2019-05-13 13:43 First FinanceI want to comment 0

Font size:

From January to March this year, among the 20 cities with the national air quality status notified by the Ministry of Ecology and Environment, Xianyang, Weinan and Xi'an were among them. In the 20 cities ranked after the relatively poor air quality in 2018, Xianyang and Weinan are also on the list.

The Central Second Ecological Environmental Protection Inspector Group today (13th) pointed out to Shaanxi Province's “review” and special inspections that the special inspectors found that Shaanxi Province has done a lot of work in the field of air pollution prevention and control, and the quality of the atmospheric environment has been improved. Improvement, but the problem of structural pollution is still outstanding, and the situation is still grim.

In the new round of national air pollution prevention and control action plan, the Yan Plain was identified as a key area alongside the Beijing-Tianjin-Hebei region and the surrounding areas and the Yangtze River Delta region, involving Luliang, Jinzhong, Linyi and Yuncheng in Shanxi Province and Luoyang in Henan Province. There are 11 cities including Sanmenxia City, Xi'an, Xianyang, Baoji, Tongchuan, Weinan and Yangling Demonstration Zones in Shaanxi Province.

The Shaanxi Provincial Government issued the "Three-Year Action Plan for the Battle of the Iron and Steel in Shaanxi Province to Win the Blue Sky Defence War (2018-2020)", saying that the proportion of Shaanxi's secondary industry in the total economic output is 49.8%, which is higher than the national average of 9.3. percentage point. Coal accounts for 8.2 percentage points of primary energy. The emission intensity of sulfur dioxide and nitrogen oxides in Guanzhong area is 3.9 times and 3.6 times of the national average.

The overall industrial structure and energy structure are not good, resulting in obvious characteristics of composite air pollution. PM10, PM2.5 and ozone have become the main factors affecting the air quality in Shaanxi Province. In 2017, Shaanxi's coal accounted for about 75% of the primary energy consumption structure, and did not meet the target of reducing to below 67%.

In addition, is Shaanxi Province really active and effective in the prevention and control of air pollution? At the feedback meeting held today, Zhu Zhixin, the head of the inspection team, said that Shaanxi Province’s “reduction of coal is not strict, clean coal is not well protected, and some industries are seriously polluted.” “Don’t dare to touch hard in rectification” Rectification and surface rectification are more common."

The inspector group pointed out these problems in Shaanxi Province:

In the rectification, I dare not touch the hard, and I dare not manage and do not want to control large enterprises. The first round of inspectors transferred the pollution problem of Shaanxi Huangling Coal Chemical Company five times, but it was not rectified. In the law enforcement inspection of the National People's Congress in 2018, it was discovered that Yanchang Xinghua Chemical Company sneaked exhaust gas and Jinduicheng Molybdenum Co., Ltd. had long-term excessive discharge of sulfur dioxide. The “Looking Back” also found that Hancheng Longmen Coal Chemical Company and other four companies Similar to corporate environmental violations.

The problem of coal reduction in Shaanxi Province has not been effectively rectified. The coal reduction work of the Provincial Development and Reform Commission mainly relies on aggregated data. In particular, the requirements for coal reduction by power companies are soft and soft, and the work of “fixing electricity by heat” and optimizing power dispatching during heating season is not effective. In 2017, the coal reduction mission of enterprises above designated size only achieved 66.78% of the target.

Xi'an City will sign the "coal to electricity, coal to gas" transformation agreement as a task to complete the transformation, reported to reduce the distortion of loose coal data. Xixian New District, Liquan County, Xianyang City, Weinan City, Han City and other places falsely reported, falsely reported that "coal to electricity, coal to gas" to complete the task, part of the loose coal reduction "nothing."

Shaanxi Meixin Industrial Investment Co., Ltd. did not strictly implement the capacity substitution requirements in accordance with the rectification plan, and increased the production capacity without authorization. The annual production capacity of 300,000 tons of electrolytic aluminum without the formalities of compliance was expanded to 450,000 tons. Weinan City and Heyang County condone the construction of the Virgin Lake in violation of laws and regulations, destroying nearly 3,000 mu of wetlands. After the State “Green Shield Action” pointed out the problem, the local area used “natural recovery” as an excuse, and the related restoration and repair work was stagnant.

In addition, the inspector found that Xianyang City recognized that the amount of coal used by Datang Binchang Power Plant in 2017 increased by 410,000 tons compared with the previous year, but the actual increase was 600,000 tons. Weinan City confirmed that Shaanxi Jiaojia Chemical Company reduced coal by 19,000 tons in 2017, but the actual increase was 300,000 tons.

The Tongchuan Municipal Development and Reform Commission approved four companies, including Shengwei Building Materials and Shengwei Special Cement, to cut 170,000 tons of coal in 2017, but it did not actually increase 180,000 tons. From January to September 2018, Xianyang Chemical Industry Co., Ltd. did not reduce coal consumption, and asked the government to coordinate coal reduction targets in the name of heating and protecting people's livelihood, resulting in adverse social impacts.

Zhu Zhixin said that there are more than 130 small thermal power units of less than 100,000 kilowatts in Shaanxi Province, which have high coal consumption and high pollution. However, the attitude of shutting down small thermal power units is not determined, and the promotion is weak. From 2015 to 2017, only 7 small units will be phased out. The unit, most of the high coal consumption units are reserved in the name of heat supply or comprehensive utilization, and the existing small units for heating generally fail to implement “heat setting” according to requirements.

The inspector found that the small boiler demolition work in the Guanzhong area of Shaanxi was slow to advance. At present, there are still 607 coal-fired boilers of 10 steam/ton or less that have not been removed, and 26 coal-fired boilers of 20 steam/ton or more have not yet completed ultra-low emission conversion. 414 sets of production and operation type gas boilers have not completed low-nitrogen combustion reform. Yulin City violated the air pollution prevention and control action plan. Since 2014, it has built 121 coal-fired boilers with a capacity of less than 10 tons.

The inspector also found that the pollution control and supervision of the coking enterprises in the Han city were not in place, and the corporate environment was illegal. Longmen Coal Chemical Company has long used the bypass flue to discharge coke oven flue gas; Heli Coal Coke Company falsified during the inspection, and lied to complete the work of CDQ reform; Shaanxi Zhonghui Coal Chemical Company VOCs governance actually changed from dispersed emissions to Concentrated emissions. The supervision of the environmental protection departments of Weinan City was weak, and the process waste gas treatment facilities of the Suihua Group were not operating normally for a long time. Shaanxi Province pays insufficient attention to the pollution control of the ceramic industry in Guanzhong area, and the requirements are not strict. The existing ceramic enterprises have low pollution control level and unorganized emissions.

In addition, the distribution of clean coal distribution centers in Baoji and Xianyang is relatively low, which is quite different from the demand; the Qinhan New Town Clean Coal Distribution Center in Xixian New District stores more than 4,000 tons of industrial coal, and there is direct sales behavior. The quality of clean coal is difficult to guarantee. The coal quality supervision work in some areas was not in place. The Hancheng Municipal Market Supervision Bureau did not conduct coal quality monitoring for large coal users and key coal units during the heating season. The Yulin City Quality Supervision Bureau never arranged for the deployment of loose coal quality inspection.

At the feedback meeting, Zhu Zhixin said that Shaanxi Province should focus on promoting the prevention and control of air pollution in the plain, and focus on accelerating the adjustment of industrial energy structure, making overall plans and comprehensive measures to promote the province to win the blue sky defense and achieve high quality development. . According to the law, serious responsibility is pursued, and the problem of dereliction of duty is instructed to further investigate the situation, clarify responsibilities, and be responsible for seriousness, accuracy and effectiveness in accordance with relevant regulations.

Editor in charge: Li Guolei

After having grown by 2.5% in 2018, global copper production is expected to remain essentially unchanged this year, but will grow by 1.9% in 2020, the International Copper Study Group (ICSG) said in its ‘Copper Market Forecast for 2019/20’, released on Monday.

ICSG met with global copper industry stakeholders on May 9 and 10 to discuss key issues affecting the global copper market.

Global mine production increased by 2.5% in 2018, mainly owing to constrained output in 2017 and to an unusually low rate of overall supply disruptions in 2018.

Besides the restart of the Katanga mine in the Democratic Republic of Congo (DRC), no major new copper mine capacity was brought on stream in 2018.

This year, additional output from the start-up of the major Cobre de Panama mine, in Panama, the expansion of Toquepala mine, in Peru, and the commissioning of a few other small to medium mines is expected to be balanced by a significant decline in Indonesian output – owing to the transition of Grasberg to an underground operation and Batu Hijau mine to Phase 7 – and regulatory and taxation issues, which will negatively impact output in Zambia.

For 2020, the ICSG said, additional supply from mines in ramp-up and expansions that started in 2019, together with a recovery in Indonesian output, will support growth of about 1.9%.

REFINED PRODUCTION

Refined production, meanwhile, is expected to increase by around 2.8% this year and by 1.2% in 2020.

In 2018, global refined copper production was constrained by an unusually high frequency of smelter disruptions and temporary shutdowns for technical upgrades and modernisations.

This year, expanded electrolytic capacity in China, the ramp-up of electrowinning output in the DRC and the recovery from 2018 operational issues and maintenance at smelters in Australia, Brazil, Indonesia and Poland, besides others, will largely offset lower anticipated production at some plants in China and Europe, owing to planned maintenance shutdowns, and lower output in Chile and Zambia, owing to operational issues at smelters.

A rise of 2.8% is expected for this year but, in 2020, planned electrolytic refined production is likely to be constrained by tightness in the availability of concentrates, resulting in a limited increase of 1.2% in world refined production.

After a small decline in 2018, world secondary production from scrap is expected to recover in 2019 and 2020. China will remain the biggest contributor to world refined production growth in both 2019 and 2020.

APPARENT REFINED USE

The ICSG expects world apparent refined copper use to increase by around 2% this year and by 1.5% in 2020.

The organisation stated that sustained growth in copper demand should continue because copper is essential to economic activity and even more so to modern technological society.

Infrastructure development in major countries such as China and India and the global trend towards cleaner energy will also continue to support copper demand.

China will remain the biggest contributor to global growth in copper use. Although underlying “real” demand growth in China is estimated by some analysts to be around 2.6% this year, Chinese apparent demand is predicted to rise by 2%.

The outlook for the European Union and Japan remains sluggish for 2019 and 2020, with demand in the US continuing to rise this year, but levelling off in 2020.

Global use, excluding China, is expected grow by around 1.7% this year and by a further 2% in 2020, mainly supported by increases in the Middle East, India and some other Asian countries.

World refined copper balance projections indicate a deficit of about 190 000 t and 250 000 t for 2019 and 2020 respectively.

Ball bearing searches tick down.

Surge in 'tax air freight tracking' searches from the US. (There's a 14 day window before all the tariffs hit on Chinese exports )

Air freight searches ticking down, but that trend existed prior to the tariff announcement.

Yuan weakening steadily now.

Bitcoin breakout.

Everything about the oversize outsider who surfaced near Norway’s Russian border seemed to confirm he was a Kremlin spy. His demeanor was excessively friendly. The gear he was sporting when detained said, “Equipment—St. Petersburg.” Adding to suspicions, the Kremlin stayed mum.

Norwegian scientists were convinced: The beluga whale stalking boats off the Arctic coast was an operative from the Russian base in Murmansk that trains sea mammals for military missions.

“If this comes from Russia—and there is great reason to believe it—then it is not Russian scientists, but rather the navy that has done this,” Martin Biuw from the Institute of Marine Research in Norway told the country’s national broadcaster.

The harness that the whale was wearing, scientists speculated, could carry a camera or a weapon. The white, SUV-sized mammal was named “Hvaldimir” in an online poll, combining the Norwegian word for whale and the first name of Russia’s president.

Scientists believe that the harness the whale was wearing could carry a camera or a weapon. Photo: jorgen ree wiig/norwegian direct/Shutterstock

Morten Vikeby, a former Norwegian consul in Murmansk, offered a different theory to fishing publication Fiskeribladet: The whale could have escaped from a therapeutic center for underprivileged children who used to pet it and watch it perform tricks.

Wherever the truth lies, behind the spy-whale fever that has gripped Norway is the question of whether Russia is the West’s most cunning adversary or just the one that is best at pushing its buttons.

Share Your Thoughts Should the U.S. and Russia be using sea mammals for military purposes? Why or why not?

With an economy the size of Spain’s and a stretched military, Russia has relied on cheap but high-profile operations that can yield outsize results. They often involve deception aimed at projecting power far greater than the Kremlin actually wields.

The Russian military, when announcing exercises, sometimes adds field kitchens to tallies of vehicles to boost numbers. The army hired far more railcars than it needed for war games in 2017 that made some in the Baltic countries nervous that an invasion was imminent. Russia uses inflatable tank replicas to feign larger formations.

Western analysis—and in some cases, imagination—has at times helped to inflate Russia’s reputation. The Cold War and its aftermath brought decades of trying to divine the workings of the Kremlin and assess the power and strategies of President Vladimir Putin, a former KGB colonel.

A military vehicle is loaded onto an amphibious warfare ship during an exercise in the Murmansk region. The Russian military, when announcing exercises, sometimes adds field kitchens to tallies of vehicles to boost numbers. Photo: Lev Fedoseyev/TASS/ZUMA Press

For the Kremlin, “it’s very important to create an exaggerated sense of Russia’s capacities and the risk of conflict,” said Mark Galeotti, senior associate fellow at the Royal United Services Institute in London.

“If you are already pegged as the schoolyard bully, you want to be the most formidable bully around so no one is going to challenge you, and everyone meekly hands over their lunch money,” he said.

Russia could have sought to soften its image by dismissing the whale story, said Keir Giles, senior consulting fellow of the Russia and Eurasia Program at London-based think tank Chatham House. “By ignoring it, Russia shows it is content to be seen as a state that will take any measures to covertly attack other states, including harnessing innocent sea mammals,” he said.

Russia doesn’t judge an operation’s success by its elegance or stealth, said Mr. Giles. A mission near London in 2018 that U.K. officials said was carried out by Russian military-intelligence officers to murder a former colleague, Sergei Skripal, ostensibly failed. Mr. Skripal survived and the alleged culprits were caught on security cameras and identified.

Instead of hushing-up the incident, Russia flaunted its derring-do by putting the men on state TV. As if to thumb a nose at Britain, they identified themselves as innocent traveling salesmen of sports supplements.

SHARE YOUR THOUGHTS Should the U.S. and Russia be using sea mammals for military purposes? Join the conversation below.

The Skripal affair illustrates the darker side of alleged Russian influence on Western soil—denied by Moscow—from targeted killings to money laundering. But the West tends to fixate on “shiny objects” from Russia, Mr. Giles said, such as social media posts and English-language propaganda channel RT.

And spy-whales. The military training of sea mammals is the kind of program that feeds images of the Russians as comic-book masterminds harnessing the superpowers of animals in pursuit of global influence. State media has drip-fed details of the program in recent years, including a report by the Russian army’s TV channel in 2017 that touted successes in Murmansk training seals, sea lions and beluga whales as “underwater special forces.”

The Kremlin, like the U.S., has for decades sought to use the sonar of sea mammals to spot mines, enemy divers and lost equipment.

Irina Novozhilova, an animal-rights activist who has petitioned the Russian Defense Ministry to end its use of sea mammals, says the military usefulness of dolphins and whales is also exaggerated.

“It doesn’t matter what you strap on a dolphin,” she said, “it’ll never be James Bond.”

Write to James Marson at james.marson@wsj.com and Thomas Grove at thomas.grove@wsj.com

Corrections & Amplifications

A mission near London in 2018 that U.K. officials said was carried out by Russian military-intelligence officers to murder a former colleague, Sergei Skripal, ostensibly failed. An earlier version of this article incorrectly stated the year of the mission as 2017. (May 11, 2019)

Source: Xinhua| 2019-05-12 21:20:38|Editor: Liangyu

Video Player Close

BEIJING, May 12 (Xinhua) -- China has unveiled "the Implementation Plan for the National Ecological Civilization Pilot Zone (Hainan)," foreseeing comprehensive experiments of ecological civilization system reform to be carried out in the southern island province.

Jointly issued by the General Office of the Communist Party of China (CPC) Central Committee and the General Office of the State Council, the document vows to bring about a new pattern of harmonious coexistence of man and nature in China's modernization drive and write a chapter of Hainan for building a Beautiful China.

The pilot zone aims at reaching world leading level in terms of environmental quality and resource utilization efficiency, according to the plan.

The zone will focus on developing a system for building an ecological civilization, optimizing spatial distribution of land, coordinating development and conservation of land and sea, improving environmental quality and resource utilization efficiency, realizing ecological products' values, promoting green production modes and lifestyle, and other aspects of exploration.

(Photo : Pixabay)

Engineers from Washington State University have developed a replacement for Styrofoam. The material is plant-based and is environmetnally-friendly.

Nanocrystals of cellulose comprise the foam. Cellulose is the most abundant plant material on earth. The foam can be produced through a simple and environmentally-friendly process with the use of water instead of other chemicals as solvents. The findings of the study have been published in the journal Carbohydrate Polymers.

The team is led by Amir Ameli, assistant professor in the School of Mechanical and Materials Engineering, and Xiao Zhang, associate professor in the Gene and Linda School of Chemical Engineering and Bioengineering.

Petroleum-based styrofoam is the material used in building and construction, coffee cups, transportation, and packaging industries. However, it uses toxic ingredients as its raw material, needs to be degraded in an artificial manner, uses petroleum, and produces toxic gases when burned.

Other scientists exerted effort in other cellulose-based foams. However, their performance is not at par with Styforoam.

"In their work, the WSU team created a material that is made of about 75 percent cellulose nanocrystals from wood pulp. They added polyvinyl alcohol, another polymer that bonds with the nanocellulose crystals and makes the resultant foams more elastic. The material that they created contains a uniform cellular structure that means it is a good insulator. For the first time, the researchers report, the plant-based material surpassed the insulation capabilities of Styrofoam. It is also very lightweight and can support up to 200 times its weight without changing shape. It degrades well, and burning it doesn't produce polluting ash," according to Nanowerk.

"We have used an easy method to make high-performance, composite foams based on nanocrystalline cellulose with an excellent combination of thermal insulation capability and mechanical properties," Ameli said. "Our results demonstrate the potential of renewable materials, such as nanocellulose, for high-performance thermal insulation materials that can contribute to energy savings, less usage of petroleum-based materials, and reduction of adverse environmental impacts."

"This is a fundamental demonstration of the potential of nanocrystalline cellulose as an important industrial material," Zhang said. "This promising material has many desirable properties, and to be able to transfer these properties to a bulk scale for the first time through this engineered approach is very exciting."The researchers are now developing formulations for stronger and more durable materials for practical applications. They are interested in incorporating low-cost feedstocks to make a commercially viable product and considering how to move from laboratory to a real-world manufacturing scale.

ارتفعت إيرادات محطتي البضائع العامة والحاويات بميناء صلالة بنسبة 23% و 3% على التوالي في الربع الأول من عام 2019، وتعاملت محطة البضائع العامة مع 4.234 مليون طن من البضاعة العامة بالربع الأول من العام الجاري، بزيادة قدرها 3% مقارنة بالربع الأول من عام 2018.

وتمثلت السلع الرئيسية التي تم التعامل معها في الحجر الجيري والجبس والميثانول والاسمنت، حيث يتم تصديرها من صلالة إلى الأسواق المجاورة، والتي تشكل المحرك الرئيسي لأعمال المحطة. فيما انخفضت أحجام الحاويات المناولة بالميناء إلى 912 ألف حاوية نمطية خلال الربع الأول من 2019 وبنسبة 12%، مقارنة بـ 1.032 مليون حاوية للفترة المماثلة من 2018. وعزت شركة صلالة لخدمات الموانئ هذا الهبوط إلى النقص الحاصل في الطاقة الاستيعابية المتاحة بسبب تأثيرات إعصار «مكونو» العام الماضي.

وفيما يتعلق بالإنتاجية قالت الشركة إن محطة الحاويات سجلت ارتفاعا طفيفا في حركات الرصيف خلال ساعة واحدة بالربع الأول من 2019، مؤكدة على تركيزها لتحسين مستويات الإنتاجية. وبلغت الأرباح الصافية مجتمعة للشركة 1.625 مليون ريال خلال الربع الأول من العام الحالي، مقارنة بـ 1.720 مليون ريال للفترة نفسها من 2018.

وسجلت المدخولات قبل خصم الضرائب والفوائد والاستهلاك 4.523 مليون ريال للربع الأول من 2019. وأوضحت الشركة أن تسهيلات محطة الحاويات ما زالت تواجه نقصا في القدرة التشغيلية الآمنة بسبب إجراءات تقييم الأضرار وصيانة المعدات وإعادتها لحالتها الأولى التي تعرض لها الميناء جراء إعصار «مكونو»، ووصلت النفقات الإجمالية خلال الربع الأول من عام 2019 إلى 1.165 مليون ريال والتي تتضمن التكاليف المتعلقة بالإعصار ، ولا تزال عملية دراسة مطالبات التأمين جارية.

وثيقة التأمين وأكدت الشركة على استقرار أعمال الشحن الإقليمية والتي تشكل العمود الفقري لمحطة الحاويات بميناء صلالة، حيث لا تزال المحطة تعمل ضمن طاقتها الاستيعابية الآمنة المنخفضة نتيجة لتأثيرات الإعصار، ومن المتوقع أن تتم العودة إلى مستويات الطاقة الاستيعابية الأصلية في الربع الثالث من العام الجاري، مع توقع استكمال الصيانات وتسليم المعدات، كما أن إدارة الميناء تعمل بشكل نشط مع الزبائن الحاليين والمحتملين لملء الزيادة في الطاقة الاستيعابية. وما زالت أعمال محطة البضائع العامة مستقرة وقد لوحظ ثبات منحنى النمو في صادرات البضائع المجمعة بالربع الأول من 2019 مقارنة بنفس الفترة من العام الماضي.

وقالت الشركة إن المطالبة المالية عن الأضرار التي ألحقها الإعصار «مكونو» أدت إلى عدم تشجيع شركات التأمين الكبرى لتجديد عقد التأمين وإلى زيادة كبيرة في قسط التأمين، وقد تم تجديد وثيقة التأمين الحالية الخاصة بالميناء والتي انتهت بنهاية مارس الماضي، بزيادة على قسط التأمين بمبلغ 2.416 مليون ريال سنويا.

3% respectively in the first quarter of 2019, and handled the general cargo terminal with 4.234 million tons of general cargo in the first quarter of this year, an increase of 3% compared to the first quarter of 2018. The main commodities dealt with were limestone, gypsum, methanol and cement, exported from Salalah to neighboring markets, which are the main engine of the station's operations. The volume of containers handling the port decreased to 912 thousand TEUs during the first quarter of 2019 and by 12% compared to 1.032 million TEUs for the same period of 2018. Salalah Port Services attributed this decline to the shortage of capacity available due to the effects of hurricane «Mkono» last year.

وأكدت الشركة على أن الإدارة تواصل تنفيذ استراتيجيتها التجارية من أجل تنويع البضائع والسلع. ويواصل الميناء تطوير قاعدته الصلبة والاستفادة من شبكة الربط الحالية وقاعدة زبائنه من أجل دعم تطوير النشاط الاقتصادي. النمو التجاري العالمي وأشارت الشركة إلى أن النمو التجاري العالمي يفقد زخمه نزولا من 4.6% في 2017 إلى 3% في 2018، مع توقعات منظمة التجارة العالمية أن يواصل هبوطه إلى حوالي 2.7% خلال 2019، وقد أرجعت المنظمة هذا الانخفاض إلى التوترات التجارية المتنامية مع تزايد مخاطر فرض تعريفات جديدة واتخاذ إجراءات مماثلة للرد عليها مما يؤثر على النمو التجاري.

وقد بدأت خطوط الشحن تشعر بهذا التأثير على معدلات التجارة الرئيسية بين آسيا وأوروبا، التي انخفضت إلى أدنى مستوى لها خلال 12 شهرا. وقالت الشركة إن المؤشرات العالمية تؤكد أن شركات الشحن تركز على زيادة أحجام أسطولها من السفن مما يتطلب قيام محطات محورية مثل صلالة بالاستثمار في تطوير ورفع مستوى طاقاتها الاستيعابية لتتمكن من مناولة السفن ذات الأحجام الكبيرة بشكل آمن.

The company noted that global business growth is losing its momentum down from 4.6% in 2017 to 3% in 2018, with the WTO forecast that it will continue to decline to about 2.7% by 2019, the و

omandaily

China April crude steel production rises 12.7% y/y - stats bureau + more data

* China April crude steel output rose 12.7% year-on-year to 85.03 million tonnes, according to data released by the National Bureau of Statistics on Wednesday.

* China Jan-April crude steel output up 10.1% y/y at 314.96 mln tonnes - stats bureau

* China Jan-April coke output up 6.5% y/y at 151.84 mln tonnes - stats bureau

* China April coke output up 3.4% y/y at 38.99 mln tonnes - stats bureau

* China April coal output up 0.1% y/y at 294.29 mln tonnes - stats bureau

* China Jan-April coal output up 0.6% y/y at 1.11 bln tonnes - stats bureau

* China Jan-April crude oil throughput up 4.7% y/y at 207.47 mln tonnes - stats bureau

* China April crude oil throughput up 5.1% y/y at 52.1 mln tonnes - stats bureau

* China April power generation up 3.8% y/y at 544 bln kWh - stats bureau

* China Jan-April power generation up 4.1% y/y at 2.22 trln kWh - stats bureau

* China April non-ferrous output up 4.9% y/y at 4.74 mln tonnes - stats bureau

* China Jan-April non-ferrous output up 5.2% y/y at 18.64 mln tonnes - stats bureau

Growth in China’s industrial output slowed more than expected to 5.4 percent in April from a 4-1/2 year high in March, reinforcing views Beijing will have to roll out more stimulus measures as a trade war with the United States intensifies.

Analysts polled by Reuters had forecast industrial output would grow 6.5%, slowing from an unexpectedly strong 8.5% in March.

Fixed-asset investment rose 6.1% in January-April from the same period last year, also lagging expectations, the National Bureau of Statistics said on Wednesday.

Analysts had predicted a 6.4% increase, picking up slightly from 6.3% in January-March.

Private-sector fixed-asset investment, which accounts for about 60 percent of overall investment in China, rose 5.5% in the same period, compared with a increase of 6.4% in the first three months of the year.

Retail sales rose 7.2% in April on-year, the slowest pace since May 2003, sharply down from March’s 8.7% and missing a forecast rise of 8.6%.

The United States escalated a tariff war with China on Friday by hiking levies on $200 billion worth of Chinese goods in the midst of last-ditch talks to rescue a trade deal. China retaliated on Monday, though on a smaller scale.

The U.S. move comes as China’s economy was beginning to show tentative signs of improvement after a flurry of support measures, though analysts had cautioned it was too early to call a recovery.

Economists at Citi estimate the U.S. tariff increase could lop 50 basis points off China’s GDP growth, reduce exports by 2.7 percent and cost the country another 2.1 million jobs, though they are optimistic a trade deal will be reached eventually.

Looking today at week-over-week shares outstanding changes among the universe of ETFs covered at ETF Channel , one standout is the Gold Miners ETF (Symbol: GDX) where we have detected an approximate $104.2 million dollar outflow -- that's a 1.1% decrease week over week (from 436,702,500 to 431,702,500). Among the largest underlying components of GDX, in trading today Newmont Goldcorp Corp (Symbol: NEM) is trading flat, Barrick Gold Corp. (Symbol: GOLD) is up about 0.8%, and Franco-Nevada Corp (Symbol: FNV) is up by about 1%. For a complete list of holdings, visit the GDX Holdings page » The chart below shows the one year price performance of GDX, versus its 200 day moving average:

Looking at the chart above, GDX's low point in its 52 week range is $17.28 per share, with $23.70 as the 52 week high point - that compares with a last trade of $20.93. Comparing the most recent share price to the 200 day moving average can also be a useful technical analysis technique -- learn more about the 200 day moving average »

Exchange traded funds (ETFs) trade just like stocks, but instead of ''shares'' investors are actually buying and selling ''units''. These ''units'' can be traded back and forth just like stocks, but can also be created or destroyed to accommodate investor demand. Each week we monitor the week-over-week change in shares outstanding data, to keep a lookout for those ETFs experiencing notable inflows (many new units created) or outflows (many old units destroyed). Creation of new units will mean the underlying holdings of the ETF need to be purchased, while destruction of units involves selling underlying holdings, so large flows can also impact the individual components held within ETFs.

Click here to find out which 9 other ETFs experienced notable outflows »

The PMI index of non-hydrocarbon private sector companies in Qatar recently confirmed an increase in new business volumes at the beginning of the second quarter of 2019. At the same time, the level of confidence for future production reached its third strongest level since the start of the study in April 2017.

More than three-quarters of participating companies expected their business units to grow over the next 12 months, although the index fell slightly from March, but growing demand for new businesses bolsters the companies' optimistic outlook for overall future business activity.

Qatar's main PMI fell slightly from 50.1 points in March to 48.9 in April. Although the recent reading recorded 48.6 points in the last quarter of 2018 above the average, it was below the trend of the first quarter of 2019 (49.7 points). The monthly decline in the PMI index mainly reflects slower growth in new orders and lower production as well as employment indicators.

.

lusailnews

Cass Freight Index Report

Negative Shipment Volume Hits Five Months in a Row Economic Contraction or Only Retrenchment?

April 2019 Year-over-year change 2 year stacked change Month-to-month change Shipments 1.194 -3.2% 6.6% -0.3% Expenditures 2.909 6.2% 19.8% 0.7% Continued decline in the Cass Freight Shipments Index continues to concern us:

• When the December 2018 Cass Shipments Index was negative for the first time in 24 months, we dismissed the decline as reflective of a tough comparison. When January 2019 was also negative, we again made rationalizations. Then February was down -2.1% and we said, “While we are still not ready to turn completely negative in our outlook, we do think it is prudent to become more alert to each additional incoming data point on freight flow volume, and are more cautious today than we have been since we began predicting the recovery of the U.S. industrial economy and the rebirth of the U.S. consumer economy in the third quarter of 2016.”

• When March was down -1.0%, we warned that we were preparing to ‘change tack’ in our economic outlook.

• With April down -3.2%, we see material and growing downside risk to the economic outlook. We acknowledge that: all of these still relatively small negative percentages are against extremely tough comparisons; the two-year stacked increase was 6.6% for April; and the Cass Shipments Index has gone negative before without being followed by a negative GDP. We also submit that at a minimum, business expansion plans should be moderated or have contingency plans for economic contraction included.

• The initial Q1 ’19 GDP report of 3.2% suggests the economy is growing faster than is reflected in the Cass Shipments Index. Our devolvement of GDP explains why the apparent disconnect is not as significant as it first appears.

• The weakness in spot market pricing for many transportation services, especially trucking, is consistent with the negative Cass Shipments Index and, along with airfreight and railroad volume data, heightens our concerns about the economy and the risk of ongoing trade policy disputes.

Consumer appliance manufacturers in China are moving production outside the country to avoid exposure to the China-US tariff disputes, altering aluminium and other metal supply chains, market sources said Wednesday.

Panasonic has moved production of car air conditioning units to Thailand and Malaysia from China, while Daikin plans to move some aluminium compressor production to Thailand, the companies said.

Key Chinese home appliance producers are relocating capacities too, China Household Electrical Appliance Association said Wednesday.

The tariffs would affect air conditioning units, refrigerators and washing machines exported from China to the US in the near term.

"It is like the whole of China coming to Vietnam," a Hanoi-based trader said.

Relocation is not happening as fast as companies had hoped. Daikin is only moving some aluminium compressor production, and other components will continue to be made in China, a company spokeswoman said.

Production transfers need to satisfy an internal standard called 4M, covering method of production, worker skills, material, and management, a Daikin source said.

Some consumer products do not allow switches in raw materials without being tested by the final end-users, and the first step of relocation would be changing delivery destination of raw materials. Shipping has become congested as companies are rerouting container deliveries to Southeast Asia, sources said.

"Due to constraints in logistics, relocation has been slow," an aluminium consumer source said.

Home appliances use devices made of aluminium foil condensers.

"The trade tensions are hitting Japanese device exports, mostly to China, and aluminium condenser demand used for the devices," a Japanese trader said.

Condensers are made of aluminium of 99.7% or higher purity.

Japan's aluminium foil shipments to condenser makers were 7,343 mt in the first quarter, down 9.7% year on year, the Japan Aluminium Association said.

China’s environment ministry has deployed nearly 1,000 inspectors to 25 cities and provinces across the country for its first round of “intensified anti-pollution inspections”.

The checks will focus on 26 environmental aspects, including potable water protection, solid waste imports, urban sewage renovation and water pollution improvement alongside Yangtze River regions.

A total of 981 inspectors were sent to key anti-pollution regions such as Beijing-Tianjin-Hebei, Shanxi-Shaanxi-Henan (known as Fenwei plain) and Yangtze River Delta regions, according to a statement published on the website of the Ministry of Ecology and Environment (MEE) earlier this week.

That came as the ruling Communist Party last year vowed to impose limits on the number of central government inspection campaigns directed at local authorities.

The environment ministry has previously launched several rounds of inspections in 27 different forms.

The intensified checks starts from May 15 and will run until May 25, with an aim to help local authorities to identify problems that require improvement. The same group of inspectors will revisit the regions between September and October to check if the problems have been solved.

“Inspectors will reduce meetings and paper works during the intensified checks, in order to improve efficiency and avoid repeatedly disturbing normal work of local authorities,” said Cao Liping, director of ecological regulation enforcement bureau at the MEE, at its monthly news briefing in April.

Meanwhile, the MEE has also carried out a fresh round of checks on air pollution from May 8, focusing on 39 cities in Beijing-Tianjin-Hebei and Fenwei plain.

A majority of the 39 cities failed to meet their anti-smog targets over the past winter.

“We will hold accountability of local officials in the region missing the targets and send inspectors and experts to help them improve air quality,” said Liu Youbin, MEE spokesman, at the news briefing.

China set mandatory renewable power quotas for each of its region for 2019 and 2020, the National Energy Administration (NEA) said on Wednesday, in an attempt to promote the use of clean energy in the country.

Local grid companies will have to purchase a certain volume of electricity from renewable energy generators, the NEA said.

The targets, setting as a portion of renewable energy use in total energy mix, vary from 10% in eastern province of Shandong to as high as 88% in southwestern province of Sichuan in 2019 based on their energy structure.

The draft plan was launched in November.

Apart from checks from local authorities, central government will also deploy inspectors to monitor the implementation of the policy, the NEA statement said.

China’s state media signaled a lack of interest in resuming trade talks with the U.S. under the current threat to escalate tariffs, while the government said stimulus will be stepped up to buttress the domestic economy.

Without new moves that show the U.S. is sincere, it is meaningless for its officials to come to China and have trade talks, according to a commentary by the blog Taoran Notes, which was carried by state-run Xinhua News Agency and the People’s Daily, the Communist Party’s mouthpiece. The Ministry of Commerce spokesman said Thursday he had no information about any U.S. officials coming to Beijing for further talks.

The indications that negotiations are paused will focus attention on the next opportunity for Presidents Xi Jinping and Donald Trump to meet -- at the Group of Twenty meeting in Japan next month. Their meeting in Argentina in December last year put negotiations back on track, only for them to fall apart again this month in Washington.

"If the U.S. doesn’t make concessions in key issues, there is little point for China to resume talks," said Zhou Xiaoming, a former commerce ministry official and diplomat. "China’s stance has become more hard-line and it’s in no rush for a deal" because the U.S. approach is extremely repellent and China has no illusions about U.S. sincerity, he said.

No Rush for a Deal

According to Zhou, the commerce ministry spokesman on Thursday effectively ruled out talks in the near term. In comments to the media, ministry spokesman Gao Feng said that China’s three major concerns need to be addressed before any deal can be reached, adding that the unilateral escalation of tensions in Washington recently had “seriously hurt" talks.

U.S. Treasury Secretary Steven Mnuchin said this week that American officials “most likely will go to Beijing at some point” in the near future to continue trade talks, before later saying he has “no plans yet to go to China.”

On Friday, China’s government said that it will work to counteract the effects of more U.S. tariffs and keep the economy in a "reasonable range." The National Development and Reform Commission is studying the impact of U.S. tariffs and will roll out "responsive measures when necessary," spokeswoman Meng Wei said at briefing in Beijing.

A sharper and more aggressive tone in state media doesn’t rule out short-term progress in trade talks, as rhetoric can be dialed back just as quickly. However, after months of downplaying the dispute with the U.S. and banning the phrase "trade war," the new strident tone of coverage is striking.

The U.S. has been talking about wanting to continue the negotiations, but in the meantime it has been playing “little tricks to disrupt the atmosphere,” according to the Taoran commentary on Thursday night, citing Trump’s steps this week to curb Chinese telecom giant Huawei Technologies Co.

“We can’t see the U.S. has any substantial sincerity in pushing forward the talks. Rather, it is expanding extreme pressure,” the blog wrote. “If the U.S. ignores the will of the Chinese people, then it probably won’t get an effective response from the Chinese side,” it added.

The Shanghai Composite Index was 1.7% lower at 1:38 p.m. in Shanghai, putting it on course for a fourth week of losses, the worst streak in 10 months. The offshore yuan had weakened more than 0.4% to 6.9395 per dollar.

The blog reiterated China’s three main concerns for a deal are tariff removal, achievable purchase plans and a balanced agreement text, as first revealed by Vice Premier Liu He. They mark the official stance as much as the will of the Chinese public, it wrote.

“If anyone thinks the Chinese side is just bluffing, that will be the most significant misjudgment” since the Korean War, it said.

In addition to putting the Taoran commentary on WeChat, the People’s Daily newspaper had three defiant articles on the trade war in the physical newspaper Friday.

A front page commentary from the Communist Party’s propaganda department headlined ‘No Power Can Stop the Chinese People from Achieving Their Dream’ said “the trade war will not cripple China, it will only strengthen us as we endure it,” citing the hardships China has overcome from the Opium War to floods to the SARS epidemic in 2002-2003.

There were two editorials on page three, with one saying “China doesn’t intend to change or replace the U.S., and the U.S. can’t dictate to China or hold back our development.” The other said claims from some officials in the U.S. that they have “rebuilt” China over the past 25 years are “outrageous” and shows their vanity, ignorance and distorted mentalities.

https://www.bloomberg.com/news/articles/2019-05-17/china-not-interested-in-talking-with-u-s-for-now-state-media

قال سفير ايران لدى نيودلهي علي جكيني: إن الجمهورية الاسلامية الايرانية طرف موثوق به قادر على توفير الطاقة للهند، مؤكداً أن الهند لا تتجاهل هذا الواقع.

وفي تصريح له لصحيفة (إينديا تايمز)، أضاف جكيني: ان الهند ستتخذ قرارها بشأن استيرادها النفط وفق أمنها القومي وحاجتها الى الطاقة، مشيراً الى العلاقات الثنائية بين البلدين والمشتركات الممتدة الى قرون سابقة.

واعتبر سفير ايران لدى نيودلهي الحظر المتفرد الأمريكي نقضاً لسيادة وحرية الدول المستقلة، لافتاً الى حق ايران في تصدير النفط وإلى عدم استطاعة أي طرف منعها عن تصدير النفط.

وتطرق جكيني، خلال المقابلة، الى مواصلة التعاون بين ايران والهند في تنمية ميناء جابهار، وقال: إن الكثير من الدول راغبة في الاستثمار في جابهار نظراً لإيلاء ايران أولوية لذلك.

وأعرب عن اعتقاده بأن الهند لاعبة مركزية في الساحة الدولية وفي المنطقة وقادرة على توظيف آلية الدبلوماسية والحل السلمي لحث الدول على إقامة العدالة. وتعتبر الهند بعد الصين ثاني أكبر بلد يشتري النفط من ايران، حيث بلغ حجم النفط الذي إشترته من ايران الى 24 مليون طن حتى نهاية العام المالي في 30 مارس

al-vefagh

Four commercial vessels were targeted by "sabotage operations" near the territorial waters of the United Arab Emirates, the UAE foreign ministry said in a statement on Sunday, adding that there were no victims.

"Subjecting commercial vessels to sabotage operations and threatening the lives of their crew is considered a dangerous development," the ministry said in a statement that was tweeted by the official news agency WAM.

Saudi Arabia's Energy Minister Khalid al-Falih said on Monday that two Saudi oil tankers were targeted on Sunday in "a sabotage attack" off the coast of Fujairah, part of the United Arab Emirates, threatening the security of global oil supplies.

Iran's response:

In response, Iran's foreign ministry spokesman Abbas Mousavi called the incidents “worrisome and dreadful”, and asked for an investigation into aspects of the matter.

Mousavi was cited by the semi-official ISNA news agency as saying “such incidents have negative impact on maritime transportation security”, and asking for regional countries to be “vigilant against destabilizing plots of foreign agents."

U.S. refiners had a plan for 2020: use their complex operations to maximize profits by making products that would comply with new international laws capping sulphur content in shipping fuels.

But after a series of unexpected market moves, heavy, sour crude oil processed by U.S. refiners has become more expensive, eating up hoped-for profit windfalls before they even materialized, forcing refiners to rethink plans to invest more in heavy crude processing units.

New regulations by the International Maritime Organization (IMO) will require ships globally to use fuels with a sulphur content below 0.5% beginning in 2020. Current shipping fuel is much dirtier, with a higher sulphur content.

The move was expected to make heavy crude oil cheap as most refiners worldwide shifted to lighter crudes that yield compliant lower-sulphur fuels - and benefit complex U.S. refiners that possess greater capability to break down that heavy crude into high-margin products.

Instead, global heavy crude supplies have become scarce due to sanctions on Venezuela, one of the world’s biggest heavy producers, pipeline bottlenecks in Canada and OPEC output cuts. The Organization of the Petroleum Exporting Countries’ April output fell to 30.23 million barrels per day (bpd), the lowest since 2015.

“The biggest single factor is the big loss of heavy crude,” said Todd Fredin, executive vice president of supply, trading and logistics at Motiva Enterprises, which operates a 603,000 bpd operation in Port Arthur, Texas, the largest U.S. refinery. The benefit to complex refiners from the regulatory change “is going to be less than people thought,” he said.

Heavy crude once fetched a big discount compared with light crude, but it has narrowed after sanctions on Iran and Venezuela. That weighed on first-quarter earnings for major independent refiners Valero Energy Corp and Phillips 66 .

Marathon Petroleum Corp this week halted plans to add a coking unit to its Garyville, Louisiana refinery that would have processed more heavy crude. Marathon said the coker, which was expected to come online in 2021, was no longer financially viable due to narrowed spreads.

U.S. refiners rely on cokers to break down residual oils into other refined products, including gasoil and naphtha. Refineries without that capability typically process more light crude, produced in abundance by the United States, versus heavy crude, which U.S. refiners have to import.

The price difference between U.S. Gulf Coast grades Louisiana Light Sweet (LLS) and Mars, the best proxy for comparing light, sweet and heavy, sour crude in the U.S. Gulf, has narrowed in the last few months.

LLS’s premium over Mars on Thursday was $2.05 per barrel, compared to $4.25 per barrel in mid-November, according to Refinitiv Eikon data. At one point in February, Mars traded at a premium to lighter LLS, the first time that has happened since 2011.

Some analysts said crude volumes processed may have to be cut, but so far that has not happened. “We really see the narrowing of the spreads to be a short-term issue,” Marathon Chief Executive Gary Heminger told Reuters, saying the company is keeping their existing coking units full.

Prices of heavy crude will likely remain high as traditional heavy suppliers like Canada and Mexico grapple with infrastructure and production constraints, said Michael Tran, an analyst at RBC Capital Markets.

“There’s not many countries that can step up to the plate” to make up for the loss, he said.

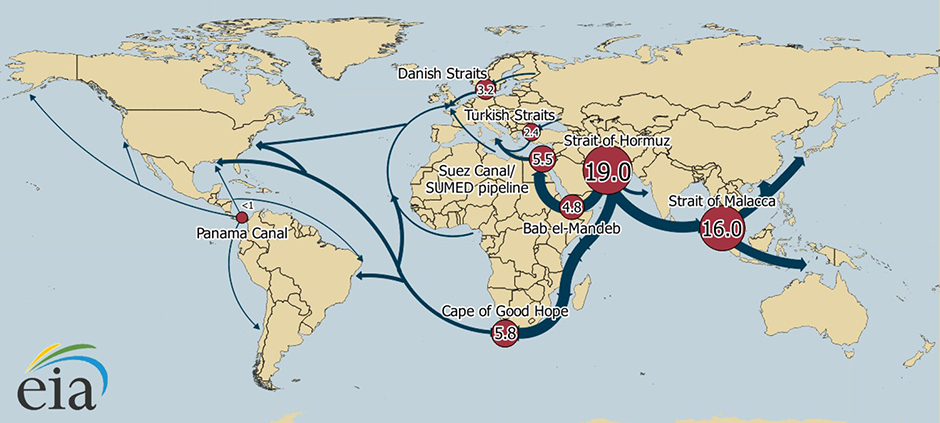

Oil refiners across Asia are bidding up crude prices from Abu Dhabi to Oman as they compete for supplies to make up for lost Iranian and Venezuelan exports.

July-loading cargoes of grades such as Murban and Das were bid at premiums of $0.80 to $0.85/bbl above the official selling price on Friday on an electronic trading platform operated by S&P Global Platts. That would be the highest spot differentials in at least three years for the grades, according to data compiled by Bloomberg. Upper Zakum crude was also bid at a $0.65 premium, while Umm Lulu changed hands at a $0.95 premium. The higher bids came even after Abu Dhabi National Oil hiked the official price of its crude earlier this week.

Buyers across the world’s top oil-importing region are scrambling for oil as U.S. sanctions on Iran and Venezuela tighten supplies of high-sulfur crude that their refineries are designed to process. Unplanned disruptions to Russian and Nigerian flows and concerns that fighting in Libya could affect oil exports also contributed to the fervor to secure cargoes.

Oman crude futures climbed to a premium of $3.10/bbl over swaps for Dubai oil, the benchmark grade for the Middle East. That’s its highest premium since September, when markets were spooked by the prospect of U.S. sanctions putting an end to Iranian exports.

A wide discount between the Dubai benchmark and Brent, the marker for more than half the world’s oil supplies, is also contributing to the strong interest for Middle Eastern grades. Dubai’s discount to Brent futures was more than $3/bbl on Friday, near the highest level in seven months.

Investor Drexel Hamilton Infrastructure Partners LP and rail operator Rio Grande Pacific Corp on Friday disclosed plans to build a $1.5 billion rail line that would transport heavy crude from Utah to connections to the U.S. Gulf Coast.

Drexel Hamilton and Rio Grande officials said the project aims to deliver about 400,000 barrels per day (bpd) of Uinta basin crude to Gulf Coast refineries looking to replace heavy oil supplies from Venezuela.

“The Uinta has only been restricted from Gulf Coast and overseas refiners as a result of limited takeaway capacity,” said Mark Michel, a managing partner at private equity fund Drexel Hamilton. “We are going to change that.”

Uinta Basin oil now is trucked to Salt Lake City refineries because it is too thick to put into a pipeline, Robert Bach, president of Rio Grande said in an interview. “This (Gulf Coast) market is much bigger.”

The proposed project would include at least one terminal able to load crude onto trains and to receive sand used in hydraulic fracturing. The rail line will be contingent on receiving commitments from oil producers, Bach said.

The Seven County Infrastructure Coalition, a Utah regional planning group, on Friday approved terms of a preliminary agreement with Drexel Hamilton to build the railroad.

Rio Grande owns four short-line railroads in Texas, Louisiana, Oklahoma and other states. The proposed rail line would extend 80 miles between connections with Union Pacific and BNSF Railway near Soldier Summit, Utah and potential terminal locations in the Uinta basin near U.S. oil producers.

“There was never enough momentum behind this before,” Bach said, explaining that U.S. sanctions on Venezuela’s state-run PDVSA oil company, a former major supplier of heavy crude to the U.S., helped spur demand.

The U.S. Coast Guard said on Saturday it’s too early to estimate when the Houston Ship Channel can reopen after a collision that spilled about 9,000 bbl of a gasoline ingredient into the water.

Friday’s collision involved the tanker Genesis River and a tug transporting two barges carrying more than 2 million gallons of reformate, an oil-refining byproduct used to make gasoline. One barge capsized and the other was damaged following the incident that occurred 2 1/2 mi east and south of the Bayport terminal.

“Our objective today is to secure the vessels,” U.S. Coast Guard Captain Kevin Oditt told reporters. “Once we have those vessels secured, we will work with the pilots and we will evaluate whether we can reopen the ship channel.”

The Houston Ship Channel is the city’s lifeline to the Gulf of Mexico and to foreign markets. Oil shippers, refiners, chemical manufacturers and grain exporters rely on the waterway to receive and deliver everything from crude to corn.

The Coast Guard established an emergency temporary safety zone and closure of the Clear Creek Channel from the entrance to Clear Lake extending east to Light 66 and north up to but not including the Bayport Ship Channel, it said in a statement. The area between Light 61 and Light 75 was also shut.

The spill was pinpointed by the National Weather Service as a possible source of the gasoline-like scent wafting across Houston’s eastern suburbs. Teams of air monitors were working around the clock to assess levels.

“To date, those teams have taken over 1,300 samples and, in all cases, the samples taken have not exceeded the established action levels,” said Craig Kartye of the oil spill prevention and response program at the Texas General Land Office.

About 3,600 ft of boom has been put in place and efforts are underway to deploy an additional 12,000 ft in the most pressing areas, said Jim Guidry, executive vice president of vessel operations for Kirby Inland Marine, operator of the tug involved.

While one of the barges has lost about 9,000 bbl of reformate, the capsized vessel hasn’t leaked any cargo at this time, he said.

“We are continuing to work with the Coast Guard and the other federal regulators to understand the cause of the incident and will be working to recover any of the spilled product and mitigate the impact on the environment,” Guidry said.

Norwegian oil and gas player Aker BP has failed to find hydrocarbons after drilling a wildcat well in the North Sea offshore Norway.

The Norwegian Petroleum Directorate (NPD) said that the well 25/11-29 S was drilled on the Utsira High, about 14 kilometers south of the Grane field and 190 kilometers west of Stavanger in the central part of the North Sea.

The primary exploration target for the well was to prove oil in reservoir rocks of Early Jurassic age in the Statfjord group. The secondary exploration target was to prove oil in reservoir rocks of Paleocene age in the Heimdal formation.

The well encountered the Statfjord group with a thickness of about 100 meters, of which 65 meters is reservoir rocks with good reservoir quality. The well did not encounter the Heimdal formation. The well is classified as dry. Extensive data acquisition and sampling have been carried out.

It is worth noting that this is the first exploration well in production license 916 which was awarded in APA 2017.

The NPA added that the well was drilled to vertical and measured depths below the sea surface of 2,233 and 2,283 meters respectively, and was terminated in the Zechstein group of Permian age. The well will be permanently plugged and abandoned.

Well 25/11-29 S was drilled by the Deepsea Stavanger drilling rig, which will now proceed to production license 777 in the central part of the North Sea to drill wildcat well 15/6-16 S, where Aker BP is the operator.

Spotted a typo? Have something more to add to the story? Maybe a nice photo? Contact our editorial team via email. Offshore Energy Today, established in 2010, is read by more than 10.000 industry professionals daily.

We had almost 9 million page views in 2018, with 2.4 million new users. This makes us one of the world’s most attractive online platforms in the space of offshore oil and gas.

These stats allow our partners advertising on Offshore Energy Today to get maximum exposure to their online campaigns. If you’re interested in showcasing your company, product or technology on Offshore Energy Today contact our marketing manager Mirza Duran for advertising options.

A tiny South American country until recently known mostly as the location of one of the worst mass suicides in modern history is about to acquire a whole new reputation, and this reputation has to do with its oil wealth.

Guyana, sandwiched between Venezuela and Suriname, has in just a couple of years turned from an empty spot on the international oil map into one of the new hot spots thanks to a series of discoveries offshore, made by Exxon and Hess Corp.

The Stabroek block is the place where the discoveries were made. The first ones came in 2015 and since then, Exxon has been announcing new ones on a more or less regular basis. To date, there have been 12 discoveries, with the reserves associated with them topping 5 billion barrels of oil equivalent.

This is certainly a lot of oil and it could either solve all economic problems of the tiny nation of less than a million people or, as history has sadly proved more than once, become an oil curse. It would all depend on how Guyana handles its future oil wealth.

The BBC’s Simon Maybin noted in an analysis of Guyana’s changing fortunes this week that the country, a former British colony, currently suffers high unemployment and poverty rates. It also has high levels of corruption—a practice that oil wealth has been found to exacerbate more often than not. The billions of dollars in oil revenues to be had also encourage political instability as more groups vie for power and access—preferably exclusive—to the oil dollars.

Already, sings of this political instability are emerging in Guyana, Maybin reports. The coalition in power lost a no-confidence vote last December, but instead of calling elections, which would have been standard procedure, the coalition challenged the result of the vote in court. This has led to demonstrations and a prolonged legal battle that is still not over.

Guyana’s only hope is if it can somehow manage to put a lid on political ambitions and focus on the actual benefits to be reaped when Exxon and Hess begin commercial production, such as improving the living conditions of the poorest Guyanese and reducing unemployment as well as boosting economic growth. Related: Oil Markets Uncertain As Trade War Counters Supply Shortages

Luckily, Guyana has both good and bad examples to look to. Norway is the best good example of how a nation can use its oil money in a productive way and turn into one of the wealthiest in the world without relying excessively on oil but rather on the smart investments of money from this oil.

And then there’s Guyana’s very own neighbor Venezuela, which is a picture of how it shouldn’t be done, namely by neglecting other sectors of the economy in favor of oil, pouring oil money directly in otherwise good social programs and seeing them crumble along with the economy once oil prices drop. Corruption and the resulting authoritarianism to keep control of the oil money are also among Venezuela’s problems that predate the U.S. sanctions. Now, the country is shaken by a perfect storm that could see its oil production obliterated.

So, the world’s new hot spot could either turn into a new Norway or a new Venezuela, Nigeria, Angola, and a host of other countries for whom oil turned from a blessing into a curse. It seems only time will tell which example the country will follow.

By Irina Slav for Oilprice.com

More Top Reads From Oilprice.com:

TEHRAN - Visiting Research Scholar in the CESP Omid Shokri believes that even with massive inspections the U.S. will not be able to drive Iran’s oil export to zero.

To drive Iran’s oil export to zero, the Trump administration said that it will no longer exempt any countries from U.S. sanctions if they continue to buy Iranian oil, stepping up pressure on Iran in a move that primarily affects the five remaining major importers: China and India and U.S. treaty allies Japan, South Korea, Turkey.

To shed more light on the issue we dissussed it with Omid Shokri Kalehsar a Washington-based Senior Energy Security Analyst.

Here is the full text of our interview with him:

Q: Saudi Arabia and the UAE have announced they will compensate for Iranian oil. Is this possible technically?

A: Supply and demand is an important factor in the international oil market. The oil market needs increased supply from major OPEC members and non-members such as Russia. It seems that Saudi, the UAE and Iraq with Russia must produce more oil to overcome the shortage of Iranian oil in the oil market. At present major importers of Iranian oil are looking to find an alternative to Iranian oil because the U.S. did not extend the waiver for Iran’s major oil buyers. India and South Korea are importing more oil from the U.S. and also imported more US LNG, refineries from these both countries are adapting themselves to U.S. oil, they previously imported Iranian oil and are now ready to import U.S. oil. Some analysts believe that the Saudis will be faced with the major problem of increasing their oil output by as much as a million barrels; Saudi Arabia's oil consumption is rising in the warm months due to increased cooling applications and oil consumption rises from 400 to 500,000 bpd.

It is claimed that the other barrier which Saudi Arabia faces in increasing its crude exports is that the government have invested heavily in their refineries and oil products exports over the past years. A unilateral increase in oil output beyond the quotas could impose a requirement for other OPEC members and even eliminate the agreement between OPEC and 10 OPEC non-member countries.

It will possible for Saudi to increase its crude production in the two months of May and June. Saudi Arabia said the country's oil production in the first quarter of this year would be lower than its country's quota, which would allow the country to increase production in those two months. It should be recalled that calculating the compliance of OPEC member states with their oil production quotas is carried out over a six-month period, and the average monthly production of these countries in this six-month period is the basis for judging their compliance with their quotas.

In this way, Saudi Arabia could offset Iranian oil exports from markets by boosting its oil production over the next two months. The decision on the quota for the second six months of this year (July to December) will be taken at the OPEC Ministerial Meeting in Vienna, held in June. Thus, eliminating Iranian oil does not necessarily increase oil prices in the global markets. Some Iranian officials have also confirmed this.

In respect with the United Arab Emirates, which has been proposed as one of the alternatives to Iran's oil market, the country has a production capacity of 3,300,000 barrels per day; its production in 2002 was 2.56 million barrels per day and in 2018 were 3 million and 34 thousand barrels a day. However, according to the latest OPEC announcement, the UAE's oil production in March 2019 amounted to about 3 million and 59 thousand barrels a day. One million barrels will be provided to domestic refineries, and the rest will also be shipped to the export market.

At present some oil producers such as Libya and Venezuela face tensions and political unrest. Currently, aside from Saudi Arabia and the United Arab Emirates, OPEC has no spare capacity. Of course, the commitment to quotas is an important message for the oil market. On the other hand, OPEC or the Consumers' Union is also seriously concerned. If major consumers such as China, India or Turkey form an oil consumer organization, America will not be able to cope with them. Most of OPEC's Middle Eastern countries have focused on Asian markets because the European market has no horizons and the future of the oil market is developing in Asia. In other words, in the current century, they are the largest producers of Asian oil.

Q: The U.S. is making efforts to drive the export of Iranian oil to zero. Is it possible? If not, why?

A: Even a massive inspection will not prevent the sale of quantities of oil. During the Iraqi oil sanctions, despite the international cooperation in this regard, the country was still able to smuggle some of its oil in various ways, including through neighboring countries. Based on this, the U.S. government largely relied on buyer cooperation and fears of a second-round sanction to curb Iran's oil exports. In terms of the oil market, despite the promise of some exporting countries to compensate for any shortages in the market and OPEC's commitment to maintaining price stability in the oil market, full compensation for Iranian oil exports to its technical specifications is not urgent, and given the special discounts that the Iran gives to some importers, small companies who are less concerned about cutting U.S. financial and trading facilities will continue to buy oil shipments.

Some of Iran's oil production is being shipped to China for storage, and part of it is also transported to tankers for informal sales. It seems that Iran could ship 300 to 650 thousand barrels of oil a day, which will not be sold every day. Selling Iranian oil on the grey market is the only way to keep some Iranian share in the oil market. Iran must sell its oil at a low price to find costumers for its oil, while another problem is how to get money from costumers? Another way is for Iranian officials is to sell Iranian oil in the name of another (third) country.

Q: The U.S. is forcing Turkey to stop buying oil from Iran and replace Saudi and Emeriti oil instead of Iranian oil. What are the advantages of Iranian oil for Turkey?

A: The main question for oil traders and political analysts is how much America wants to test these relationships by crippling the Iranian economy. According to the latest official figures available in January, Iran provided more than 12% of Turkey's oil imports. Iraq held 24 percent of the main supply, and Russia provided 15 percent of Turkey's imported oil. Turkey imported only diesel from the UAE in January, and now Iran is the third largest supplier of crude oil for Turkey. 'Iran's oil is not cheap, but there is a major difference in comparison to the prices of Saudi Arabia and the United Arab Emirates,' Turkish Foreign Minister Mevlut Çavusoglu said in Ankara.

Turkey has always defended its commercial ties with its eastern neighbors and considers it a strategic requirement. Iran's oil could be another source of diplomatic controversy between Ankara and Washington, when relations between them are tense due to Turkey's emphasis on purchasing a missile defense system from Russia. Turkey, after some time, will be able to find alternative for Iranian oil; although Turkey prefers to have energy relations with Iran, it seems that Turkey will decrease oil imports from Iran and they may drop to zero in the medium term.

Omid Shokri Kalehsar is a Washington-based Senior Energy Security Analyst, currently serving as a Visiting Research Scholar in the Center for Energy Science and Policy (CESP) and the Schar, School of Policy and Government at George Mason University.

tehrantimes

The lingering oversupply of vessels in the VLCC market has left shipowners weighing options to either idle, reduce sailing speed extensively or take on only short voyages as freight returns are seen below operating costs.

Stay up to date with the latest commodity content. Sign up for our free daily Commodities Bulletin.

Sign Up The Time Charterer Equivalent or TCE, which is the earnings accrued, for a modern VLCC has slumped to around $7,000/day on key Persian Gulf to North Asia routes, which hardly covers the daily running cost of the vessel, according to market participants.

To tide over the staggeringly low earnings period, two shipowners told S&P Global Platts that they have resorted to drifting their vessels to save fuel cost. When a vessel is made to drift in a safe location, the power to the main engine is switched off to save on fuel expenses.

"It makes no sense for owners to accept further lower freight levels at the current TCE levels," a VLCC owner said.

Some shipowners are contemplating to avoid working on any cargoes until the freight returns improve to levels that would cover the operating expenses.

"With earnings so low, [a few shipowners are] doing short voyages, so that the pain is over a lesser amount of time. Not everyone can afford to stop ships," a shipbroker said.

The current TCE has fallen massively from levels seen in January, when owners pocketed around $40,000/day.

The anemic earnings are a result of the early onset of the Asian refinery turnaround season along with the slowdown in US crude exports as well as the flood of newbuilding VLCCs during the first quarter of the year.

So far this year 20 new vessels have been added to the VLCC fleet out of the estimated delivery of 54 ships with fewer vessels deleted to offset the tonnage growth.

"Initially, owners will slow steam to cut bunker costs. [Owners are running vessels] at 12-12.5 knots for laden and 9-11 knots on the ballast [leg]," a second shipbroker said.

Meanwhile, shipowners are yet to resort to laying-up of vessels, a strategy adopted when freight levels are insufficient to cover the running costs.

"When the earnings is below $5,000/day, the owners will start laying-up the more expensive ships in the fleet," the second shipbroker said.

"People will not do lay-up now, but just not fix and wait. Waiting is cheap at current rates," a second VLCC owner said.

Some shipowners are compelled to keep their vessels running due to their business models, while others are opting to keep their vessels waiting at Fujairah in the Persian Gulf or Galle at Sri Lanka's west coast, market sources said.

"Slow speed is already happening and people just prefer to wait than fix. What you may see soon is a bit more activity on the VLCC scrapping," a third VLCC owner said, adding that "lay-up is not a usual option and is the last resort".

Despite shipowners with modern VLCCs resisting to fix their vessels, the stiff competition from those with "handicapped" ships has allowed charterers to pick tonnage at very cheap freight levels. The ships coming out of dry-dock and with fewer approvals from oil majors or inspections by marine industry forums are termed as handicapped vessels.

Platts assessed the key PG-China rate at Worldscale 36.5 on Thursday, basis 270,000 mt, which is equivalent to $6.87/mt, down by w26.5 from when Platts had assessed the rate of the same route at w63 on January 2.

Russia has begun shipping clean oil via the Baltic after a contamination problem disrupted flows for three weeks and it is working to resume supplies by a pipeline to Europe although traders said this might take several more weeks to fix.

High levels of organic chloride, used in oil extraction but which must be removed before being sent to clients, was found in crude pumped to the Baltic port of Ust-Luga and through the Druzhba pipeline in late April, disrupting Russian exports.

Two trading sources told Reuters the level of organic chloride in oil loading at Ust-Luga was back to normal on Monday, after the contamination halted sales. Two other sources said test oil shipments via Druzhba had started to Hungary.

Russia’s Energy Ministry had said on Friday tankers were being loaded with clean oil at Ust-Luga, after the disruptions to exports through the port and Druzhba pipeline drove up global crude prices and left refiners as far west as Germany scrambling to find alternative crude supplies.

Two industry sources said Hungarian energy company MOL was receiving oil via Druzhba as part of a test to see whether the equipment at its sole Danube refinery could process the oil. High levels of organic chloride damages refinery equipment.

Hungary has become the first European country to resume imports, but one of the sources said the organic chloride content in Hungary’s test supplies was still above permitted levels of a maximum norm of 10 parts per million (ppm).

The sources said MOL hoped to restart regular Druzhba intakes from May 17, once it had carried out the tests.

Ukraine said on Saturday it had resumed transfers to European clients via the pipeline’s southern leg to Slovakia, Hungary and Czech Republic. The pipeline, which splits into two branches in Belarus, has a northern spur routed to Poland and Germany.

The Czech government approved on Monday a second loan from state oil reserves for refiner Unipetrol, part of Poland’s PKN Orlen group, for more than 100,000 tonnes of crude to cover for supply interruptions from Russia.

“ENORMOUS” COST

Belarus plans to discuss the contamination crisis in the Slovak capital of Bratislava on May 13-14, Belarusian state firm Belneftekhim said on Monday.

President Alexander Lukashenko said last week Belarus had faced “enormous” costs due to the contamination and expected compensation from Russia, although the mechanism for any compensation and who will pay remains unclear.

Russian pipeline monopoly Transneft blamed unnamed “fraudsters” for the problem. Russian President Vladimir Putin said Transneft lacked a proper mechanism to prevent contamination.

The issue has driven down Russian oil shipments. About 6% less oil was pumped through Transneft’s pipeline network from May 1 to May 12 compared with April’s average, two sources familiar with the shipment data said.

They said oil intake in Transneft’s nationwide network, which handles about 85% of Russia’s total crude output, was about 8.8 million barrels per day (bpd) in the 12-day period, citing data that included oil used at home and export volumes.

At least 5 million tonnes of oil, or about 36.7 million barrels, was tainted with high levels of organic chloride.

Transneft has proposed mixing tainted oil with the clean crude at the Black Sea port of Novorossiisk. Industry sources said levels of the organic chloride at Novorossiisk had risen since early May but remained below 10 ppm limit.

Total Russian oil production has also slipped this month, declining to 11.16 million bpd from May 1 to May 12 from an average of 11.23 million bpd in April, sources said, the lowest output level since June, when it was 11.06 million bpd.

Russia has agreed with the Organization of the Petroleum Exporting Countries and other producers to lower output to shore up global prices, but its May output has now dipped below the target level allowed in the deal of 11.18 million bpd.

Equinor has acquired an additional 22.45% stake in the Caesar Tonga oilfield in the U.S. Gulf of Mexico from Shell for $965 million in cash, the Norwegian company said on Monday.

The acquisition will increase Equinor’s interest in the deepwater field, operated by Andarko, to 46% percent, giving it an additional 15,000 barrels of oil equivalents per day (boepd).

Its current net production from the field is 18,600 boepd, compared to Equinor’s total U.S. Gulf of Mexico production of 110,000 boepd in the first quarter.

“We are pleased to increase our presence in the United States, one of our core areas,” the head of Equinor’s offshore U.S. production, Christopher Golden, said in a statement.

“This is an asset we understand well, and our larger interest will deliver significant additional free cash flow from day one,” he added.

Later this year, Equinor will drill an exploration well at its Monument prospect, which could further increase the company’s foothold in the area, Golden added.

Andarko has a 33.7 percent interest in Caesar Tonga, while Chevron holds the remaining 20.25 percent.

Only one Indian buyer of Iranian oil has taken up Saudi Arabia’s offer of additional oil to make up for the loss of supplies from Tehran due to U.S. sanctions, taking an extra 2 million barrels from the Kingdom for June shipment, industry sources said.

Last month, Saudi Arabia approached Indian buyers offering them additional supplies to compensate for loss of Iranian oil after the United States threatened to sanction entities buying oil from Tehran, the sources said.

The United States had imposed new sanctions on Iran in November last year, but gave a six-month waiver to eight countries, including India, which allowed them to import some Iranian oil.

India was able to buy about 300,000 barrels per day (bpd) of Iranian oil under the waiver. But last month, Washington ended the waivers and said buyers should stop Iranian oil purchases or face sanctions.