as the day went on. Now sterling is down 0.4% against the dollar and 0.3% against the euro, tripping away from Monday’s fresh 5-month highs. Not only is it feeling nervy pre-vote, it is also dealing with the re-raised spectre of a general election,” Campbell added.

“Boris Johnson has threatened to pull the WAB if MPs decline his timetable in Tuesday’s 2nd vote, and instead seek to send the public to the polls pre-Christmas (this is as long as the EU would grant a 3-month extension as requested by the Benn act),” he said.

Wells Fargo Economics reckons there is a “better-than-ever” chance the bill will be ratified in the next few days; possibly it meant “better-than-even” chance.

“Given the challenges negotiators are likely to face in the coming years as they work to agree on a new trading arrangement, we think most of the Brexit optimism will be front-loaded in the next few weeks,” the economics group predicted.

3.00pm: FTSE 100 kicks on as sterling tumbles on General Election fears

The FTSE 100 has kicked on after sterling took a tumble on foreign exchange markets.

A Downing Street source has been quoted as saying, “if Parliament votes again for delay by voting down the programme motion, and the EU offers delay until 31 Jan -- then we will pull the Bill, there will be no further business for Parliament and we'll move to an election before Christmas”.

The FTSE 100, which usually receives a fillip from a weak exchange rate, climbed above 7,200 to 7,209, up 46 points (0.6%) on the day as sterling fell to US$1.2929, down a third of a cent.

STERLING FALL CAUSED BY BBC POLITICAL EDITOR TWEET THAT GOVT WILL PULL BREXIT LEGISLATION AND PUSH FOR ELECTION IF LAWMAKERS VOTE DOWN BILL

— Quantitative Trading (@fiquant) October 22, 2019

Not sure he will spell it out at the despatch box, but it seems if MP s won't agree govt timetable for Brexit legislation tonight, they will pull it, and if EU then offers a delay, they would push straight for an election instead

— Laura Kuenssberg (@bbclaurak) October 22, 2019

Sterling's stumble lifted spirits a bit after what Howard Archer of the EY ITEM Club called “a dismal October CBI industrial trends survey”.

“There is not even any sign of manufacturers getting a temporary boost in October from increased stock-building ahead of the 31 October Brexit deadline. The balance for stocks of finished products fell back to a six-month low of +11% in October after jumping to +28% in September (the highest since May 2009) from +14% in August,” Archer reported.

“The survey shows the orders balance fell to -37% in October, which was the weakest level since March 2010. It was down from -28% in September and -13% in August, and substantially below the long-term average of -13%,” Archer observed.

“The simultaneously released CBI quarterly survey showed that confidence among manufacturers was the lowest since July 2016. Specifically, the business optimism index weakened to -44% from -32% in July. Manufacturers were particularly downbeat about export prospects (the lowest since October 2001),” he added.

Meanwhile, in the US, the Dow Jones is more or less unchanged while the broader-based S&P 500 is up 5 points (0.2%) at 3,012.

1.40pm: Blue-chips consolidate gains

The Footsie remained in positive territory ahead of what is expected to be a modestly firmer start on Wall Street.

London’s index of blue-chip shares was up 34 points (0.5%) at 7,197.

Across the pond, while the Dow Jones is expected to open 5 points lower at 26,822 – weighed down by negative sentiment towards fast-food giant McDonalds after an earnings miss – the S&P 500 is tipped to start 4 points higher at 3,011.

In the UK, the CBI’s total orders balance dropped to -37 in October from -28 in September. Economists had pencilled in a figure of -30.

“Manufacturers appear to be experiencing the full force of the global downturn and aren’t enjoying any relief this time from preparations ahead of the October Brexit deadline,” observed Samuel Tombs at Pantheon Macroeconomics.

“Granted, the total orders balance is not seasonally adjusted and it has fallen by an average of six points over the last 42 years. Nonetheless, our seasonally adjusted version of the balance also dropped in October and points to manufacturing output falling at a 4% year-over-year rate soon. In addition, the quarterly business optimism balance dropped to the lowest level since July 2016, while all three investment intentions balances, relating to building, machinery and training, fell to their lowest levels since the financial crisis,” he added.

12.05pm: Just Eat share price super-sizes

Led by Just Eat PLC (LON:JE.), the FTSE 100 has reversed track and hurtled into positive territory.

London's index of leading shares was up 35 points (0.5%) at 7,199, thanks in part to a 25% increase in the share price of Just Eat after the online takeaway giant received a hostile takeover bid from a company owned by South African e-commerce giant Naspers.

The shares are trading at around 735p, 25p above Naspers’ offer price, which suggests the market is expecting a bidding war to ensue, as Just Eat management had previously agreed to a merger with the Dutch company, Takeaway.com.

“The 710p cash offer from Prosus is a 20% premium to the Takeaway.com offer and about 12% higher than the shares were trading before the latter’s bid. Always a strong possibility given the increasingly low-ball offer from Takeaway.com, a bidding war is now on. You may need more like 750p to sort this out,” suggested Neil Wilson.

Today’s borrowing figures put PSNB at £40.3bn in the first half of 2019-20, up 22% on the same period in 2018-19. But back at the Spring Statement, the OBR projected that full-year borrowing would reach £40.6bn (adjusting for student loans), down v slightly on the 2018-19 total pic.twitter.com/sKN0l3GGlQ

— Matt Whittaker (@MattWhittakerRF) October 22, 2019

On the macro front, the public sector net borrowing excluding public sector banks – “PSNB ex.” in the jargon – rose to £9.4bn in September from £8.8bn the year before but was below the consensus forecast of £9.7bn.

“September’s relatively small increase in borrowing leaves the public finances looking a little healthier than before, though the government still is on course to exceed next year’s 2% of GDP [gross domestic product] borrowing limit,” said Samuel Tombs, the chief UK economist at Pantheon Macroeconomics.

“No political appetite exists for further austerity measures to reduce the deficit. Indeed, the Chancellor allocated in last month's Spending Round an extra £12bn to departments to spend in 2020/21, over and above that already planned for in the Spring Statement, while both parties will pledge giveaways to the electorate in the election likely to be held in the coming months. If the next Budget is held as currently planned on November 6, voters can expect pre-election sweeteners from the Conservatives,” Tombs declared.

Also on the home front – literally, in this case – the provisional seasonally adjusted estimate of UK property transactions for September was 101,740 residential and 10,500 non-residential transactions.

The provisional seasonally adjusted count of residential property transactions in September was 2.3% higher than in September 2018 and 5.0% higher than in August 2019, Her Majesty’s Revenue & Customs revealed.

The provisional seasonally adjusted count of non-residential property transactions in September was 0.2% higher than in September 2018 and 7.7% higher than in August 2019.

“A seasonally inspired spike in transactions will be welcomed across an otherwise weary market landscape and while uncertainty continues to dominate the property sector, this late rally in the number of homes being sold proves there is plenty of life in the old dog yet,” ventured Shepherd Ncube, the chief executive officer of Springbok Properties.

“There remains a huge appetite for home ownership across the UK and while transactions may have plateaued in recent years they have remained consistently stable, with pent up demand from homebuyers occasionally giving way in the form of a monthly spike in sales,” he added.

Property listings website operator Rightmove PLC (LON:RMV) was heartened by the news and added 12p to yesterday’s gains to advance to 581.8p.

Yesterday, Rightmove reported that house prices are rising at their lowest rate in October since 2008, climbing 0.6% while property listing numbers are down 13.5% on levels seen a year ago.

10.00am: Stocks chug lower

London's leading shares are lower on balance as traders await the outcome of Boris Johnson's “one more heave” to get Brexit over the line.

The FTSE 100 was down 14 points (0.2%) at 7,150, with travel firm TUI AG (LON:TUI), down 5.1% at 1,012.5p, leading the retreat after Morgan Stanley cut its rating on the stock to “equal weight”.

Also under the cosh is Reckitt Benckiser PLC (LON:RB.) after it slashed full-year sales guidance in its third-quarter trading update.

The Anglo-Dutch fast-moving consumer goods giant's shares were down 5.0% at 5,577p.

Anglo-American PLC (LON:AAL), up 1.3% at 1,965.2p, was the top-performing blue-chip after its third-quarter production update.

Whitbread plc (LON:WTB) was another stock on the rise, hardening 0.8% to 4,238p, after its interims.

“Now without the significant buttress of the Costa business, Whitbread is finding life tough,” declared Richard Hunter, the head of markets at interactive investor.

“Whitbread’s reliance on the hotels market makes the company less diversified and therefore more vulnerable to economic swings. The shares have underperformed of late, having declined 13% over the last six months and 7% over the last year, the latter of which compares to a 1.7% increase in the wider FTSE100. With the real potential of economic clouds on the horizon, the market consensus of the shares has now swung to a sell in the absence of any sustained cheer from the company,” Hunter noted.

8.45am: Stuttering start ahead of the Withdrawal Agreement Bill

The FTSE 100 made a stuttering start to proceedings with caution the watchword ahead of Boris Johnson’s final bid get the UK out of the EU by the end of the month.

Later Tuesday, MPs will be asked to back the Prime Minister’s Withdrawal Agreement Bill. If Johnson is successful, and at this stage, it is still a big ‘if’, the Commons will be asked to approve an intensive three-day timetable in which to consider the legislation.

“There are yet plenty of hurdles for the government to clear after winning the vote that will keep traders mindful of downside risks,” said Neil Wilson, an analyst at Markets.com.

The morning’s big mover was Reckitt Benckiser (LON:RB.), which cut its sales target after a dour third-quarter update. The shares fell 4.5%.

On the upside, there was a recovery from recent lows for the miners led by Antofagasta (LON:ANTO), which was up 1.5%.

6.43am: Hesitant start predicted

The FTSE 100 will start very hesitantly ahead of a potentially big Brexit day in parliament.

London's blue-chip index is predicted to drop three points to 7,163, according to spread betters, having added 13 the day before.

Boris Johnson is thought to have the House of Commons numbers to win a vote on his withdrawal agreement bill (https://www.gov.uk/government/publications/eu-withdrawal-agreement-bill - WAB), in what is known as the second reading of the bill on Tuesday, but may find it more difficult to get the deal through on the accelerated timeline for approval by 31 October.

This timeline, known as the programme motion, allows only three days’ of consideration and debate on the WAB, and many MPs who say they are willing to vote for the second or third readings are opposed to the current programme.

But even if the WAB continues its passage, various groups of MPs are planning to try to add amendments, including the push for a customs union and/or a confirmatory referendum.

"The prospect of an extension has continued to support the pound which made another five-month high against the US dollar yesterday above the 1.3000 level," said Michael Hewson at CMC Markets.

"For now, this appears to be acting as a short-term top, with markets reluctant to drive the currency too much higher given that there could be many more political twists and turns before any deal gets across the line."

Economists at Pantheon Macroeconomics noted that the pound has only been tickling the 1.3 mark rather than going much higher, saying “markets are right to view the passing of the WAB as far from a done deal”.

“By our reckoning, the customs union amendment will be only one vote short of passing if the SNP, Lib Dems and others back it, so the vote essentially looks likely to be a toss-up,” Pantheon said.

But the big votes are not scheduled until late on Tuesday evening, so investors can safely mull over some corporate news in the meantime, plus perhaps the second term for Canada’s Justin Trudeau confirmed overnight.

Hotel sector squeeze

Premier Inn owner Whitbread plc's (LON:WTB) half-year results come amid some negative news from the hotels sector.

At the end of last week, smaller rival easyHotel gave a grim assessment of UK market, saying its London hotels performed well enough but regional hotels saw a 2.8% decline, with many regions hit by double-digit drops.

Across the UK, sector-wide revenue per available room (revpar) is down by an average of 0.7% this year, according to market data from STR Global.

Recently, however, UBS upgraded the shares to 'buy' from 'neutral' as they said the recent share price valuation implies that the market is predicting Whitbread's revpar will fall 10%, while the analysts reckon the fall will be nearer 3%.

In the first quarter, Premier Inn reported a 6.0% fall in revpar, with total accommodation sales down 1.5% and like-for-like sales down 4.6%, blaming weaker business and consumer confidence due to Brexit uncertainty.

Tough for Travis

Similarly, after a profit warning by a sector peer last week, builders’ merchant Travis Perkins PLC (LON:TPK) will post what analysts say is “a relatively important update” on Tuesday.

Investors will be wondering how the economic backdrop has impacted the company’s third quarter, especially after Grafton’s warning last week that UK business has been hit by "increased economic uncertainty" that was preventing consumers from spending on home improvement projects.

With such strong pressure from macro conditions, Peel Hunt said this might mean the benefits from Travis Perkins’ operational improvements may be offset.

Also hotly anticipated will be news on sales at Wickes and the plumbing and heating division, which have been dividing consensus forecasts for adjusted results.

Anglo's diversity

Diversified miner Anglo American (LON:AAL) is to deliver third-quarter production reports on Tuesday.

Shares in many companies in the sector have stumbled in the last six months amid the ongoing trade war between the US and China, the world’s two biggest economies and major base metals importers.

Anglo American could be a winner since it should be better protected from copper and iron ore volatility as its 80%-owned platinum group metals division Amplats turned a corner and has risen strongly this year thanks to rising demand for palladium, used in batteries, and platinum, which has benefited from a bullish precious metals market.

RBC Capital Markets rates the diversified miner a “top pick” and raised its target price to 2,300p, meanwhile Credit Suisse has rated it an “outperform”.

Significant events on Tuesday 22 October:

Interims: Whitbread Group PLC (LON:WTB)

Trading statement: Anglo American plc (LON:AAL), Bunzl PLC (LON:BNZL), Gear4Music Holdings PLC (LON:G4M), Reckitt Benckiser Group PLC (LON:RB.), St James's Place PLC (LON:STJ), Travis Perkins PLC (LON:TPK)

AGMs: Accrol Group PLC (LON:ACRL), McBride (LON:MCB)

Economic announcements: UK public sector net borrowing, CBI industrial trends survey, US existing home sales, China policy decision

Business Headlines

Financial Times:

Downing Street believes Boris Johnson is on course to secure a narrow victory when MPs vote on his Withdrawal Agreement bill, although the backlash was furious over his attempt to railroad the whole legislation process through parliament with extremely limited scrutiny. Justin Trudeau’s Liberal party survived a multipronged challenge from both the left and right in Canada’s general election on Monday but he will return to power as the head of a minority government. Parties involved in opioid crisis litigation on Monday sketched out a $48bn proposal that could end thousands of lawsuits if four US states can convince their fellow plaintiffs to accept the deal from drugmakers and distributors. Botched public sector outsourcing contracts wasted at least £14.3 billion of taxpayers’ money in the past three years, according to the think-tank Reform. Coty is exploring the sale of its professional hair and nail products business, including Wella and Clairol, as it seeks to cut debt. Adam Neumann, the flamboyant co-founder of WeWork, is favouring a $9.5bn rescue proposal from his largest investor that would pay him about $200m to cede his outsize voting power and chairmanship of the crisis-hit property company.

The Times:

An influential think tank has questioned the value of a tax break for entrepreneurs, saying that it does little to promote business investment and only makes wealthy people even richer. More than £1 billion was wiped off Smith & Nephew’s market value yesterday after its chief executive stood down only 18 months into the role amid a dispute about his pay. Investors keen for swift and substantial capital growth might prefer to own Prudential shares, writes Tempus, those seeking a reliable income might be better off with M&G. The Financial Reporting Council has criticised the lack of diversity at accountancy firms, where women make up only 17% of partner-level roles. An Israeli drug company accused of helping to fuel America’s opioid addiction crisis has laid out a framework for a global settlement deal. Teva Pharmaceuticals said that it had offered $250 million in cash and a supply of Suboxone, an opioid addiction treatment, worth $23 billion to settle sprawling litigation against the company. The population of Britain is set to increase by three million over the next decade, with 80 per cent of the growth driven by immigration, according to official projections published yesterday.

The Daily Telegraph:

Boris Johnson is expected to abandon Brexit legislation in Parliament rather than accept a customs union or second referendum, rebel MPs were warned. Campaigners ask the Treasury to investigate the City watchdog's handling of the Woodford failure amid concerns the regulator is shirking its responsibilities. Endemol Shine is on the brink of a €2 billion takeover by television company Banijay. British esports firm Gfinity almost doubled its revenues on the back of a surge in the popularity of professional video game tournaments.

The Guardian:

Up to 12,000 Asda workers could lose their jobs next week, according to union officials, if they refuse to sign up to a new contract. Four major pharmaceutical companies agreed to a $260 million payout over the US opioid epidemic on Monday, hours before a landmark federal trial.

Daily Mail:

PWC could face legal action over claims it leaked highly sensitive information about the scandal-hit insurer Quindell in 2015. Sirius Minerals has insisted there are no plans to take the business private following controversial comments made by its boss.

A U.S.-China trade deal could be finalized by the New Year, according to Trump’s top advisor.

The outcome will hinge on mid-November negotiations in Chile, said Peter Navarro, director of trade and manufacturing for President Trump, at the Citizen by CNN Conference in New York City Thursday morning.

“The best thing to do is to just see what happens in Chile,” he said. “It will be a good indication to see where we are… As the president says many times, we’ll either get a great deal or we won’t, we’ll see what happens.”

The APEC Economic Leaders’ Meeting in Santiago, Chile on November 17, is part of a year-long Asia-Pacific Economic Cooperation forum facilitating cooperation among 21 Pacific Rim economies, including the U.S. and China. The meeting, facilitated by President of Chile Sebastian Pinera, will address “emerging trade challenges and the future of cooperation between APEC [Asia-Pacific Economic Cooperation] economies,” according to the event’s site.

FILE - In this file photo dated Wednesday, Sept. 11, 2019, U.S. White House trade adviser Peter Navarro speaks during a television interview at the White House, in Washington, U.S.A. The U.S. is threatening to pull the United States out of the 145-year-old Universal Postal Union, as Navarro said they opposes options being considered that would maintain the current limits. (AP Photo/Alex Brandon) More

With the presidential election approaching in 2020, China may want to wait for the outcome (and potentially a new U.S. president) instead of reaching a deal. “They [China] may play the string out, but that would be a miscalculation... They have underestimated the resolve of the president... [The Trump tariffs are] giving China the incentive to come to the bargaining table.” said Navarro. “Their [China’s] economy is hurting.”

When Jim Sciutto, chief national security correspondent for CNN, said the war is hurting the U.S. too, Navarro disagreed. “I don’t know that,” said Navarro, who emphasized that the costs of tariffs burdened by manufacturers and farmers have been offset by job growth and subsidies for farmers. A notion he has shared with Yahoo Finance.

Sarah Paynter is a reporter at Yahoo Finance. Follow her on Twitter @sarahapaynter

Read the latest financial and business news from Yahoo Finance

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.

More from Sarah:

Eric Trump on paying contractors: We pay ‘people when they do great jobs’

Bethenny Frankel on real estate: ‘Don’t worry about taking your losses on a sell’

Rich millennials are like their older cohorts: study

President Donald Trump reiterated that the United States will be withdrawing from the Paris Climate Agreement, praising soaring U.S. oil and gas production at the same time.

“I withdrew the United States from the terrible, one-sided Paris Climate Accord,” President Trump said at the 9th Annual Shale Insight Conference in Pittsburgh on Wednesday, less than two weeks before the United States can formally begin the process to pull out of the climate agreement on November 4.

This day is the earliest date on which the U.S. can submit a formal letter to the United Nations to begin the process of withdrawal, which would be completed one year after that, right around the time of the 2020 presidential election.

“The Paris Accord would’ve been shutting down American producers with excessive regulatory restrictions like you would not believe, while allowing foreign producers to pollute with impunity,” President Trump said at the Pittsburgh conference, touting America’s air and water as ones of the cleanest on earth.

“And, you know, as I said before, we’re now number one, not by a little bit, but by far. Way ahead of Saudi Arabia. Way ahead of Russia. But we can do even much better than that,” the U.S. President added, referring to U.S. oil production.

Petroleum and natural gas production in the United States jumped by 16 percent and 12 percent, respectively, in 2018, setting new production records and placing the United States as the world’s single largest producer of oil and natural gas, EIA has estimated. Related: Two Dead Following ISIS Attack On Iraqi Oil Field

Although the Trump Administration will soon formally begin the withdrawal from the global climate agreement, cities, states, and businesses continue to pledge emissions reduction through organizations such as America’s Pledge and We Are Still In. Across America, 24 states have committed to upholding the U.S. commitment to the Paris Accord of reducing emissions 26 to 28 percent below 2005 levels by 2025.

The Trump Administration’s intent to start the withdrawal process drew criticism from the Center for American Progress, whose president and CEO Neera Tanden said:

“Instead of projecting strength, this action weakens America on the world stage and cedes leadership on climate change and other challenges of our time to countries like Russia and China.”

By Tsvetana Paraskova for Oilprice.com

More Top Reads From Oilprice.com:

n initial pact on U.S-China trade will include much of a scrapped May deal’s agreement regarding intellectual property and will target enforcement mechanisms, White House trade adviser Peter Navarro said on Thursday, adding that he hopes the Chinese negotiate in “good faith.”

“The good news about this phase one ... is it adopted virtually the entire chapter in the deal last May that they reneged on for IP,” Navarro told Fox Business Network in an interview. “Practically it means, if they steal our IP we’ll be able to take retaliatory action without them retaliating.”

Teck Resources, Canada’s largest diversified miner, has kicked off a cost-cutting program that will see layoffs and the deferral of capital spending projects as the ongoing US-China trade hit the company’s third-quarter profit.

Revenue for the three months through September declined by 5.4% to C$3.04 billion, compared to a year ago, even as its energy and zinc units partly offset weak base metal and steelmaking coal prices caused by global economic uncertainty.

The Vancouver-based mining giant’s adjusted profit fell to C$403 million, or C$0.72 per share, in the quarter ended Sept. 30, from C$466 million, or C$0.81 per share, a year earlier. Analysts on average were expecting it to earn 66 Canadian cents per share, based on estimates by financial markets data firm Refinitiv.

“Over the past few years, we have focused our attention on maximizing production to capture margin during periods of higher commodity prices,” the company’s president and CEO, Don Lindsay, said. “However, current global economic uncertainties are having a significant negative effect on the prices for our products, particularly steelmaking coal.”

As part of the planned cost-cutting measures, Teck said it would eliminate around 500 full-time jobs. Some of them, it said, will come from attrition, the expiry of temporary or contract positions and current job vacancies.

Lindsay noted that while Teck would focus on improving efficiency and productivity across its business for the balance of 2019 and 2020, it will continue to forge ahead with certain key projects.

One of them, the company said, is Quebrada Blanca Phase 2 (QB2) project in Chile. Construction at one of the world’s largest undeveloped copper resources is expected to be completed in the fourth quarter of 2021, with ramp-up to full production expected during 2022.

Teck in late 2018 teamed up with the Japanese Sumitomo Metal Mining Co Ltd and Sumitomo Corp to boost the production of its aging open-pit mine in northern Chile to 300,000 tonnes of copper a year from 23,400 tonnes in 2017.

Copper, one of four business units at Teck besides steelmaking coal, oil and zinc, is considered a company’s priority.

https://www.mining.com/teck-to-lay-off-workers-cut-spending-as-us-china-trade-war-weighs-on-profit/

(Bloomberg Opinion) -- Saudi Arabia should give up trying to manage the global crude market and return to the pump-at-will policy it briefly adopted in 2014 under its longest serving oil minister Ali Al-Naimi.

In the mercantilist world in which we now live, where decisions are based on narrow national interest, it makes no sense for the world's lowest-cost oil producer to subsidize shale and prop up other high-cost suppliers.

Of course when it does, oil prices will crash just as they did in 1986 when the country finally abandoned fixed official selling prices. And then, in the aftermath, global investors will get in a flap about all things Saudi: the IPO of the kingdom’s state oil company, the financing required to fund a young and under-employed population, Mohammed bin Salman’s ambitious Vision 2030 plan to transform the economy away from its dependence on oil.

Despite the risks, it’s time to admit that market management is failing, even though Saudi Arabia and it “allies” say that it isn’t.

The OPEC+ agreement was meant to drain excess stockpiles in six months. But we are now approaching a fourth year of Saudi Arabia leading a global alliance of producers in trying — and failing — to push up oil prices in a sustainable way.

For a while it appeared that the cuts were having the desired effect. Inventories came down and Brent prices rose from about $45 a barrel in June 2017 to reach a high of $86 in October 2018. But they swiftly fell back towards $50 and a second round of cuts that began in January has failed to keep them above $60. Even the temporary loss of more than half of Saudi Arabia’s oil production — and most of the world’s spare capacity — in an attack on two of the kingdom’s biggest processing facilities failed to lift prices for more than a few days.

The latest data from OPEC itself — along with the International Energy Agency and the U.S. Energy Administration — show the failure of the policy.

All three see global oil inventories building in the first half of next year in the face of what is starting to look like America's forever trade war. The global gridlock has also prompted a reduction in forecasts for growth in oil demand this year and next. The average level of Saudi oil production in the first eight months of 2019 was the lowest since 2014 — even excluding the dip caused by the Sept. 14 attacks on the kingdom’s oil processing infrastructure. And it will have to come down further next year if the kingdom wants to continue trying to manage the market.

Meanwhile Russia, the kingdom’s leading partner in the OPEC+ group of countries that came together to manage supply, has seen its output continue to rise each year, even as it has come to dominate OPEC+ policymaking.

Saudi Arabia should let American shale drillers take the strain. After all, aren't they the producers of the marginal barrel of crude now? As long as Saudi Arabia and its cohorts continue to restrict output and subsidize shale they are merely delaying an answer to the question.

It’s time to discover a true price of oil.

Saudi Arabia will learn to work with this over time, just as it did after 1986. And it will probably find that that price isn’t as low as the kingdom fears. Eventually, shale producers will be forced to cut back — or they won’t.

If they are forced to cut, then Saudi Arabia will get the price support it craves, without having to lower its own output. But if shale production can just keep going up and up, even in a lower-price environment, then it proves just as emphatically that the Saudi-led policy of market management is a busted flush anyway.

Will they do it? I doubt it.

Current oil minister Abdulaziz Bin Salman sees it as his job “to ensure that the oversupply doesn’t continue.” December’s OPEC and OPEC+ meetings will likely yield the promise of further output cuts and Saudi Arabia will pump even less next year in a vain attempt to prop up prices. But it would be nice to believe that they are capable of change.

To contact the author of this story: Julian Lee at jlee1627@bloomberg.net

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Julian Lee is an oil strategist for Bloomberg. Previously he worked as a senior analyst at the Centre for Global Energy Studies.

For more articles like this, please visit us at bloomberg.com/opinion

©2019 Bloomberg L.P.

https://finance.yahoo.com/news/saudi-arabias-best-bet-crash-060024198.html

The U.S. pullout from Syria sparked strong—and opposing—reactions, as a move of that magnitude was bound to do. Trump bashers bashed Trump for quitting and Trump supporters cheered the America First agenda. And some pointed to the fact that this may be part of a larger reshuffling of priorities that could result in the United States effectively leaving the Middle East. Either way, the aftershock in the oil industry could be wide reaching.

It also could form strange alliances. In a recent story for Bloomberg, Liam Denning noted the unexpected unanimity between President Trump and one of the more popular Democratic contenders for the White House, Elizabeth Warren, on the troop pullout.

“The methods and language may be different,” Denning wrote. “But neither looks committed to the U.S. presence that has endured in the Middle East for decades.”

Indeed, it seems that Washington’s attention is shifting away from the Middle East and towards home. Even the troops Trump sent to Saudi Arabia after the attacks on its oil infrastructure were paid for by Riyadh, leading one analyst to call the move “Americans going pseudo-mercenary,” Denning writes.

That Trump and Warren agree on anything may be surprising at first, but a deeper look might suggest this agreement reflects the shifting priorities of their voters. The people who voted Trump into the White House wanted, among other things, of course, jobs, even in doomed industries such as coal. People who vote Democrat and may vote for Warren, care more about climate change than the never-ending conflicts in the Middle East. Related: Iraq's Return To Oil's Top Table

Besides, there is Trump’s weakness for tariff and sanction action. These have become his weapons of choice in international disputes, which are not as violent as troop deployment. The question of whether sanctions work is a different matter, but the fact remains that for all the alarm about Trump starting a war basically as soon as he enters office, he has mostly reserved his belligerence for Twitter.

So, what happens if the American troop exodus from the Middle East continues? The power balance there is already changing. Russia has expanded its influence in the region through its alliance with the Syrian government and its closeness with Iran.

China has been reluctant to stir this particular geopolitical pot directly, but it will sure step into premises vacated by the U.S. After all, China has the most to lose from an escalation of violence in its main supplier of crude oil. Related: There’s Tremendous Room For Growth In Offshore Oil & Gas

Speaking of oil supply, that’s a big part of the reason why Trump feels confident he can pull out U.S. troops from the Middle East. Whole still importing quite a lot of oil, the United States is nowhere as import-dependent as in the early 70s when the Arab oil embargo almost caused an economic collapse because of the spike in oil prices. It imports 6 million barrels daily, according to the EIA’s latest petroleum status report, and produces 12.6 million bpd.

True energy independence may be still out of reach, but the U.S. is no longer vitally dependent on Middle Eastern oil. It will certainly keep its allies—and arms buyers, of course—there close but thinking in Washington may be changing to reflect this reduced need for securing Middle Eastern oil flows with a presence on the ground.

By Irina Slav for Oilprice.com

More Top Reads From Oilprice.com:

Brazilian state-run oil firm Petroleo Brasileiro SA posted a significant production boost in the third quarter, as heavy investments in its deepwater, pre-salt zone showed signs of paying off.

Investors and analysts have been watching the firm’s production figures closely in recent quarters, and the company’s ability to swiftly boost output is key to its current strategy.

In a securities filing, Petrobras, as the firm is commonly known, said it produced 2.878 million barrels of oil equivalent per day (boepd) in the third quarter, up 9.3% from the previous quarter and 14.6% from the same period a year ago.

August monthly production reached a new record of 3 million boepd, and daily production hit a high of 3.1 million boepd during the month. The company is on target to reach its annual production target of 2.7 million boepd, Petrobras added in the filing.

First quarter production at Petrobras was considered weak, and while second-quarter figures were markedly better, some analysts were spoked by poor June figures, which were affected by a number of stoppages. In late July, Chief Executive Roberto Castello Branco revised the firm’s 2019 annual target to 2.7 million boepd from a previous 2.8 million, which hit Petrobras shares.

Third quarter production in Petrobras’ core pre-salt region climbed 17% from the previous quarter. Post-salt production, which also takes place in deep waters, as well as onshore production remained roughly steady on a quarterly basis.

Shallow-water production increased 9.8% from the second quarter, Petrobras said, as platform stoppages were reversed.

The company said its new P-68 production platform left the shipyard in September and is currently in the anchoring process. It will begin producing in Petrobras’ Berbigao and Sururu oilfields in the fourth quarter.

Carlyle Group (CG.O) said on Friday it had dropped out as a stakeholder in Lone Star Ports LLC, which proposed a $1 billion crude oil export terminal near Corpus Christi, Texas.

Sean Strawbridge, chief executive of the Port of Corpus Christi, said Carlyle notified the port on Oct. 8 it would no longer proceed with its investment. That left construction company Berry Group as the sole backer.

Carlyle said in a statement Berry Group was “now the sole owner of Lone Star,” but did not comment on why it dropped out of the project, which it said continues to be actively developed.

Lone Star in September filed a lawsuit against Carlyle in a Texas state court, alleging the private equity firm breached its contract to jointly pursue the project and asking the court to award it full ownership. The lawsuit also sought unspecified damages.

The project was one of at least nine crude oil export terminals proposed for the U.S. Gulf Coast to load U.S. shale oil onto supertankers that carry around 2 million barrels apiece. Carlyle was competing with projects in the same area proposed by commodities trader Trafigura AG and refiner Phillips 66 (PSX.N).

“Interest in Harbor Island remains at an all-time high,” Strawbridge said. The port will continue dredging in the area to make it more attractive to export crude, he said.

Lone Star and Berry did not immediately respond to requests for comment.

The U.S. shale boom has prompted a surge in oil exports, which last week hit 3.25 million barrels per day (bpd) and continued to fuel a race to build new export terminals.

However, only one or two of the proposed projects may get built in coming years, with offshore terminals proposed by pipeline operator Enterprise Products Partners LP (EPD.N) and Phillips 66 having the best chance of moving forward, said Sandy Fielden, an energy analyst at financial services company Morningstar.

Investors also have grown wary of global oil demand and have questioned “if the world is ready to absorb that amount of additional exports,” Fielden said.

Carlyle’s project had faced hurdles including a months-long delay after regulators called for a full environmental review. It also faced fierce competition with Trafigura, which launched its project earlier, with an easier path to regulatory approval and fewer objections from environmentalists.

Carlyle earlier this year had been looking to sell a 25% stake in the project with companies that operate U.S. pipelines and storage terminals for $625 million, a source familiar with the matter had said.

Enterprise signed long-term agreements with oil major Chevron Corp (CVX.N) that advanced its proposed offshore crude export project near Houston, it said in late July, making it the first to make a final investment decision on a proposed deepwater port.

Singapore — The combined run rates at China's independent refineries in eastern Shandong province hit a 19-month high of 68.3% in September, compared with 60.4% in August, according to S&P Global Platts calculations based on raw data from JLC.

JLC is a Beijing-based information provider, formerly known as JYD.

On a year-on-year basis, it was higher than the 67.8% from a year earlier.

The higher run rates in September were mainly attributed to the restart of several refineries despite weaker refining margins during the month. Jincheng Petrochemical lifted crude throughputs in September, and Haihua Petrochemical restarted operations after an upgrade.

Refining margins for processing imported crudes -- a basket of common grades including Lula, ESPO and Oman -- dropped by about Yuan 90/mt ($12.3/mt) to around Yuan 177/mt, theoretically, from August, according to JLC.

Looking into October, with refining margins remaining strong from the end of September, the run rates are likely to stay flat or slightly lower this month.

On the other hand, with spot premiums for various import crude grades rising sharply in October, some refineries were hesitant to purchase crudes at such high prices for November or December deliveries. This will probably cap the run rates in the coming months, according to refinery sources.

JLC's survey covered 44 independent refineries, with a total capacity of 172.4 million mt/year (3.4 million b/d), which accounts for about 60% of the country's total independent capacity.

FEEDSTOCK CONSUMPTION

Total feedstock consumption at the 44 surveyed refineries recovered by 13.2% on the month from August to around 2.4 million b/d last month, Platts calculations showed.

Dongming Petrochemical, Hongrun Petrochemical, Jincheng Petrochemical, Changyi Petrochemical and Luqing Petrochemical were the top five refineries that cracked the most crudes last month, with an average consumption of 529,600 mt.

This was 16.5% higher from an average of 454,000 mt cracked by the top five refineries in August.

Among those refineries, total crudes processed by Jincheng Petrochemical have seen the biggest increase, of 177.8% from a month earlier to 500,000 mt. The refinery resumed full operations in September after suspending for about a month from heavy flooding caused by Typhoon Lekima.

The crude throughputs from Dongming also increased, by 82.9% on the month to around 640,000 mt, making it the top refiner in terms of feedstock consumption last month.

Total consumption by the remaining 32 operational refineries -- excluding seven that were under maintenance or have been offline for months -- processed about 220,000 mt on average.

FAR EAST RUSSIAN ESPO CRUDE

The consumption of ESPO crude fell by 0.9% on the month to around 1.62 million mt in September.

Around 16 refineries cracked the grade. Lijin Petrochemical was still the top cracker for ESPO crudes at 280,000 mt, while Changyi Petrochemical followed at 230,000 mt in September.

Meanwhile, the consumption of Lula increased by 31.5% on the month to around 1.17 million mt.

In September, Lula was cracked by 17 refineries, compared to 14 refineries in August.

Besides these two grades, Oman and Nemina were the other two grades that were widely processed. The consumption of Oman crudes increased by 10.6% to 730,000 mt, and it was 82.5% higher year on year.

In September, a total 34 grades of imported crudes were cracked by the surveyed refineries compared with 38 grades in August.

GASOIL OUTPUT

The output of gasoil reached a record high of 4.54 million mt in September, up 10.3% on the month.

Meanwhile, gasoline output rose by 1.6% on the month to around 2.81 million mt, slightly lower than the record high of 2.82 million mt in July.

This has led to a record high for the combined output of gasoil and gasoline, at 7.34 million mt.

Separately, the gasoil/gasoline ratio reached a 10-month high of 1.62:1.

The relatively strong demand from agricultural harvest in northern China and the driving season during the National Day holiday in early October encouraged refineries to lift the gasoil and gasoline outputs last month.

In September, the average price of gasoil increased by Yuan 129/mt, or 1.83% on the month, to around Yuan 6,620/mt, while the price of 92 RON gasoline increased by 5.4%, or Yuan 359/mt, to around Yuan 6,964/mt.

-- Analyst Daisy Xu, daisy.xu@spglobal.com

-- Edited by Shashwat Pradhan, shashwat.pradhan@spglobal.com

Dhahran — Saudi Aramco, which temporarily lost half of its oil production following the September 14 attacks on two key oil facilities, is running its local refineries at full capacity and is forging ahead with plans to start up new refineries, the company's senior vice president for downstream Abdulaziz al-Judaimi said on Monday.

"Domestic refineries are operating at full capacity," Judaimi told reporters at the company's headquarters in Dhahran.

"We met every customer requirement [after the attacks]," he said, adding that Aramco did not buy crude to meet demand.

The attack on Abqaiq, the world's biggest oil processing capacity and Khurais, the country's second largest oil field, cut the company's output by some 5.7 million b/d.

Saudi Arabia's wellhead crude production stands at 9.9 million b/d, with production capacity of 11.3 million b/d, the country's oil minister Abdulaziz bin Salman said earlier this month.

The country intends to return to full oil production capacity of 12 million b/d by the end of November.

Aramco has five domestic refineries with total processing capacity of 1.9 million b/d.

New refineries

Aramco is on track to start up by the end of this year a new 400,000 b/d domestic refinery and petrochemical project in Jazan, Judaimi said.

The company is also starting up a joint venture refinery in Malaysia next year, he added. According to Aramco's bond prospectus released in April, the refining and petrochemical joint venture with Petronas -- the Malaysian national oil company -- collectively known as PRefChem, was supposed to start this year.

The PRefChem joint venture includes a 300,000 b/d refinery, an integrated steam cracker with capacity to produce 1.3 million mt of ethylene located in Johor, Malaysia. Aramco was supposed to provide a significant portion of PRefChem's crude supply under a long-term supply agreement. Jazan and PrefChem will help Aramco reach a gross refining capacity of 5.6 million b/d, it said in the prospectus.

The company currently owns and has stakes in four refineries abroad with a total refining capacity exceeding 2 million b/d.

Aramco also expects to close by 2021 a deal to buy a 20% stake in the oil-to-chemicals business of India's Reliance Industries, a deal that will add another 1.4 million b/d of refining capacity to the Saudi company's portfolio, Judaimi said.

Acquisitions

Aramco's long term goal is to have up to 10 million b/d of refining capacity, he added.

Aramco has been scouring the globe for opportunities to set up refining and petrochemical projects.

In April, Saudi Aramco acquired a 17% stake in South Korea's Hyundai Oilbank from Hyundai Heavy Industries. Oilbank has a processing capacity of 650,000 b/d.

This deal makes Saudi Aramco the second-largest shareholder of Hyundai Oilbank, following Hyundai Heavy Industries Holdings with a 74.1% stake in Hyundai Oilbank.

In September, Aramco signed a memorandum of understanding that facilitates its planned acquisition of a 9% stake in the Zhejiang integrated refinery and petrochemical complex in China.

In February, Aramco signed an agreement to form a joint venture with NORINCO Group and Panjin Sincen to develop an integrated refining and petrochemical complex located in China as well.

SABIC deal

Aramco is also in the process of finalizing the acquisition of a 70% stake in SABIC, the Middle East's biggest petrochemical company, as the state-run firm forges ahead with beefing up its petrochemicals portfolio, Judaimi said.

"We are near the finish line on the SABIC acquisition," he said.

Aramco officials had said the company partly delayed its initial public offering of up to a 5% stake last year due to its acquisition of SABIC for $69 billion.

-- Claudia Carpenter, claudia.carpenter@spglobal.com

-- Dania Saadi, dania.el.saadi@spglobal.com

-- Edited by Kshitiz Goliya, kshitiz.goliya@spglobal.com

Equinor’s first cargo from Johan Sverdrup set for Asia trip

10/21/2019

OSLO - Oil from the giant Johan Sverdrup field in the North Sea has arrived at the Mongstad plant north of Bergen. “This is a great day for Equinor and the Johan Sverdrup partnership, consisting of Lundin Norway, Petoro, Aker BP and Total. First oil to Mongstad only a few days after production start confirms that the field is producing well. This day also marks the start of a new phase as we prepare to bring Johan Sverdrup oil to the international market,” says Irene Rummelhoff, executive vice president for Marketing, Midstream & Processing (MMP) in Equinor.

Oil is piped from the North Sea Johan Sverdrup field, a distance of 283 kilometers. At the Mongstad complex the oil is stored in caverns and prepared for shipping to markets all over the world.

The first cargo is expected to leave for customers in Asia this week, and contains 1 MMbbl of crude with a market value of around $60 million. Future cargoes are expected to contain between 600,000 and 2 MMbbl.

“Oil from Johan Sverdrup is expected to provide revenue of more than NOK 1400 billion for the next 50 years, of which more than NOK 900 billion will go to the Norwegian state and society. Mongstad will play an important role in realizing this value. At the same time, Johan Sverdrup triggers high activity at the plant and new opportunities for the future,” says Rummelhoff.

As Johan Sverdrup receives power from shore, oil will be produced with record-low climate gas emissions of less than one kilogram of CO 2 /bbl.

The Mongstad plant is expected to receive up to 440,000 boepd from Johan Sverdrup when the first development phase reaches peak production. When the second phase is completed in 2022, Mongstad will receive up to 660,000 boepd.

When Johan Sverdrup is operating at full capacity, Mongstad will receive more than 30% of the total oil from the Norwegian continental shelf. Johan Sverdrup will lead to higher activity and new opportunities for Mongstad, which is an important plant for the company, and will help strengthen the importance of Equinor’s onshore activities in Norway.

Many people at Mongstad have been involved in preparing the reception of oil from Johan Sverdrup, including Equinor employees and many suppliers.

“This is a big day for everyone who has worked for a long time on preparing Mongstad for oil from Johan Sverdrup. It has been a major effort involving plant modifications and completion of pipes. The work has been carried out properly and efficiently. As head of Mongstad I am proud of the great effort leading up to this day,” says Rasmus F. Wille, vice president for the Mongstad complex.

Related News ///

FROM THE ARCHIVE ///

Oil extends decline as concerns over global economy persist

(FILES) In this file photo taken on September 6, 2016 shows pump jacks and a gas flare near Williston, North Dakota. - (FILES) In this file photo taken on September 6, 2016 shows pump jacks and a gas flare near Williston, North Dakota. - Photo: ROBYN BECK, Contributor / AFP/Getty Images Photo: ROBYN BECK, Contributor / AFP/Getty Images Image 1 of / 1 Caption Close Oil extends decline as concerns over global economy persist 1 / 1 Back to Gallery

Oil fell again after a weekly loss amid ongoing concern that a fragile economic outlook will continue to weigh on fuel demand.

Futures fell 1% in New York after dropping 1.7% last week. Policy makers in China, the world’s second-biggest oil consumer, are preparing for two key meetings with fresh evidence that economic growth will slip further from its lowest in almost three decades. Speculators have almost tripled short positions in U.S. crude futures since mid-September as Washington and Beijing struggle to finalize a trade deal, according to data released on Friday.

Oil has declined 19% since an April peak even though markets were last month hit by the biggest-ever supply incident with the missile strike on Saudi Arabia’s Abqaiq plant, and continue to face crises from Iran to Venezuela and Iraq. Any fears over supply are being drowned out by the increasingly bleak economic outlook.

PREVIOUSLY: Oil posts a weekly loss amid dour economic outlook, supply rise

“The alarm bells for the global economy are ringing to the rhythm of doom,” said Stephen Brennock, an analyst at PVM Oil Associates Ltd. in London.

WTI for November delivery fell 51 cents to $53.27 a barrel on the New York Mercantile Exchange as of 10:24 a.m. in London. The contract lost 15 cents to close at $53.78 on Friday, capping a 1.7% weekly loss.

Brent for December settlement fell 67 cents to $58.75 a barrel on the London-based ICE Futures Europe Exchange. The contract fell 49 cents to $59.42 on Friday. The global benchmark crude traded at a $5.34 premium to WTI for the same month.

NEWSLETTER: Get Fuel Fix headlines in your inbox each weekday

Short-selling of WTI has climbed to 114,709 futures and options, from just 39,948 in the week ended Sept. 17, according to U.S. Commodity Futures Trading Commission data. Net-long positions, or the difference between the long and short positions, shrank 8.8%.

“The market longs for better macro data and a further weakening of the U.S. dollar before it will turn positive on the outlook for the oil market,” said Jens Naervig Pedersen, a senior analyst at Danske Bank A/S in Copenhagen.

--With assistance from James Thornhill.

©2019 Bloomberg L.P.

LONDON (ICIS)--SABIC’s joint ventures and acquisitions around the world are set to continue as it seeks to widen its reach, according to the vice president (VP) for petrochemicals at the Saudi chemicals major.

Abdulrahman Al-Fageeh added that sustainability would be at the core of the company’s business going forward, although he would not disclose how much money SABIC allocates for research and development (R&D) going into circularity.

The executive said he could not give details about the proposed acquisition by Saudi energy major Aramco, which plans to become the majority owner of SABIC by acquiring a 70% stake for $69bn.

SUSTAINABLITY: CUSTOMERS DEMAND

The executive spoke to ICIS on the sidelines of the plastics and rubber trade fair K, in Dusseldorf, Germany, where many petrochemicals companies have announced projects to produce greener chemicals.

A sea change from the last K Trade Fair in 2016.

However, higher costs to produce greener products from sustainable feedstocks has so far been a key impediment for intake among end customers.

According to Al-Fageeh, that is not the main reasoning anymore, and it is end consumers the ones demanding more sustainable products as public awareness rises.

On 17 October, SABIC said it was targeting an industry first by launching a polycarbonate (PC) based on certified, renewable feedstocks.

“This is just the start. This has value for us and we want to pursue [this line of work]. As well as achieving a more circular economy, this benefits the environmental and the economy,” said Al-Fageeh.

“We need do make sure we have a very sustainable business for the company – our customers and business partners are requesting this, as well as [end market, consumers products] brand owners.”

The executive said, however, that it would be difficult to quantify how much SABIC assigns to R&D because the issue is looked at as “part of our renovation” and spills over to every project the company starts up.

“Given the way we operate, it would be unfair to give you some numbers. R&D is part of our renovation and we call it an investment to make sure we have operations based on safe assets,” said Al-Fageeh.

“Frankly speaking, R&D is not only the money we spend on R&D [activities] but more in a cross-wise way – in the development of our people or in our assets investments themselves.

“We are spending huge resources [on R&D],” he added.

SABIC’s annual report for 2018 does not specify either spending on R&D. Its Sustainability Report 2018 is also scarce in figures.

However, for a company like SABIC, headquartered in a country sitting above vast amounts of crude oil, hardly circular products based on fossil fuels are destined to continue being its main offering.

SABIC’s ways of producing really matter. The company has become a key, major petrochemicals, with operations spanning globally.

Al-Fageeh diagnosis on crude oil may indicate that there is still a long way to achieve a non-fossil fuels petrochemicals industry.

“Crude oil will continue to be our focus for cracking and for production of petrochemicals,” he said.

UPCOMING PROJECTS

Those operations spanning the globe include projects from China to the US, from Europe to the Middle East.

However, Al-Fageeh did not give any update about the projects, which among others include a 50:50 joint venture in the US with energy and petrochemicals major ExxonMobil due to start up in 2022.

The petrochemicals complex would include a 1.8m tonne/year ethane cracker, two polyethylene (PE) units, and a monoethylene glycol (MEG) plant.

In China, the company is mulling a “world-scale” petrochemicals complex in the Chinese province of Fujian, south of Shanghai, although no definitive timelines have been set out.

ARAMCO, CLARIANT

While Al-Fageeh said he was “wrong guy” to ask about Aramco’s acquisition at SABIC, he also said he could not comment on SABIC’s 24.99% stake at Swiss chemicals producer Clariant, and whether the company intends to keep that stake.

SABIC's participation in Clariant's capital structure came to be more turbulent than expected.

After the Saudi major came to the rescue of Clariant's management, under siege by activist investors who kept increasing their stake at the company to force a change of course, the SABIC-appointed CEO Ernesto Ochiello resigned only a few months later.

He is now an executive at SABIC again.

The former CEO Hariolf Kottmann returned to Clariant’s help in an interim basis.

At the time of Ochiello’s resignation, both companies also cancelled one of the tie-up's stars: a joint venture for production of high performance materials.

Al Fageeh only said that despite the joint venture’s sudden end, “high performance polymers is still one of the core businesses” at SABIC, adding that growth will continue to come from acquisitions when the right opportunities arise.

"As usual, SABIC is open to any opportunity. Growth cannot only be organic: it needs to be both [organic and acquisitions]."

'AWAY FROM POLITICS'

There are growing signs that the US-China trade war is reducing business for US polyolefins producers in Asia, who were hoping the increasing capacities in their home market could be exported, mostly to China.

The reduction in business would give other low-cost producers, like those in the Middle East, a chance to maintain or increase market share in China.

But Al-Fageeh would not give concrete figures to back that up, and limited himself to call for freer trade and for tariff and non-tariff trade barriers to diminish.

“We don’t like difficulties. We are encouraging decision makers to make sure there are no barriers [to trade],” he said.