China's economy grew at its slowest pace in six years in the first quarter as the latest round of data added to concerns about a loss of momentum.

Official data shows the world’s second largest economy grew at 7 per cent year-on-year, in line with expectations, but slowing from 7.3 per cent in the fourth quarter.

Chinese Premier Li Keqiang announced a growth target of “around 7 per cent” for 2014 last month.

While the GDP figures met expectations, industrial output in March fell well short at 5.6 per cent against a predicted 6.9 per cent.

Retail sales for the month also lagged at 10.2 per cent growth against an expected 10.9 per cent. Similarly, growth in fixed asset investment also underwhelmed at 13.5 per cent against forecasts for 13.9 per cent growth.

On Monday, official data showed a surprise 14.6 per cent collapse in exports in March, adding to worries about the slowing economy.

MGL: Chinese rail shipments: down 10% yoy. China electricity consumption down 6.3% yoy. Chinese bank lending +14% yoy.

Here is Premier Li on growth:

"The U.S. cable reported that Li, who is now a vice premier, focused on just three data points to evaluate Liaoning's economy: electricity consumption, rail cargo volume and bank lending.

"By looking at these three figures, Li said he can measure with relative accuracy the speed of economic growth. All other figures, especially GDP statistics, are 'for reference only,' he said smiling," the cable added."

Of course, now he is in charge, he actually has someone to write the fiction for him. More surreal yet, we have an entire bevy of analysts, strategists and market commentators trying to guess what piece of fiction will be written.

China March power output down 3.7 pct, biggest drop since 2008

China produced 451.1 billion kilowatt-hours (kWh) of power in March, down 3.7 percent compared to the previous year, official data showed on Wednesday, a further sign that an economic slowdown is hurting energy-consuming industries.

Excluding holiday months, the year-on-year decline in power output is the biggest since late 2008, when China's economy was hit by the global financial crisis, with analysts saying the slowdown was the major driver.

"Beijing's decision to remove overcapacity from some industrial sectors has shown some effects on power output, but more importantly, electricity demand was capped by sluggish demand," said Zhou Hao, economist at ANZ Bank in Shanghai.

The figures also suggest that China's "war on pollution" is having an impact on coal-fired power generation, with grids taking more power from clean and renewable sources amid slowing demand.

Output from thermal power stations, most of which run on coal, fell 9.4 percent to 349.7 billion kWh in March, amounting to 77.5 percent of the total. Hydropower generation rose 25.3 percent to 67.6 billion kWh, or 15 percent of the total.

The statistics bureau also said in a statement that China's energy intensity - its consumption per unit of economic growth - fell 5.6 percent year-on-year in the first quarter.

"The large energy intensity reduction is not a surprise - when you have all major energy intensive industries slowing so much, this is what happens," said Tao Wang, resident scholar at the energy and climate programme of the Carnegie-Tsinghua Center for Global Policy in Beijing.

Power generation growth fell to 3.2 percent last year, the slowest rate since the Asian financial crisis, hit by the slowing economy, milder weather and government efforts to improve energy efficiency.

MGL: Oops! Its all confirmation, and history now to our regular readers. If you are surprised or shocked by this number, you have not been reading the tealeaves.

Mr Zhao was detained after opposing the use of force to end the protests in Beijing's Tiananmen Square in 1989.

The former Communist Party leader was under constant house arrest until his death in 2005, and his name is still rarely mentioned in official circles.

"In the past 25 years, China has pursued a path that [Mr] Zhao and his think tanks opposed at that time, becoming the world's second-largest economy. China is using its actions and achievements to answer questions over the sensitive issues," read the article.

Zhao Ziyang was promoted by China's former supreme leader, Deng Xiaoping, who was looking for someone to reform the economy and open up the country to the outside world.

Mr Zhao's position seemed assured when he was made general secretary of the ruling Communist Party in 1987.

MGL: So why is this story important? How does it make us money?

In the first place this story is important because it is a small declaration of victory by the President . It is worth recalling that Zhao opposed Jiang Zemen in his crackdown of the Tiananmen Square movement. There's a distinct smell here of the "Enemy of my enemy is my friend". It certainly one of the first symptoms we've seen of a feeling of security by the ruling faction.

So how does it make us money? China's policy dictates 50% of resource demand. Just look at iron ore, had Jiang Zemen's go-go growth faction been in power we would still have $100 iron ore. So I am going to suggest to you that this politburo is actually quite radical in nature. Yes they've swung right, thats to reap the approval of the military and the core party cadre. Yes, they've hit out at the Jiang Zemen faction-- and hard! That is an endeavour to clear the decks.

So what is President Xi's agenda?

Lee Kuan Yew first met President Xi years before he became president.

Here's an excellent blog from the WSJ on China and Lee Kwan Yew:

"Chinese state media on Monday gave prominent coverage to the death of Singapore’s founding prime minister Lee Kuan Yew, whose brand of paternalistic one-party rule has long been a model for Beijing.

“Mr. Lee Kuan Yew was an old friend of the Chinese people,” Chinese President Xi Jinping wrote to Singapore President Tony Tan in a condolence letter Monday, according to a statement from China’s foreign ministry. “Mr. Lee Kuan Yew and the older generation of Chinese leaders jointly set the course for the development of China-Singapore ties.”

State broadcaster China Central Television devoted nearly half of its midday news bulletin to reports on the former Singaporean leader’s death, while obituaries were splashed across the homepages of websites run by the official Xinhua News Agency and the Communist Party mouthpiece People’s Daily, among others.

“If they change in a pragmatic way, as they have been doing, keeping tight security control and not allowing riots and not allowing rebellions and, at the same time, easing up… it is holdable,” Mr. Lee said, referring to the Communist Party’s ability to keep its grip on political power. “One thing is for sure: the present system will not remain unchanged for the next 50 years.”

Such views have gained credence in Chinese official circles, even if it remains unclear whether they can or will materialize in practice.

While Mr. Lee succeeded arguably because his tiny island state was easier to manage compared to far larger nations like China and India, “many Chinese officials and intellectuals see Singapore as a possible reference point for China,” said Mr. Lam, of the Jamestown Foundation. This, Mr. Lam said, was partly due to the common ethnic roots between China and Mr. Lee’s Singapore, which is dominated by an ethnic Chinese majority while governed under multiracial and secular principles.

In the quarter of a century since Singapore established formal ties with China, thousands of Communist officials and mid-ranking bureaucrats have gone on official business and study tours of the Southeast Asian city-state. Meanwhile, scores of Singaporean businesses – backed by Mr. Lee and his successors – have pushed into China, investing in industrial parks and real-estate among other sectors, albeit with varying degrees of success.

More recently, Singapore’s influence on China has been particularly visible in Beijing’s recent legal reform push, scholars say.

The reforms, outlined by the Communist Party in an ambitious blueprint released last fall, aim to make the country’s courts more independent and credible while ensuring that they continue to cleave to the party’s core interests.

Fu Hualing, a professor of law at the University of Hong Kong, says the likely end-goal is a legal system that is efficient and consistent in settling commercial and personal disputes while bending to Beijing’s whims in politically sensitive cases, such as those dealing with dissidents, corruption or terrorism.

“They might not mention Singapore by name, but in many respects we’re moving in that direction. You’ll have a decent judicial system that’s ultimately under political control,” Mr. Fu says.

Jerome Cohen, a veteran China legal scholar at New York University, said the legal system developed under Mr. Lee might be the best China can hope for under the Communist Party. “An optimum, next-generation goal would be if they could produce a judiciary and government like Singapore’s,” he said. “That would at the very least enhance predictability.”

Such a system could work in China because — as in Singapore — the majority of regular citizens keep themselves distant from politics, legal scholars say. “If there’s a dark and hidden corner, most people choose not to look it,” says Mr. Fu."

MGL: So what did Lee think of President Xi?

I quote: "He is in the Mandela class of statesmen".

There are all sort of compliments Lee could have chosen, this one is very revealing. Mandela lead South Africa out of Apertheid. Is Lee inferring that he thinks President Lee could lead China away from the Party? This is not the first time we've visited this thought, and several of President Xi's actions are highly suggestive. I would add, from personal experience, that Chinese investors are fascinated by the history of the UK in the 1980's, and incredibly knowledgeable on the affairs of a small distant country that party orthodoxy and nationalist rhetoric regards as one of the great evil empires of the past.

High praise indeed.

We would add, that in the present round of SEO privatisations it is the Temesek model, designed by Lee Kuan Yew, that is being implemented.

Global emissions of carbon dioxide from the energy sector stalled in 2014

Data from the International Energy Agency (IEA) indicate that global emissions of carbon dioxide from the energy sector stalled in 2014, marking the first time in 40 years in which there was a halt or reduction in emissions of the greenhouse gas that was not tied to an economic downturn.

"This gives me even more hope that humankind will be able to work together to combat climate change, the most important threat facing us today," said IEA Chief Economist Fatih Birol, recently named to take over from Maria van der Hoeven as the next IEA Executive Director.

Global emissions of carbon dioxide stood at 32.3 billion tonnes in 2014, unchanged from the preceding year. The preliminary IEA data suggest that efforts to mitigate climate change may be having a more pronounced effect on emissions than had previously been thought.

The IEA attributes the halt in emissions growth to changing patterns of energy consumption in China and OECD countries. In China, 2014 saw greater generation of electricity from renewable sources, such as hydropower, solar and wind, and less burning of coal.

The equation for GDP is: GDP = Money Supply x Velocity of Money.

MGL: Thesis: EU central banks buy bonds from banks. Banks take cash, buy dollars and pay depositors out to shrink balance sheet. Dollar goes up. Banks contract. Velocity plummets.

This is the latest iteration on falling velocity which has been a huge drag on gold prices since the 1980 peak.

Now the dollar is exploding: Some years ago when we realised the significance of the shale, we suggested that it was very bullish for the dollar.

Two impacts: 1> Declining oil imports improved balance of trade. (BIG numbers) 2> Declining dependence on middle east crude gave Obama the policy option of withdrawing US military from the middle east and cutting defence expenditure. (BIG numbers)

But the Saudi's want to end this game.

Now the dollar is still going up, but this time its a herd of EU banks with dollar liabilities that they are desperate to extinguish. (Dollar goes up, liability VALUE increases, stresses capital ratio!).

BIS data at the end of Q3:

"The fact of the matter is that there is a parallel dollar-based financial system – call it the "Global Dollar system" – that operates outside the United States.

Using data from the BIS, we can estimate the size of this Global Dollar system. Starting with U.S. dollar liabilities of banks outside the United States, we quickly get around $13 trillion. (If you have a dollar-denominated account in a bank in London, Zurich or Hong Kong, it would be included in this sum.) Now, not all countries report to the BIS, so this subtotal is incomplete. China and Russia are missing, for example. In addition, Ecuador, El Salvador and Panama are dollarized, so their banks are issuing dollar liabilities. Tallying these non-reporting sources may add another $1 trillion. Next come a few trillion dollars more from dollar-denominated securities that are issued outside the United States (mostly in London)."

Here's the ECB balance sheet liabilities of Dollars: Each time there's a crisis the ECB is forced to shoulder the Banking system excess liabilities in the many and various rescue packages. As the emergency ends the banking system re-shoulders the liabilities, and the ECB outstanding, contracts. That trade is in the EU area, so has no $ consequences.

With QE occuring, the ECB is a net buyer of EU assets, so its non EU liabilities should be rising. They are not. Ergo the ECB is a massive buyer of dollars. Lets try that again: QE implies the EU is selling Euros to the banks, in order to sell Euros, or print, they are buying dollars. Thats what the chart says! These are really, really big numbers. That last little down tick is $50bn of contraction, or dollar purchases.

Oil prices rise after signs of U.S. production dip

Oil prices rose on Wednesday after signs of a dip in U.S. production, but gains were capped by Chinese quarterly growth slowing to a six-year low.

In the United States, North Dakota's February oil production fell 15,000 barrels per day (bpd) versus January, although the number of producing wells hit a record high.

This followed a U.S. Energy Information Administration (EIA) report forecasting U.S. shale production would fall by 45,000 bpd to 4.98 million bpd in May, which would be the first monthly decline in four years.

Analysts said the U.S. figures were pushing prices up. "We expect Brent Jun'15 and WTI Jun'15 to end today breaking resistance of $60.3 and $55.34 (per barrel)," Phillip Futures said.

But the slowing Chinese economy prevented prices from rising further.

BP seeks LNG buyers to finance $12 bln Tangguh Train 3 project

BP said it would be tough to proceed with financing for a planned third LNG train at its Tangguh project in West Papua, Indonesia, without buyers for the remaining 1.3 million tonnes of annual output from the production plant.

Prospects for new liquefied natural gas (LNG) developments globally have been hammered by the fallout from a 50-percent drop in oil prices since last June. The situation in Asia is set to get worse as two LNG projects in Australia come onstream this year, crowding an already amply supplied market.

"There is still 1.3 million tonnes per year (mtpa) that has not yet (been sold)," said Dharmawan Samsu, country head at BP Indonesia, noting that so far the firm had only found buyers for 2.5 million tonnes of expected output from Train 3.

Without buyers for the remainder it would be "difficult to proceed" with financing the third train project, which is currently expected to be completed by 2020, Samsu said on Tuesday.

BP will review its final investment decision for the $12 billion Train 3 project after a so-called Front End Engineering Design has been completed at the end of 2015 or early 2016, Samsu said.

"We're not looking at difficulties in funding, but more at the economics of the project," he said, declining to comment further on pricing.

Earlier, Samsu said Japan's Kansai Electric Power Co. had agreed to purchase 1 mtpa from Train 3, adding to the 1.5 mtpa committed to Indonesia's state electricity utility PLN.

A total of 7.6 mtpa of LNG from the first two Tangguh trains had been fully committed, he said.

MGL: If BP can't finance an LNG train then who can?

Dutch court orders production cut at part of Groningen field

A Dutch high court on Tuesday ordered a temporary halt to gas production around Loppersum, in the northern province of Groningen, because of safety concerns from earthquakes.

In a preliminary ruling, the Council of State said it would however not order a complete halt to gas production at the Groningen gas field, as complainants had sought.

Loppersum production was previously capped at 3 billion cubic meters (bcm) for 2015, representing roughly 9 percent of overall production from the Groningen field, Europe's largest.

"For the time being, gas may be extracted in and around Loppersum only if extraction from other locations is no longer possible and if necessary for the security of supply," a court statement said.

Judge Thijs Drupsteen said he was ordering the government's approval of the extraction plan submitted by NAM, a joint venture between Royal Dutch Shell and Exxon Mobil Corp. 0 to be "partially suspended". The administrative court has jurisdiction over government decisions.

The ruling on Tuesday was preliminary and based on complaints filed by two out of 40 applicants. The cases will be heard in full in mid-September, it said.

"If production were stopped in full, demand for gas from the Netherlands and neighbouring countries could not be met," the judge said.

MGL: Judge implicitly suggesting here that court will allow some production. Shell and Exxon still loose 90% of production, its approx 1.2bcf pa each. Not huge, but definately a ding.

Norway’s state-owned oil giant, Statoil, is reportedly cutting stuff in a new round of redundancies.

According to Aftenbladet, Statoil will cut up to 20 percent within its technical sector that employs around 12,000 engineers.

This might mean that up to 2,400 engineers will find themselves without employment, notably those that are drilling and maintaining wells, and administrative staff.

This move is a part of cost cutting measures caused by the drop in global oil prices.

Offshore Energy Today reached out to Statoil seeking confirmation of these reports; however, we are yet to receive a response.

MGL: We've cut the capex, and we've seen a dribble of redundancies so far, but there have to be more to come surely?

The Oil industry is now in project 'runoff' mode. We entered the downturn at peak capex, and with a projects stacked high on Big Oil's decks. The pressure is on to sustain those all important dividends, and only ENI has blinked so far. (No one is entirely sure whether ENI counts, is it really part of Big Oil or not? Small note: ENI has new senior management, so a clearing of the decks was always on the cards!)

So if you can't cut the dividend, then you have to cut costs really. Thats staff, people and particularly project generation teams. Low oil prices are seeping into the industry's consciousness slowly.

As an aside I listened to 3-4 hours of Laredo's presentation yesterday, and I simply don't recall anyone on the call mentioning the dreaded $50 number. Its so obvious, so out there, so in your face, it simply can't be true. Make no mistake, everyone is thinking about it, and hoping normal service will resume as soon as possible.

It’ll Take More Than Yemen’s LNG Shutdown to Blunt Supply Boom

There’s so much liquefied natural gas set to hit global markets this year that it’ll take more than the shutdown of Yemen’s only plant to threaten supplies.

As rebels seized army positions outside the nearby city of Balhaf, Yemen LNG Co. halted production and exports at its 6.7 million metric ton-a-year facility because of a “degredation of the security situation,” according to a statement on its website Tuesday. Its customer, Korea Gas Corp., and consultants including EnergyQuest and Manaar Energy Consulting, said that’s unlikely to disrupt the markets. Yemen accounts for about 2.2 percent of the world’s liquefaction capacity, data from the International Group of LNG Importers show.

The cost of LNG for delivery to Northeast Asia has slumped by more than half over the past year amid a collapse in oil prices and as supplies swell. About 12 million tons of the supercooled gas will start this year, the most since 2011, with more to flow in 2016.

MGL: No evidence of any reaction in LNG spot markets to this disruption. Our last report had Kepco oversupplied, and seeking to reduce purchases, so Kepco may simply shrug, and not replace the lost LNG.

MGL: We have an estimate now for the Bakken Fracklog via the state data. It looks to be around the 200k bpd mark. So with Texas at 400k bpd (on January data) and the Bakken at 200kbpd (on February data). We can infer the following:

~The Fracklog in January was some 1mbpd across the continental USA. ~The Fracklog appears to have increased dramatically between January and March. ~March estimates for the fracklog suggest 2mbpd.

This all has the Oil bulls frothing at the mouth for a breakout.

Cabot Drills Test Well in WV Rogersville Shale, More on the Way?

A fascinating story in Sunday’s Charleston Gazette shines a light on the Rogersville Shale formation in southwestern West Virginia and eastern Kentucky. Rogersville a shale layer that is older and much deeper than the Marcellus. The Marcellus is about a mile down. The Rogersville is between 9,000-14,000 feet down, or 2-3 times the depth of the Marcellus.

Until now we’ve heard about potential Rogersville activity in Kentucky . Two exploratory wells have already been drilled in the Rogersville in Kentucky. But the new news, the thing that interests us, is that Cabot Oil & Gas has now drilled a test well in the Rogersville in West Virginia.

"Production rumored by some to be slightly over 2000 bod for each of 3 zones which is crazy high and multiple industry estimates come in at slightly over 2100 bod for 2 of 3 zones tested which fits well with observations of two rounds of flare tests conducted over two two week periods with a day or two between the two rounds of flares. Industry estimates on the photos of the flare below were 4-10 mmcfd and daylight observers indicated it was smoky flare indicating wet gas.

Based on the two large flow tanks and no more than 8-12 frac tanks on the site there would have been no where to store the large oil flows during the tests so that leaves us with the assumption that the rumored flows were estimates based on chokes and some theoretical number of feet of lateral in a horizontal well.

Should these numbers hold up, even If we cut these flow rates in half leaving a net 2000 to 2300 and use BOED in lieu of BOD, this is definitely shaping up to be a world class play.

Regardless of how they are calculating the flows is does seem like the Rogersville Shale will definitely be a game changer for Eastern Kentucky and maybe the whole Country."

Our intrepid blogger trecked to the scene of the Cimerex well and photographed the flare:

Further it looks like this is CLR's new play alluded to in the last quarterly conference call:

"Sources indicate that Continental picked up an 85% interest in the deep rights on 7500 acres from privately held Hay Exploration for an estimated $9.4 million — $1250 per acre — that was being marketed at the NAPE Expo in Houston.

Late last year, Continental completed initial title work to buy the Rogersville Shale rights on an undisclosed amount of acreage from partners Nytis Exploration and Liberty Energy.

Full terms of the deal were not disclosed but Continental is understood to have spent about $20 million on the package.

The Rogersville formation is a Cambrian-aged dark-gray shale member of the Conasauga group that lies at depths ranging from 9000 to 14,000 at the base of the Rome Trough extensional basin."

An old Exxon mud core examined by state geologists last year showed wet gas from the core, and started the play. Continental does not pay $1250 an acre for moose pasture unless Harold Hamm is very excited.

Eclipse Resources announces revised capital budget, production

Eclipse Resources estimates that first quarter 2015 production averaged approximately 160 MMcfe per day, a 316% increase relative to the first quarter of 2014 and a 29% sequential increase over fourth quarter 2014 production For the full year 2015, Eclipse Resources expects production to be between 180 MMcfe per day and 190 MMcfe per day representing production growth at the midpoint of this range of 154% over 2014 average daily production Eclipse Resources' Board of Directors has approved a capital budget of $352 million for 2015 Following discussions with various financial partners, Eclipse Resources has made the decision not to pursue a drilling joint venture at this time

Eclipse Resources announced today that its Board of Directors has approved a revised capital budget of $352 million for 2015, representing a 45% reduction from its initial capital budget for the year, and a 57% decrease from 2014. The Company expects to spud approximately 19 net operated wells, and 2 net non-operated wells. The company expects to place 29 net wells (18 net operated wells and 11 net non-operated) wells into sales during the year.

MGL: Eclipse has barely $50m of cashflow to finance $352m of capex. Enterprise value is $1.7bn, PV10 is $183m. They are only 41% held by production, and only one of their core areas is really making economic returns today. There are 800 net wells to drill, 150 of which are economic at strip today. So you are paying $1.5bn for the call option on 700 wells becoming economic via price or productivity. ~$200m per tcf of resource, its in the Marcellus, so there's likely upside on the stacked pay. Range for comparison is ~$135 per tcf, with better cashflow!

Europe Finally Decides to Stunt Growth of Destructive Biofuels

Today the European Parliament's Environment Committee approved a deal with EU governments to cap the amount of harmful biofuels used to meet renewable energy targets.

Marc-Olivier Herman, Oxfam's EU biofuels expert, said: "The European Parliament and governments have finally decided to tone down a harmful biofuels policy that has only contributed to deprive poor people of food and accelerate the climate change it claims to fight."

"However, this new 7% cap on crop-based biofuels can only be a first step. Europe must phase out these fuels completely so they can no longer jeopardize food security and contribute to climate change."

A 7% cap on biofuels from agricultural crops (in comparison to 8.6% business as usual scenario) - with an option for Member states to go lower.

Indirect emissions will be reported on every year by the European Commission and by fuel suppliers by taking into account 'ILUC factors'. This will increase the transparency of the impacts of this policy for European citizens.

Codelco: copper production flat through 2020 despite $25 billion spend

Chilean state copper giant Codelco expects no significant gain in production through 2020 despite plans to invest $25 billion in its mines over the next five years, CEO Nelson Pizarro said Tuesday.

Speaking at the CRU World Copper Conference in Santiago, Pizarro said Codelco will invest around $5 billion annually through 2019 largely to replace exhausted mine capacity.

These investments will maintain production from Codelco's mines at around 1.7 million mt/year, Pizarro said.

Codelco also plans to begin construction of a new 100,000 mt/d concentrator plant to process sulfide resources from its Radomiro Tomic mine by year-end once it obtains environmental permits, with ramp-up beginning in 2019, the executive said.

Codelco data, however, shows that in 2018 output will fall below 1.6 million mt, compared to 1.672 million mt last year.

The development of a new mine level at the century-old El Teniente mine is running 38 months behind schedule Pizarro said.

MGL: $25bn simply sustains production. This is a massive change of tenor from Codelco. For years their projections have been rosy and ever upwards, their reality, volatile and slightly declining. If the best they can forecast is flat, then all the risk is on the downside.

Thats cements Copper price prospects for a decade. This is really important, there's an entire phalanx of metal analysts out there with rising Codelco production in their spreadsheets.

Antofagasta sees forecast global copper surplus disappearing in 2015

London-listed Antofagasta Minerals' newly installed chief executive sees the global copper market surplus practically disappearing this year due to kinks in output.

Analysts had anticipated seeing the first surplus in years in 2015, to the tune of 500,000 to 600,000 tonnes copper, but production stoppages, such as those caused by recent heavy rains and mudslides in northern Chile, have curtailed those estimates.

"What we've seen is that the surplus has been disappearing and we're probably talking about a market that is virtually in balance," Ivan Arriagada told Reuters in one of his first media interviews since assuming as CEO in February.

Antofagasta's flagship Los Pelambres mine in central Chile lost 8,500 tonnes of refined copper production earlier this year after protests by local villagers blocked access to the mining complex.

In light of the production loss, Antofagasta is in the process of refining its initial guidance of 710,000 tonnes of copper production for 2015 "depending on how much of that can be recovered," he said.

Arriagada sees the global copper market in a slight surplus of 100,000 to 150,000 tonnes this year, and remaining balanced in 2016 before returning to a deficit in 2017, "at which time there will be upward pressure on prices."

For this year, copper prices should fluctuate between $2.70 and $3.00 per pound, in line with market expectations, according to Arriagada.

Prices, a sticking point at the CRU Copper conference in Santiago this week, have been recovering from a five-year low in late January, but have lost momentum as sluggish demand during a normally strong seasonal period offsets an erosion of mine supply.

Asked if the lull in copper prices had created merger and acquisition opportunities, Arriagada said "there could be attractive opportunities ... there could be space in this context for new opportunities."

"We want to develop and grow ... so in that sense obviously we're always monitoring the market and eventual opportunities that may arise."

However, Arriagada denied that Antofagasta had ever been in talks with Vancouver-based Teck Resources Ltd about a business tie-up.

Zambia has approved a proposal to drop a recent hike in mining royalties as Africa’s second top copper producer seeks to resolve a six-month standoff with miners over the controversial tax increase.

The government intends to set its mining royalties at 9% for both open-pit and underground mines.

According to Reuters, the government intends to set its mining royalties at 9% for both open-pit and underground mines. In January, the country increased taxes for open pit mines from 6% to 20% and those for underground mines from 6% to 8%, as part of major overhaul to the industry's tax system announced last year.

The mover prompted warnings of closures and thousands of job losses, underscoring a growing trend across the continent, where governments from Tanzania to Guinea are changing tax regimes and adjusting ownership structures to get a larger share of natural resources.

From 1997 to 2013, mining attracted $12.6bn in foreign investment to Zambia, according to industry figures. The capital injection helped the southern African nation become one of the continent’s star economic performers, with average annual GDP growth of 6.4% over the last decade.

Today, mining employs 90,000 people and contributes about three-quarters of the country’s foreign exchange earnings and 25-30 % of government revenue.

MGL: Zambia backs off the killer 20% tax, and settles on a 9% tax on all mines, so thats a 50% increase in royalties and an approximate cut of 10% on pre tax income for all miners in Zambia.

Investors breathe a sigh of relief that its not worse.

PanAust rejects $844 mln bid from China's Guangdong

Australian copper and gold miner PanAust Ltd rejected on Wednesday an $844 million bid from its top shareholder, China's Guangdong Rising Assets Management (GRAM), but said it would be open to discussing a better offer.

GRAM offered A$1.71 a share, valuing PanAust at A$1.1 billion ($844 million), well below an offer of A$2.30 a share it made last year that PanAust also rebuffed.

"The PanAust Board believes there are compelling reasons why GRAM should pay more if it wishes to acquire increased ownership of PanAust," the company said in a statement, as expected.

PanAust mines copper in Laos and paid $125 million in late 2013 for the rights to the huge Frieda River copper project in Papua New Guinea.

It said the offer was well below analysts' average valuation of A$2.03 and failed to recognise that it expects to boost annual copper output by 25 percent by 2018 with no need for further capital.

It also said the bid did not appear to take into account a strong medium to long-term outlook for copper as global supplies grow tighter, with the company's Frieda River project well placed to benefit from rising prices.

PanAust further justified the rejection by saying that its shares, at A$1.74, last traded above GRAM's offer, indicating the market agreed that the offer was too low.

"While we believe the current offer is inadequate, we are open to engagement and to considering all proposals which we believe are in the best interests of our shareholders," PanAust Chairman Garry Hounsell said in a statement.

Guangdong, which owns 24 percent of PanAust, has urged shareholders to accept the all-cash offer, warning that PanAust may need to raise additional capital to get the Frieda River project into production, potentially sending its shares lower.

PanAust, which dumped former CEO and co-founder Garry Stafford late last year, plans to send shareholders its formal recommendation around April 30.

South Korea's Public Procurement Service (PPS) paid a premium of $223 per tonne in its latest aluminium tender, almost a third less than a month ago, highlighting an accelerating collapse in global premiums as supply swells.

PPS's purchase of 2,000 tonnes of Australian aluminium for shipment by July 20 marked a sharp drop from its last purchase at a $315 per tonne premium for the origin in March.

The state-run procurement agency also said on its website on Wednesday (www.g2b.go.kr) that it had bought another 2,000 tonnes of Indian aluminium for the same shipment at a $209 per tonne premium via tender, also down from its last purchase at a $308 per tonne premium. Both tenders closed on Tuesday.

The two tenders come amid a flood of supply in Asia, which is likely to speed a downturn in global premiums, a delivery surcharge paid on top of London Metal Exchange prices to obtain metal.

Asia has seen a particularly steep drop from record highs, due to its proximity to China, which has stepped up exports of semi-manufactured products, although exports dipped last month.

A searing record run for premiums over the past two years has helped many producers stay afloat during years of low aluminium prices. The steep drop will ramp pressure on producers to cut capacity.

Aluminium maker Alcoa Inc said last month it would shut its only remaining smelter inBrazil, as part of a wider move to curtail expensive capacity.

Surplus stock has also been seen in Japan where aluminium stocks held at three major ports climbed for a 12th month to hit a record peak at the end of March due to a high level of imports and slow housing sector demand.

Faced with high stocks and a supply surplus, aluminium prices have lost about 17 percent since their high in August 2014.

Australia's Fortescue Metals Group has two stark choices to deal with a crash in the iron ore market and cut its $9 billion debt pile - sell off stakes in its mines or transport infrastructure, or sell new shares.

Investors say the quickest capital-raising option for the world's No. 4 iron ore miner would be a rights issue, although that could lead to the dilution of the one-third stake held by Chairman Andrew "Twiggy" Forrest.

"There's no question, all of those things, in a challenging environment, get a run," said a person close to the company who asked not to be identified. "You've always got them on the agenda."

Fortescue, which has been ramping up output and cutting costs, updates its quarterly production and costs on Thursday, with investors anxious to see if it is burning through its $1.6 billion in cash as iron ore prices hover around $50 a tonne.

With valuable infrastructure and long-life mining assets, analysts say Fortescue is in better shape than smaller rivals like Atlas Iron, which last week moved to shut all its mines to stem losses.

But its debt load makes it more vulnerable than its much bigger rivals Rio Tinto and BHP Billiton, after it scrapped a $2.5 billion bond sale last month.

It could sell stakes in its mines, which are all 100 percent owned, unlike those of its rivals who already have partners. Or it could again try to sell a stake in its port and rail unit which it put up for sale in 2012 during a brief dip in iron ore prices.

"While the company's under duress, we believe it's unlikely to go bust, simply because there is strategic value in that infrastructure," said Ric Ronge, a portfolio manager at Pengana Capital.

In 2012, analysts estimated Fortescue could have raised up to A$4 billion by selling a minority stake in the port and rail, but such a price is unlikely now even if a buyer can be found.

MGL: That Fortescue moves under the spotlight should come as no surprise.

There is, however, an interesting wrinkle in the tale: if Fortescue sells its railroad, and thats the valuable asset here, the economics of an entire group of deposits suddenly wildy improve on open access. That means more supply!

Usiminas' main shareholders ordered to extend tender offer

Brazil's Usiminas said its two main shareholders have been ordered by the country's securities regulator to extend a partial tender offer to other minority shareholders - the latest twist in their heated battle for control of the steelmaker.

Usiminas is controlled through a shareholder pact between Luxembourg-based Ternium SA and Japan's Nippon Steel & Sumitomo Metal Corp but the two have been at loggerheads for six months over the departure of Usiminas' former CEO, leading to a number of court cases and appeals to the regulator.

Last October, Ternium increased its stake with a 616.7 million reais ($200 million) deal to buy shares owned by the pension fund of state-run Banco do Brasil SA, known as Previ. At the time, Ternium stated the deal would not automatically trigger a tender offer to other minority shareholders.

The decision by Brazilian securities regulator CVM, which was asked to review the deal by Nippon Steel, overturns that and says the offer must be extended by both Ternium and Nippon Steel, according to the Usiminas statement.

It is not immediately clear how the regulator's ruling would affect the battle for control. Ternium offered 12 reais per share in its offer, an 82 percent premium to the closing price on the day before the deal was announced, but since then the shares have rallied, closing at 16.80 reais on Tuesday.

According to Thomson Reuters data based on filings from November 2014, Ternium has a 26.9 percent stake in Usiminas while Nippon Steel holds 29.1 percent through two units. Rival steelmaker Companhia Siderurgica Nacional S.A. (CSN) owns 11.7 percent.

Ternium and Nippon Steel have been at odds since former Usiminas CEO Julian Eguren, who previously worked at Ternium, was dismissed over allegations of misuse of funds in September. Eguren denies wrongdoing and Ternium has demanded his reinstatement while Nippon Steel has refused.

MGL: Nippon Steel derailed a similiar bid by CSN some years ago. This is all happening in the voting class, the more liquid non voters trade at a paltry BRL$4.80. Nippon Steel wants to use Usiminas as a strategic vehicle to access Latin America, and other export markets.

Gerdau, controlled by Techint, wants to take full operational control. Meanwhile Banco Pactual has stepped into the fight with a 2% stake. Interesting spectacle, but we cant see any money being made by long suffering minority non voting shareholders.

China Steel Output Slides to Worst First Quarter in 20 Years

China’s crude steel output fell in the first three months of the year, the first decline over that period in 20 years, as the country grew at the slowest pace since the global recession.

Crude steel production from January to March slid 1.7 percent from a year earlier to 200.1 million metric tons, according to National Bureau of Statistics data released Wednesday in Beijing. First quarter output hasn’t contracted since 1995.

Falling production in the world’s largest steelmaker reflects the country’s slowing pace of construction and sliding exports. Output is poised to fall further as the government tries to trim overcapacity and cut pollution in its drive to shift the world’s second-biggest economy toward consumption and services.

“Given that China has been closing down some of the steel mills, the drop is less than we expected,” said Helen Lau, a metals and mining analyst at Argonaut Securities Ltd. in Hong Kong. “The less profitable and higher polluting ones are shutting, but the larger ones are taking their market share.”

The country’s gross domestic product in the three months through March rose 7 percent from a year earlier, the weakest pace since 2009, the statistics bureau said. That matches the median forecast in a Bloomberg survey, as well as the leadership’s full-year target.

MGL: So now that we've seen this nasty q1 figure we have to look forward:

1> Is the faction fight that completely stopped the economy in its tracks over? 2> Does Beijings change of music in the last two weeks signal something more -ahem- 'normal'?

Read our background piece on the burial of Zhou Ziyang.

Commodity Intelligence LLP is Authorised and Regulated by the Financial Conduct Authority

The material is based on information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such. Opinions expressed are our current opinions as of the date appearing on this material only.

Officers and employees, including persons involved in the preparation or issuance of this material may from time to time have “long” or “short” positions in the securities of companies mentioned herein. No part of this material may be redistributed without the prior written consent of Commodity Intelligence LLP.

So what is President Xi's agenda?

So what is President Xi's agenda? Some years ago when we realised the significance of the shale, we suggested that it was very bullish for the dollar.

Some years ago when we realised the significance of the shale, we suggested that it was very bullish for the dollar. Each time there's a crisis the ECB is forced to shoulder the Banking system excess liabilities in the many and various rescue packages. As the emergency ends the banking system re-shoulders the liabilities, and the ECB outstanding, contracts. That trade is in the EU area, so has no $ consequences.

Each time there's a crisis the ECB is forced to shoulder the Banking system excess liabilities in the many and various rescue packages. As the emergency ends the banking system re-shoulders the liabilities, and the ECB outstanding, contracts. That trade is in the EU area, so has no $ consequences.

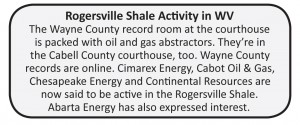

Cabot's not the only player in town.

Cabot's not the only player in town. Here's the Rodgersville shale map,

Here's the Rodgersville shale map,